Subpart (a):

The equilibrium price and the quantity of haircuts and total surplus.

Subpart (a):

Explanation of Solution

Demand curve: The demand equation is

Supply curve: The supply equation is

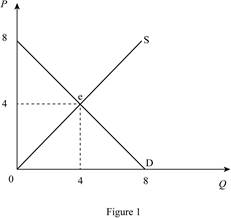

In Figure 1, horizontal axis measures quantity and vertical axis measures price. The curve D indicates demand and the curve S indicates supply. Market reaches the equilibrium at point ‘e’ where the demand curve intersects with supply curve.

Equilibrium price can be calculated as follows.

Equilibrium price is $4.

Thus, equilibrium quantity is 4 units.

Consumer surplus is $8.

Producer surplus is $8.

Total surplus can be calculated as follows.

Total surplus is $16.

Concept introduction:

Consumer surplus: It is the difference between the highest willing price of the consumer and the actual price that the consumer pays.

Producer surplus: It is the difference between the minimum accepted price for the producer and the actual price received by the producer.

Equilibrium price: It is the market price determined by equating the supply to the demand. At this equilibrium point, the supply will be equal to the demand and there will be no excess demand or

Subpart (b):

The equilibrium price and the quantity of haircuts and total surplus.

Subpart (b):

Explanation of Solution

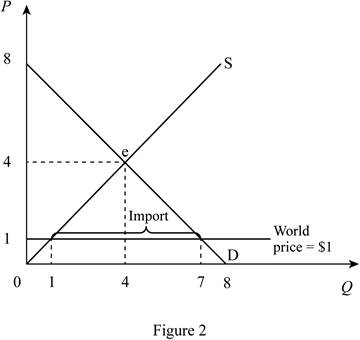

The world price for the good is $1. Thus, when the country opens the market for trade, the price becomes $1 in domestic country too. Figure 2 describe this situation.

In Figure 2, horizontal axis measures quantity and vertical axis measures price. The curve D indicates demand and the curve S indicates supply. Market reaches the equilibrium at point ‘e’ where the demand curve intersects with supply curve.

When the competitor (Rest of the world) sells a good at price $1, in domestic country equilibrium price become equal to world price. Thus, equilibrium price in the domestic country is $1.

Equilibrium domestic supply can be calculated by substituting the domestic equilibrium price in to supply equation.

Thus, equilibrium quantity is 1 unit.

Equilibrium domestic demand can be calculated by substituting the domestic equilibrium price in to demand equation.

Thus, equilibrium domestic demand is 7 units.

Total imports can be calculated as follows.

Domestic imports are 6 units.

Consumer surplus can be calculated as follows.

Consumer surplus is $24.5.

Producer surplus can be calculated as follows.

Producer surplus is $0.5.

Total surplus can be calculated as follows.

Total surplus is $25.

Concept introduction:

Consumer surplus: It is the difference between the highest willing price of the consumer and the actual price that the consumer pays.

Producer surplus: It is the difference between the minimum accepted price for the producer and the actual price received by the producer.

Equilibrium price: It is the market price determined by equating the supply to the demand. At this equilibrium point, the supply will be equal to the demand and there will be no excess demand or excess supply in an economy. Thus, the economy will be at equilibrium.

Subpar (c):

The equilibrium price and the quantity of haircuts and total surplus.

Subpar (c):

Explanation of Solution

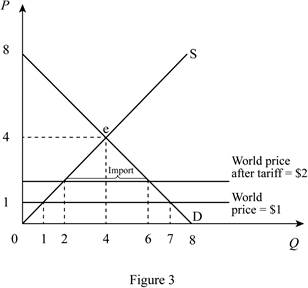

When domestic country impose tariff of $1, the price in domestic country increases from $1 to $2. This increase in price is shown in the Figure 3.

In Figure 3, horizontal axis measures quantity and vertical axis measures price. The curve D indicates demand and the curve S indicates supply. Market reaches the equilibrium at point ‘e’ where the demand curve intersects with supply curve. Price is increases from $1 to $2 due to the tariff of $1.

Domestic equilibrium price can be calculated as follows.

New domestic price is $2.

Equilibrium domestic supply can be calculated by substituting the domestic equilibrium price in to supply equation.

