Cornerstones of Cost Management (Cornerstones Series)

4th Edition

ISBN: 9781305970663

Author: Don R. Hansen, Maryanne M. Mowen

Publisher: Cengage Learning

expand_more

expand_more

format_list_bulleted

Concept explainers

Videos

Textbook Question

Chapter 9, Problem 40P

Aspen Medical Laboratory performs comprehensive blood tests for physicians and clinics throughout the Southwest. Aspen uses a standard process-costing system for its comprehensive blood work. Skilled technicians perform the blood tests. Because Aspen uses a

For the month of November, Aspen reported the following actual results:

- a. Beginning work in process: 1,250 tests, 60 percent complete

- b. Tests started: 25,000

- c. Ending work in process: 2,500 tests, 40 percent complete

- d. Direct labor: 47,000 hours at $19 per hour

- e. Direct materials purchased and used: 102,000 at $4.25 per ounce

- f. Variable overhead: $144,000

- g. Fixed overhead: $300,000

- h. Direct materials are added at the beginning of the process.

Required:

- 1. Explain why the FIFO method is used for

process costing when a standard costing system has been adopted. - 2. Calculate the cost of goods transferred out (tests completed and transferred out) for the month of November. Does standard costing simplify process costing? Explain.

- 3. Calculate price and quantity variances for direct materials and direct labor.

Expert Solution & Answer

Trending nowThis is a popular solution!

Students have asked these similar questions

MedServices Inc. is divided into two operating departments: Laboratory and Tissue Pathology.The company allocates delivery and accounting costs to each operating department. Deliverycosts include the costs of a fleet of vans and drivers that drive throughout the state each day toclinics and doctors’ offices to pick up samples and deliver them to the centrally located laboratory and tissue pathology offices. Delivery costs are allocated on the basis of number of samples. Accounting costs are allocated on the basis of the number of transactions processed. Noeffort is made to separate fixed and variable costs; however, only budgeted costs are allocated.Allocations for the coming year are based on the following data:

Required:1. Assign the support department costs by using the direct method. (Note: Round allocationratios to four decimal places.)2. Assign the support department costs by using the sequential method, allocatingaccounting costs first. (Note: Round allocation ratios to four…

Cost Assignment and JIT

Bunker Company produces two types of glucose monitors (basic and advanced). Both pass through two producing departments: Fabrication and Assembly. Bunker also has an Inspection Department that is responsible for testing monitors to ensure that they perform within prespecified tolerance ranges (a sampling procedure is used). Budgeted data for the three departments are as follows:

Inspection

Fabrication

Assembly

Overhead

$320,000

$480,000

$136,000

Number of tests

—

20,000

60,000

Direct labor hours

—

48,000

24,000

In the Fabrication Department, the basic model requires 1.1 hour(s) of direct labor and the advanced model requires 2.2 hour(s). In the Assembly Department, the basic model requires 1.3 hour(s) of direct labor and the advanced model requires 2.45 hours. There are 30,000 basic units produced and 16,000 advanced units.

Immediately after preparing the budgeted data, a consultant suggests that two manufacturing cells be created:…

Variance Analysis in a Process-Costing Setting, Service Firm

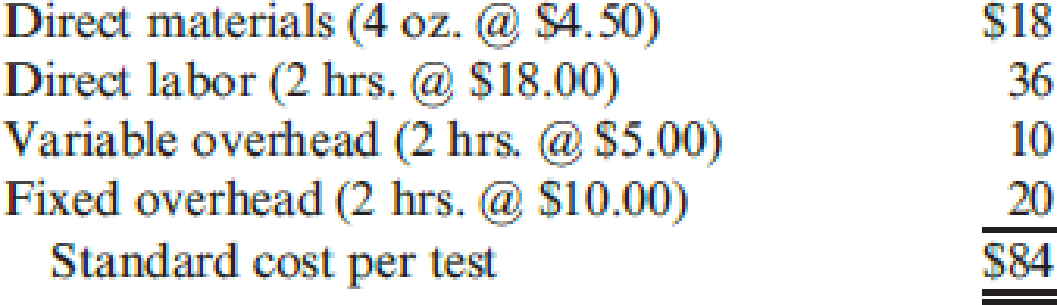

Kolite Medical Laboratory performs comprehensive blood tests for physicians and clinics throughout the Southwest. Kolite uses a standard process-costing system for its comprehensive blood work. Skilled technicians perform blood tests. Because Kolite uses a standard costing system, equivalent units are calculated using the FIFO method. The standard cost sheet for the blood test follows (these standards were used throughout the calendar year):

