Concept explainers

Videos

Comprehensive

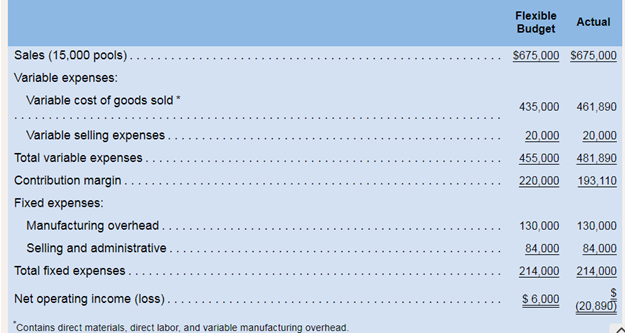

Miller Toy Company manufactures a plastic swimming pool at its Westwood Plant. The plant problems as shown by its June contribution format income statement below:

Janet Dunn. vio has just been appointed general mnagcr of the Westwood Plant. has been given instnctions to “get things under control. Upon reviewing the plants income statement. Ms. Dunn has concluded that the major problem lies in the variable cost of goods sold. She has been provided with the following

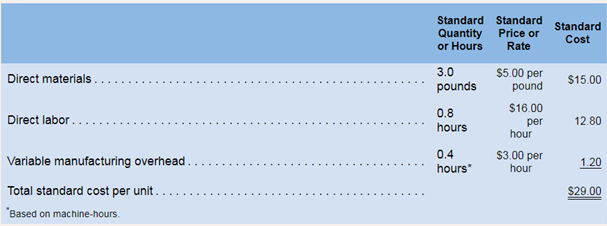

During June the plant produced 15,000 pools and incurred the following costs:

a. Purchased 60,000 pounds of materials at a cost of 54.95 per pound.

b. Used 49,200 pounds of materials in production. (Finished goods and work in process inventories are insignificant and can be ignored.)

c. Worked 11.800 direct labor-hours at a cost of 517.00 per hour.

d. Incurred variable

It is the company’s policy to close all variances to cost of goods solid on a monthly basis.

Required:

1. Compute the following variances for June:

a Materials price and quantity variances.

b. Labor rate and efficiency variances.

c. Variable overhead rate and efficiency variances.

2. Summarize the variances that you computed in (1) above by showing the net overall favorable or unfavorable variance for the month. What impact did this figure have on the company’s income statement? Show computations.

3. Pick out the two most significant variances that you computed in (1) above, Explain to Ms. Dunn possible causes of these variances.

1

Variances

A variance shows the difference between an actual amount and a budgeted or standard amount. Budgeted amount is calculated by a company using certain standards. A variance may either be favorable or unfavorable. It is usually considered as favorable if standard amount is higher than the actual amount.

To calculate: Value of various variances related to materials, labor and overheads.

Answer to Problem 18P

Material price variance is $3,000 Favorable and quantity variance is $3,200 Unfavorable.

Labor rate variance is calculated as $11,800Unfavorable and efficiency variance is $3,200 Favorable.

Overhead rate variance is calculated as $590Unfavorable and efficiency variance is $300 Favorable.

Explanation of Solution

Part a)

Calculation of material price and quantity variance:

Formula to calculate material price variance is

Here, actual quantity is given as 60,000 pounds, actual price is $4.95 per pound and standard price is $5 per pound. So, the variance will be:

Formula to calculate material quantity variance is

Here, actual quantity is given as 49,200, standard quantity is 45,000 (3.0 ponds * 15,000) and standard price is $5. So, the variance will be:

So, material price variance is $3,000 favorable and material quantity variance is $2,100 Unfavorable.

Part b)

Calculation of labor rate and efficiency variances:

Formula to calculate labor rate variance is

Here, actual hours are given as 11,800, actual rate is $17 and standard rate is $16. So, the variance will be:

Formula to calculate labor efficiency variance is

Here, standard rate is $16 per hour, actual hours are 11,800 and standard hours will be 12,000 (15,000 *0.8).So, variance will be:

Labor rate variance is calculated as $11,800unfavorable and efficiency variance is $3,200 Favorable.