Thus, equilibrium quantity is 2 units.

Equilibrium domestic demand can be calculated by substituting the domestic equilibrium price in to demand equation.

Thus, equilibrium domestic demand is 6 units.

Total imports can be calculated as follows.

Domestic imports are 4 units.

Consumer surplus can be calculated as follows.

Consumer surplus is $18.

Producer surplus can be calculated as follows.

Producer surplus is $2.

Government revenue can be calculated as follows.

Government revenue is 4.

Total surplus can be calculated as follows.

Total surplus is $24.

Concept introduction:

Consumer surplus: It is the difference between the highest willing price of the consumer and the actual price that the consumer pays.

Producer surplus: It is the difference between the minimum accepted price for the producer and the actual price received by the producer.

Equilibrium price: It is the market price determined by equating the supply to the demand. At this equilibrium point, the supply will be equal to the demand and there will be no excess demand or excess supply in an economy. Thus, the economy will be at equilibrium.

Subpart (d):

Calculate total gains and deadweight loss .

Subpart (d):

Explanation of Solution

Total gains from opening up trade can be calculated as follows.

Total gains are$8.

Deadweight loss can be calculated as follows.

Deadweight loss is $1.

Want to see more full solutions like this?

Chapter 9 Solutions

Principles of Microeconomics

- Explain how a subsidy on agricultural goods like sugar adversely affects the income of foreign producers of imported sugar.arrow_forwardSteel Industry Consider a small country that exports steel. Suppose the following graph depicts the domestic demand and supply for steel in this country. One of the two price lines represents the world price of steel. Use the following graph to help you answer the questions below. You will not be graded on any changes made to this graph. 1. Because this country exports steel, the world price is represented by P1 or P2. Suppose that a “pro-trade” government decides to subsidize the export of steel by paying $10 for each ton sold abroad. 2. With this export subsidy, the price paid by domestic consumers is $???? per ton, and the price received by domestic producers is $???? per ton. 3. The quantity of steel consumed by domestic consumers INCREASES or REMAINS UNCHANGED or DECREASES, the quantity of steel produced by domestic producers INCREASES or REMAINS UNCHANGED or DECREASES, and the quantity of steel exported INCREASES or REMAINS UNCHANGED or DECREASES. 4. TRUE or FALSE:…arrow_forward. The United States currently imports all of its coffee. The annual demand for coffee by U.S. consumers is given by the demand curve Qd = 150 − 10P, where Qd is quantity (in millions of pounds) and P is the market price per pound of coffee. Suppose the domestic supply is Qs = 10P −50. The U.S. coffee market is competitive. Suppose that the world price of coffee is $6. Congress is considering a tariff on coffee imports of $2 per pound. (a) Find the producer and consumer surplus if there was no trade. (b) Calculate the consumer and producer surplus after we engage in free trade. (c) If the tariff is imposed calculate the changes to consumer and producer surplus. (d) Other than lower prices, provide two benefits that can occur as a result of free trade.arrow_forward

- Scenario 9-1 For a small country called Boxland, the equation of the domestic demand curve for cardboard is QD = 380 − 2P, where QD represents the domestic quantity of cardboard demanded, in tons, and P represents the price of a ton of cardboard. For Boxland, the equation of the domestic supply curve for cardboard is QS = –60 + 3P, where QS represents the domestic quantity of cardboard supplied, in tons, and P again represents the price of a ton of cardboard. Refer to Scenario 9-1. Suppose the world price of cardboard is $139 and international trade is allowed. Then Boxland’s consumers demand Group of answer choices 204 tons of cardboard and Boxland’s producers supply 357 tons of cardboard. 204 tons of cardboard and Boxland’s producers supply 204 tons of cardboard. 102 tons of cardboard and Boxland’s producers supply 204 tons of cardboard. 102 tons of cardboard and Boxland’s producers supply 357 tons of cardboard.arrow_forwardThe following graph shows the domestic market for oil in the United States, where SDSD is the domestic supply curve, and DDDD is the domestic demand curve. Assume the United States is considered a large nation, meaning that changes in the quantity of its imports due to a tariff influence the world price of oil. Under free trade, the United States faced a total supply schedule of SD+WSD+W, which shows the quantity of oil that both domestic and foreign producers together offer domestic consumers. In this case, the free-trade equilibrium (black plus) occurs at a price of $240 per barrel of oil and a quantity of 9 million barrels. At this price, the United States imports 6 million barrels of oil. Suppose the U.S. government imposes a $60-per-barrel tariff on oil imports.arrow_forwardConsider a small country where the domestic market for sandals is described by the following demand and supply equations, respectively: P = 100 – (1/3)Q and P = 20 + (1/2)Q where P represents the price of a pair of sandals and Q represents the quantity of sandals. The world price for a pair of sandals is $60. Therefore the gains from trade would bearrow_forward