Direct materials (4 oz. @ $4.50)

$18

Direct labor (2 hrs. @ $18.00)

36

Variable overhead (2 hrs. @ $5.00)

10

Fixed overhead (2 hrs. @ $10.00)

20

Standard cost per test

$84

For the month of November, Kolite reported the following actual results:

Beginning work in process: 1,250 tests, 60 percent complete

Tests started: 25,000

Ending work in process: 2,500 tests, 40 percent complete

Direct labor: 47,000 hours at $19 per hour

Direct materials purchased and used: 102,000 at…

Chapter 9 Solutions

Cornerstones of Cost Management (Cornerstones Series)

Ch. 9 - Discuss the difference between budgets and...Ch. 9 - What is the quantity decision? The pricing...Ch. 9 - Why is historical experience often a poor basis...Ch. 9 - Prob. 4DQCh. 9 - How does standard costing improve the control...Ch. 9 - The budget variance for variable production costs...Ch. 9 - Explain why the direct materials price variance is...Ch. 9 - The direct materials usage variance is always the...Ch. 9 - The direct labor rate variance is never...Ch. 9 - Prob. 10DQ

Ch. 9 - Prob. 11DQCh. 9 - What is the cause of an unfavorable volume...Ch. 9 - Prob. 13DQCh. 9 - Explain how the two-, three-, and four-variance...Ch. 9 - Prob. 15DQCh. 9 - Prob. 1CECh. 9 - Direct Materials Usage Variance Refer to...Ch. 9 - Refer to Cornerstone Exercise 9.1. Guillermos Oil...Ch. 9 - Kavallia Company set a standard cost for one item...Ch. 9 - Yohan Company has the following balances in its...Ch. 9 - Standish Company manufactures consumer products...Ch. 9 - Variances Refer to Cornerstone Exercise 9.6....Ch. 9 - Standish Company manufactures consumer products...Ch. 9 - Mangia Pizza Company makes frozen pizzas that are...Ch. 9 - Mangia Pizza Company makes frozen pizzas that are...Ch. 9 - Refer to Cornerstone Exercise 9.9. Required: 1....Ch. 9 - Quincy Farms is a producer of items made from farm...Ch. 9 - During the year, Dorner Company produced 280,000...Ch. 9 - Zoller Company produces a dark chocolate candy...Ch. 9 - Oerstman, Inc., uses a standard costing system and...Ch. 9 - Refer to the data in Exercise 9.15. Required: 1....Ch. 9 - Chypre, Inc., produces a cologne mist using a...Ch. 9 - Refer to Exercise 9.17. Chypre, Inc., purchased...Ch. 9 - Delano Company uses two types of direct labor for...Ch. 9 - Jameson Company produces paper towels. The company...Ch. 9 - Madison Company uses the following rule to...Ch. 9 - Laughlin, Inc., uses a standard costing system....Ch. 9 - Responsibility for the materials price variance...Ch. 9 - Which of the following is true concerning labor...Ch. 9 - A company uses a standard costing system. At the...Ch. 9 - Relevant information for direct labor is as...Ch. 9 - Which of the following is the most likely...Ch. 9 - Haversham Corporation produces dress shirts. The...Ch. 9 - Plimpton Company produces countertop ovens....Ch. 9 - Algers Company produces dry fertilizer. At the...Ch. 9 - Misterio Company uses a standard costing system....Ch. 9 - Petrillo Company produces engine parts for large...Ch. 9 - Business Specialty, Inc., manufactures two...Ch. 9 - Vet-Pro, Inc., produces a veterinary grade...Ch. 9 - Refer to the data in Problem 9.34. Vet-Pro, Inc.,...Ch. 9 - Energy Products Company produces a gasoline...Ch. 9 - Nuevo Company produces a single product. Nuevo...Ch. 9 - Ingles Company manufactures external hard drives....Ch. 9 - As part of its cost control program, Tracer...Ch. 9 - Aspen Medical Laboratory performs comprehensive...Ch. 9 - Leather Works is a family-owned maker of leather...