Part c)

Calculation of variable overhead rate and efficiency variance:

Formula to calculate variable overhead rate variance is

Here, actual labor hours are 5,900 machine hours, actual rate is $3.10 ($18,290/5,900) and standard rate is $3.00. So, the variance will be:

Formula to calculate variable overhead efficiency variance is:

Here, standard rate is $3.00, actual hours are given as 5,900 and standard hours are 6,000 (15,000*0.4). So, the variance will be:

Variable overhead rate or spending variance is $590 Unfavorable and efficiency variance is $300 favorable.

2

Favorable or unfavorable variance

A variance is considered as a favorable variance if the actual amount is lower than the standard amount and it is considered unfavorable when actual amount is greater than the standard amount. After the calculation of all the variances, favorable or unfavorable amounts of all the variances are added to reach at the net overall effect.

To calculate: Amount of labor rate and efficiency variance.

Answer to Problem 18P

Overall, there is an unfavorable variance of $26,890.

Explanation of Solution

Net overall favorable or unfavorable variance will be calculated as:

| Variances | Amount | Net value |

| Material price variance | $3,000 F | |

| Material efficiency variance | $21,000 U | |

| Labor rate variance | $11,800 U | |

| Labor efficiency variance | $3,200 F | |

| Variable overhead rate or spending variance | $590 U | |

| Variable overhead efficiency variance | $300 F | |

| Net variance | $26,890 U |

There is a net unfavorable variance of $26,890. An unfavorable variance indicates that a company has incurred more, or extra cost as compare to its standard cost and therefore, it reduces the amount of profit earned by the company. This kind of variance alerts the management that profit of the company will be low than the expected profit. It should be detected at the earliest time possible and reasons of unfavorable variance should be fixed.

So, an unfavorable variance increase the cost and decreases the profit shown in the income statement.

3

Material efficiency variance

This variance represents the difference between the actual value of materials used by labor in producing goods and value that was budgeted to be used.

Labor rate variance

This variance represents the difference between actual value incurred on labors and value that was expected to be incurred.

To calculate: Amount of variable overhead rate and efficiency variance.

Answer to Problem 18P

Overhead rate variance is calculated as $280 unfavorable and efficiency variance is $480 Favorable.

Explanation of Solution

I am selecting the following two variances as most significant variances,

1 Material efficiency variance

2 Labor rate variance

I have selected theses two variances as they both have the highest unfavorable amount.

A material efficiency variance can be unfavorable because of several reasons, some of them are stated below:

1 When unskilled or unqualified labor is used.

2 When incorrect standards are used to calculate the standard cost.

2 When material having low quality is purchased.

3. When there is an increase in the wastages because of depreciation.

Labor rate variance can be unfavorable because of many reasons. Some of them are:

1 When incorrect standards are used to calculate the standard amount.

2 When some extra payments are being paid to labors.

3 When amount payable to labors include certain benefits.

4. When there some alterations are made in the product components.

Want to see more full solutions like this?