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, accounting and related others by exploring similar questions and additional content below.Similar questions

- Jacson Company produces two brands of a popular pain medication: regular strength and extra strength. Regular strength is produced in tablet form, and extra strength is produced in capsule form. All direct materials needed for each batch are requisitioned at the start. The work orders for two batches of the products are shown below, along with some associated cost information: In the Mixing Department, conversion costs are applied on the basis of direct labor hours. Budgeted conversion costs for the department for the year were 60,000 for direct labor and 190,000 for overhead. Budgeted direct labor hours were 5,000. It takes one minute of labor time to mix the ingredients needed for a 100-unit bottle (for either product). In the Bottling Department, conversion costs are applied on the basis of machine hours. Budgeted conversion costs for the department for the year were 400,000. Budgeted machine hours were 20,000. It takes one-half minute of machine time to fill a bottle of 100 units. Required: 1. What are the conversion costs applied in the Mixing Department for each batch? The Bottling Department? 2. Calculate the cost per bottle for the regular and extra strength pain medications. 3. Prepare the journal entries that record the costs of the 12,000 regular strength batch as it moves through the various operations. 4. Suppose that the direct materials are requisitioned by each department as needed for a batch. For the 12,000 regular strength batch, direct materials are requisitioned for the Mixing and Bottling departments. Assume that the amount of cost is split evenly between the two departments. How will this change the journal entries made in Requirement 3?arrow_forwardFordman Company has a product that passes through two processes: Grinding and Polishing. During December, the Grinding Department transferred 20,000 units to the Polishing Department. The cost of the units transferred into the second department was 40,000. Direct materials are added uniformly in the second process. Units are measured the same way in both departments. The second department (Polishing) had the following physical flow schedule for December: Costs in beginning work in process for the Polishing Department were direct materials, 5,000; conversion costs, 6,000; and transferred in, 8,000. Costs added during the month: direct materials, 32,000; conversion costs, 50,000; and transferred in, 40,000. Required: 1. Assuming the use of the weighted average method, prepare a schedule of equivalent units. 2. Compute the unit cost for the month.arrow_forwardDama Company produces womens blouses and uses the FIFO method to account for its manufacturing costs. The product Dama makes passes through two processes: Cutting and Sewing. During April, Damas controller prepared the following equivalent units schedule for the Cutting Department: Costs in beginning work in process were direct materials, 20,000; conversion costs, 80,000. Manufacturing costs incurred during April were direct materials, 240,000; conversion costs, 320,000. Required: 1. Prepare a physical flow schedule for April. 2. Compute the cost per equivalent unit for April. 3. Determine the cost of ending work in process and the cost of goods transferred out. 4. Prepare the journal entry that transfers the costs from Cutting to Sewing.arrow_forward

- During December, Krause Chemical Company had the following selected data concerning the manufacture of Xyzine, an industrial cleaner: All materials are added at the beginning of processing in this department, and conversion costs are added uniformly during the process. The beginning work in process inventory had 120 of raw materials and 180 of conversion costs incurred. Materials added during December were 540, and conversion costs of 1,484 were incurred. Krause uses the first-in, first-out (FIFO) process cost method. The equivalent units of production used to compute conversion costs for December were: a. 110 units. b. 104 units. c. 100 units. d. 92 units.arrow_forwardHeap Company manufactures a product that passes through two processes: Fabrication and Assembly. The following information was obtained for the Fabrication Department for September: a. All materials are added at the beginning of the process. b. Beginning work in process had 80,000 units, 30 percent complete with respect to conversion costs. c. Ending work in process had 17,000 units, 25 percent complete with respect to conversion costs. d. Started in process, 95,000 units. Required: 1. Prepare a physical flow schedule. 2. Compute equivalent units using the weighted average method. 3. Compute equivalent units using the FIFO method.arrow_forwardUsing the same data found in Exercise 6.22, assume the company uses the FIFO method. Required: Prepare a schedule of equivalent units, and compute the unit cost for the month of December. Fordman Company has a product that passes through two processes: Grinding and Polishing. During December, the Grinding Department transferred 20,000 units to the Polishing Department. The cost of the units transferred into the second department was 40,000. Direct materials are added uniformly in the second process. Units are measured the same way in both departments. The second department (Polishing) had the following physical flow schedule for December: Costs in beginning work in process for the Polishing Department were direct materials, 5,000; conversion costs, 6,000; and transferred in, 8,000. Costs added during the month: direct materials, 32,000; conversion costs, 50,000; and transferred in, 40,000.arrow_forward