Chapter 9 Solutions

Introduction To Managerial Accounting

- Flexible budgeting and variance analysis Im Really Cold Coat Company makes womens and mens coats. Both products require filler and lining material. The following planning information has been made available: Im Really Cold Coat Company does not expect there to be any beginning or ending inventories of filler and lining material. At the end of the budget year, Im Really Cold Coat Company experienced the following actual results: The expected beginning inventory and desired ending inventory were realized. Instructions 1. Prepare the following variance analyses for both coats and the total, based on the actual results and production levels at the end of the budget year: A. Direct materials price, quantity, and total variance. B. Direct labor rate, time, and total variance. 2. Why are the standard amounts in part (1) based on the actual production at the end of the year instead of the planned production at the beginning of the year?arrow_forwardVariance interpretation Vanadium Audio Inc. is a small manufacturer of electronic musical instruments. The plant manager received the following variable factory overhead report for the past month of operations: Actual units produced: 15,000 (90% of practical capacity) The plant manager is not pleased with the 12,320 unfavorable variable factory overhead controllable variance and has come to discuss the matter with the controller. The following discussion occurred: Plant Manager: I just received this factory report for the latest month of operations. Im not very pleased with these figures. Before these numbers go to headquarters, you and I need to reach an understanding. Controller: Go ahead. Whats the problem? Plant Manager: Whats the problem? Well, everything. Look at the variance. Its too large. If I understand the accounting approach being used here, you are assuming that my costs are variable to the units produced. Thus, as the production volume declines, so should these costs. Well, I dont believe these costs are variable at all. I think they are fixed costs. As a result, when we operate below capacity, the costs really dont go down. Im being penalized for costs I have no control over. I need this report to be redone to reflect this fact. If anything, the difference between actual and budget is essentially a volume variance. Listen, I know that youre a team player. You really need to reconsider your assumptions on this one. Assume you are the controller. Write a memo responding to the plant manager.arrow_forwardFlexible budgeting and variance analysis I Love My Chocolate Company makes dark chocolate and light chocolate. Both products require cocoa and sugar. The following planning information has been made available: I Love My Chocolate Company does not expect there to be any beginning or ending inventories of cocoa or sugar. At the end of the budget year, I Love My Chocolate Company had the following actual results: Instructions 1. Prepare the following variance analyses for both chocolates and the total, based on the actual results and production levels at the end of the budget year: A. Direct materials price, quantity, and total variance. B. Direct labor rate, time, and total variance. 2. Why are the standard amounts in part (1) based on the actual production for the year instead of the planned production for the year?arrow_forward

- Uchdorf Manufacturing just completed a study of its purchasing activity with the objective of improving its efficiency. The driver for the activity is number of purchase orders. The following data pertain to the activity for the most recent year: Activity supply: five purchasing agents capable of processing 2,400 orders per year (12,000 orders) Purchasing agent cost (salary): 45,600 per year Actual usage: 10,600 orders per year Value-added quantity: 7,000 orders per year Required: 1. Calculate the volume variance and explain its significance. 2. Calculate the unused capacity variance and explain its use. 3. What if the actual usage drops to 9,000 orders? What effect will this have on capacity management? What will be the level of spending reduction if the value-added standard is met?arrow_forwardSulert, Inc., produces and sells gel-filled ice packs. Sulerts performance report for April follows: Required: 1. Calculate the contribution margin variance and the contribution margin volume variance. 2. Calculate the market share variance and the market size variance. (CMA adapted)arrow_forwardBudgeted unit sales for the entire countertop oven industry were 2,500,000 (of all model types), and actual unit sales for the industry were 2,550,000. Recall from Cornerstone Exercise 18.6 that Iliff, Inc., provided the following information: Required: 1. Calculate the market share variance (take percentages out to four significant digits). 2. Calculate the market size variance. 3. What if Iliff actually sold a total of 41,000 units (in total of the two models)? How would that affect the market share variance? The market size variance?arrow_forward

- Cortez Manufacturing, Inc. has the following flexible budget formulas and amounts: Actual results for May for the production and sale of 5,000 units were as follows: Prepare a performance report for May that includes the identification of the favorable and unfavorable variances.arrow_forwardDirect labor time variance Maywood City Police uses variance analysis to monitor police staffing. The following table identifies three common police activities, the standard time to perform each activity, and their actual frequency to establish the expected cost to serve these activities. The police are paid 25 per hour. The actual amount of hours per activity for the year were as follows: A. Determine the total budgeted cost to perform the three police activities. B. Determine the total actual cost to perform the three police activities. C. Determine the direct labor time variance. D. What does the time variance suggest?arrow_forwardBuenolorl Company produces a well-known cologne. The standard manufacturing cost of the cologne is described by the following standard cost sheet: Management has decided to investigate only those variances that exceed the lesser of 10% of the standard cost for each category or 20,000. During the past quarter, 250,000 four-ounce bottles of cologne were produced. Descriptions of actual activity for the quarter follow: a. A total of 1.35 million ounces of liquids was purchased, mixed, and processed. Evaporation was higher than expected. (No inventories of liquids are maintained.) The price paid per ounce averaged 0.42. b. Exactly 250,000 bottles were used. The price paid for each bottle was 0.048. c. Direct labor hours totaled 48,250, with a total cost of 733,000. Normal production volume for Buenolorl is 250,000 bottles per quarter. The standard overhead rates are computed by using normal volume. All overhead costs are incurred uniformly throughout the year. (Note: Round unit costs to the nearest cent and total amounts to the nearest dollar.) Required: 1. Calculate the upper and lower control limits for materials and labor. 2. Compute the total materials variance, and break it into price and usage variances. Would these variances be investigated? 3. Compute the total labor variance, and break it into rate and efficiency variances. Would these variances be investigated?arrow_forward