- Jameson Company produces paper towels. The company has established the following direct materials and direct labor standards for one case of paper towels: During the first quarter of the year, Jameson produced 45,000 cases of paper towels. The company purchased and used 135,700 pounds of paper pulp at 0.38 per pound. Actual direct labor used was 91,000 hours at 12.10 per hour. Required: 1. Calculate the direct materials price and usage variances. 2. Calculate the direct labor rate and efficiency variances. 3. Prepare the journal entries for the direct materials and direct labor variances. 4. Describe how flexible budgeting variances relate to the direct materials and direct labor variances computed in Requirements 1 and 2.arrow_forwardHolmes Products, Inc., produces plastic cases used for video cameras. The product passes through three departments. For April, the following equivalent units schedule was prepared for the first department: Costs assigned to beginning work in process: direct materials, 90,000; conversion costs, 33,750. Manufacturing costs incurred during April: direct materials, 75,000; conversion costs, 220,000. Holmes uses the weighted average method. Required: 1. Compute the unit cost for April. 2. Determine the cost of ending work in process and the cost of goods transferred out.arrow_forwardCardiff Inc. manufactures men’s sport shirts for large stores. It produces a single quality shirt in lots of a dozen according to each customer’s order and attaches the store’s label. The standard costs for a dozen shirts include the following: During October, Cardiff worked on three orders for shirts. Job cost records for the month disclose the following: The following information is also available: Cardiff purchased 95,000 yards of materials during October at a cost of $53,200. The materials price variance is recorded when goods are purchased, and all inventories are carried at standard cost. Direct labor incurred amounted to $112,750 during October. According to payroll records, production employees were paid $10.25 per hour. Overhead is applied on the basis of direct labor hours. Factory overhead totaling $22,800 was incurred during October. A total of $288,000 was budgeted for overhead for the year, based on estimated production at the plant’s normal capacity of 48,000 dozen shirts per year. Overhead is 60% fixed and 40% variable at this level of production. There was no work in process at October 1. During October, Lots 30 and 31 were completed, and all materials were issued for Lot 32, which was 80% completed as to labor and overhead. Required: Prepare a schedule computing the October total standard cost of Lots 30, 31, and 32. Prepare a schedule computing the materials price variance for October and indicate whether it is favorable or unfavorable. For each lot produced during October, prepare schedules computing the following (indicate whether favorable or unfavorable): Materials quantity variance in yards. Labor efficiency variance in hours. (Hint: Don’t forget the percentage of completion.) Labor rate variance in dollars. Prepare a schedule computing the total flexible-budget and production-volume overhead variances for October and indicate whether they are favorable or unfavorable. Give some reasons as to why the production-volume variance may be unfavorable and why it is important to correct the situation.arrow_forward