- Materials and labor variances Branca Inspections Inc. specializes in determining whether a building or houses drainpipes are properly tied into the citys sewer system. The company pours colored chemical through the pipes and collects an inspection sample from each outlet, which is then analyzed. Each job should take 15 hours for each of four inspectors, at a standard rate of 18 per hour. Each job requires a standard quantity of 5 gallons of Glow (a colored chemical), which should cost 25 per gallon. Data from the companys most recent job (a building) follow: Required: Compute the following variances, using the formulas on pages 421422 and 424: 1. Materials price and quantity variances. 2. Labor rate and efficiency variances.arrow_forwardRefer to Cornerstone Exercise 8.13. In March, Nashler Company produced 163,200 units and had the following actual costs: Required: 1. Prepare a performance report for Nashler Company comparing actual costs with the flexible budget for actual units produced. 2. What if Nashler Companys actual direct materials cost were 1,175,040? How would that affect the variance for direct materials? The total cost variance?arrow_forwardVariances Refer to Cornerstone Exercise 9.6. Required: 1. Calculate the variable overhead spending variance using the formula approach. (If you compute the actual variable overhead rate, carry your computations out to five significant digits and round the variance to the nearest dollar.) 2. Calculate the variable overhead efficiency variance using the formula approach. 3. Calculate the variable overhead spending variance and variable overhead efficiency variance using the three-pronged graphical approach. 4. What if 26,100 direct labor hours were actually worked in February? What impact would that have had on the variable overhead spending variance? On the variable overhead efficiency variance? Standish Company manufactures consumer products and provided the following information for the month of February: Required: 1. Calculate the fixed overhead spending variance using the formula approach. 2. Calculate the volume variance using the formula approach. 3. Calculate the fixed overhead spending variance and volume variance using the three-pronged graphical approach. 4. What if 129,600 units had actually been produced in February? What impact would that have had on the fixed overhead spending variance? On the volume variance?arrow_forward

Principles of Cost AccountingAccountingISBN:9781305087408Author:Edward J. Vanderbeck, Maria R. MitchellPublisher:Cengage Learning

Principles of Cost AccountingAccountingISBN:9781305087408Author:Edward J. Vanderbeck, Maria R. MitchellPublisher:Cengage Learning Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub

Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub Financial And Managerial AccountingAccountingISBN:9781337902663Author:WARREN, Carl S.Publisher:Cengage Learning,

Financial And Managerial AccountingAccountingISBN:9781337902663Author:WARREN, Carl S.Publisher:Cengage Learning, Managerial Accounting: The Cornerstone of Busines...AccountingISBN:9781337115773Author:Maryanne M. Mowen, Don R. Hansen, Dan L. HeitgerPublisher:Cengage Learning

Managerial Accounting: The Cornerstone of Busines...AccountingISBN:9781337115773Author:Maryanne M. Mowen, Don R. Hansen, Dan L. HeitgerPublisher:Cengage Learning Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning

Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning Excel Applications for Accounting PrinciplesAccountingISBN:9781111581565Author:Gaylord N. SmithPublisher:Cengage Learning

Excel Applications for Accounting PrinciplesAccountingISBN:9781111581565Author:Gaylord N. SmithPublisher:Cengage Learning