- Larkin Company produces leather strips for western belts using three processes: cutting, design and coloring, and punching. The weighted average method is used for all three departments. The following information pertains to the Design and Coloring Department for the month of June: a. There was no beginning work in process. b. There were 400,000 units transferred in from the Cutting Department. c. Ending work in process, June 30: 50,000 strips, 80 percent complete with respect to conversion costs. d. Units completed and transferred out: 330,000 strips. The following costs were added during the month: a. Direct materials are added at the beginning of the process. b. Inspection takes place at the end of the process. All spoilage is considered normal. Required: 1. Calculate equivalent units of production for transferred-in materials, direct materials added, and conversion costs. 2. Calculate unit costs for the three categories of Requirement 1. 3. What is the total cost of units transferred out? What is the cost of ending work-in-process inventory? How is the cost of spoilage treated? 4. Assume that all spoilage is considered abnormal. Now, how is spoilage treated? Give the journal entry to account for the cost of the spoiled units. Some companies view all spoilage as abnormal. Explain why. 5. Assume that 80 percent of the units spoiled are abnormal and 20 percent are normal spoilage. Show the spoilage treatment for this scenario.arrow_forwardSalisbury Bottle Company manufactures plastic two-liter bottles for the beverage industry. The cost standards per 100 two-liter bottles are as follows: At the beginning of March, Salisburys management planned to produce 500,000 bottles. The actual number of bottles produced for March was 525,000 bottles. The actual costs for March of the current year were as follows: a. Prepare the March manufacturing standard cost budget (direct labor, direct materials, and factory overhead) for Salisbury, assuming planned production. b. Prepare a budget performance report for manufacturing costs, showing the total cost variances for direct materials, direct labor, and factory overhead for March. c. Interpret the budget performance report.arrow_forwardDouglas Davis, controller for Marston, Inc., prepared the following budget for manufacturing costs at two different levels of activity for 20X1: During 20X1, Marston worked a total of 80,000 direct labor hours, used 250,000 machine hours, made 32,000 moves, and performed 120 batch inspections. The following actual costs were incurred: Marston applies overhead using rates based on direct labor hours, machine hours, number of moves, and number of batches. The second level of activity (the right column in the preceding table) is the practical level of activity (the available activity for resources acquired in advance of usage) and is used to compute predetermined overhead pool rates. Required: 1. Prepare a performance report for Marstons manufacturing costs in the current year. 2. Assume that one of the products produced by Marston is budgeted to use 10,000 direct labor hours, 15,000 machine hours, and 500 moves and will be produced in five batches. A total of 10,000 units will be produced during the year. Calculate the budgeted unit manufacturing cost. 3. One of Marstons managers said the following: Budgeting at the activity level makes a lot of sense. It really helps us manage costs better. But the previous budget really needs to provide more detailed information. For example, I know that the moving materials activity involves the use of forklifts and operators, and this information is lost when only the total cost of the activity for various levels of output is reported. We have four forklifts, each capable of providing 10,000 moves per year. We lease these forklifts for five years, at 10,000 per year. Furthermore, for our two shifts, we need up to eight operators if we run all four forklifts. Each operator is paid a salary of 30,000 per year. Also, I know that fuel costs about 0.25 per move. Assuming that these are the only three items, expand the detail of the flexible budget for moving materials to reveal the cost of these three resource items for 20,000 moves and 40,000 moves, respectively. Based on these comments, explain how this additional information can help Marston better manage its costs. (Especially consider how activity-based budgeting may provide useful information for non-value-added activities.)arrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning

Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning Principles of Cost AccountingAccountingISBN:9781305087408Author:Edward J. Vanderbeck, Maria R. MitchellPublisher:Cengage Learning

Principles of Cost AccountingAccountingISBN:9781305087408Author:Edward J. Vanderbeck, Maria R. MitchellPublisher:Cengage Learning Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub

Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub Managerial Accounting: The Cornerstone of Busines...AccountingISBN:9781337115773Author:Maryanne M. Mowen, Don R. Hansen, Dan L. HeitgerPublisher:Cengage Learning

Managerial Accounting: The Cornerstone of Busines...AccountingISBN:9781337115773Author:Maryanne M. Mowen, Don R. Hansen, Dan L. HeitgerPublisher:Cengage Learning Financial And Managerial AccountingAccountingISBN:9781337902663Author:WARREN, Carl S.Publisher:Cengage Learning,

Financial And Managerial AccountingAccountingISBN:9781337902663Author:WARREN, Carl S.Publisher:Cengage Learning,

Cornerstones of Cost Management (Cornerstones Ser...

Accounting

ISBN:9781305970663

Author:Don R. Hansen, Maryanne M. Mowen

Publisher:Cengage Learning

Principles of Cost Accounting

Accounting

ISBN:9781305087408

Author:Edward J. Vanderbeck, Maria R. Mitchell

Publisher:Cengage Learning

Managerial Accounting

Accounting

ISBN:9781337912020

Author:Carl Warren, Ph.d. Cma William B. Tayler

Publisher:South-Western College Pub

Managerial Accounting: The Cornerstone of Busines...

Accounting

ISBN:9781337115773

Author:Maryanne M. Mowen, Don R. Hansen, Dan L. Heitger

Publisher:Cengage Learning

Financial And Managerial Accounting

Accounting

ISBN:9781337902663

Author:WARREN, Carl S.

Publisher:Cengage Learning,

Cost Accounting - Definition, Purpose, Types, How it Works?; Author: WallStreetMojo;https://www.youtube.com/watch?v=AwrwUf8vYEY;License: Standard YouTube License, CC-BY