- Consider a small country that exports steel. Suppose the following graph depicts the domestic demand and supply for steel in this country. One of the two price lines represents the world price of steel. Because this country exports steel, the world price is represented by(p1 or p2) . Suppose that a “pro-trade” government decides to subsidize the export of steel by paying $10 for each ton sold abroad. With this export subsidy, the price paid by domestic consumers is $______ per ton, and the price received by domestic producers is$_______per ton. The quantity of steel consumed by domestic consumers (reamins unchanged, decrease, and increase) , the quantity of steel produced by domestic producers (reamins unchanged, decrease, and increase) , and the quantity of steel exported (reamins unchanged, decrease, and increase) . True or False: With the export subsidy, this country will start importing steel from abroad. Under the export subsidy, consumer surplus is…arrow_forwardQuestion 31 Consider a small country where the domestic market for sandals is described by the following demand and supply equations, respectively: P = 100 – (1/2)Q and P = 20 + (1/3)Q where P represents the price of a pair of sandals and Q represents the quantity of sandals. The world price for a pair of sandals is $45. Therefore the gains from trade would be $135.00 $102.50 $88.75 $122.50arrow_forwardThe market for pencils has a domestic demand equation P=20−0.5Q�=20−0.5�, and a domestic supply equation P=5+Q�=5+�, where quantity is measured in thousands. The world supply equation for pencils is PW=10��=10. The domestic government decides to implement a tariff of $10 per thousand pencils. As a result of the tariff, the new domestic price of pencils isarrow_forward

- Consider a small country that exports steel. Suppose the following graph depicts the domestic demand and supply for steel in this country. One of the two price lines represents the world price of steel. ecause this country exports steel, the world price is represented by . Suppose that a “pro-trade” government decides to subsidize the export of steel by paying $10 for each ton sold abroad. With this export subsidy, the price paid by domestic consumers is per ton, and the price received by domestic producers is per ton. The quantity of steel consumed by domestic consumers , the quantity of steel produced by domestic producers , and the quantity of steel exported . True or False: With the export subsidy, domestic producers will sell steel to domestic consumers and sell the rest abroad. True False Under the export subsidy, consumer surplus is and producer surplus is . Government revenue by (increases or Decreases) . As a…arrow_forwardThe figure shows a country’s domestic supply and demand curves for a good, as well as the world price, Pw, for the good that it faces, as a small country, on the world market. Initially, the country is exporting X1 units of that good at that price. Suppose that producers in this industry lobby policy makers to provide them with some sort of assistance to help them export even more. Policy makers are considering an export subsidy. What area represents the cost of this subsidy to the government (taxpayers)? Group of answer choices b+c+d a+b+c+d c+d a+b+carrow_forwardSuppose that a country implements a $20 tariff. Before the tariff, the country was importing 900 units of the good. After the tariff, the country imported 850 units of the good. What is the deadweight loss from the tariff? Assume that domestic supply and demand are linear.arrow_forward

Principles of Macroeconomics (MindTap Course List)EconomicsISBN:9781285165912Author:N. Gregory MankiwPublisher:Cengage Learning

Principles of Macroeconomics (MindTap Course List)EconomicsISBN:9781285165912Author:N. Gregory MankiwPublisher:Cengage Learning Principles of Economics, 7th Edition (MindTap Cou...EconomicsISBN:9781285165875Author:N. Gregory MankiwPublisher:Cengage Learning

Principles of Economics, 7th Edition (MindTap Cou...EconomicsISBN:9781285165875Author:N. Gregory MankiwPublisher:Cengage Learning Principles of MicroeconomicsEconomicsISBN:9781305156050Author:N. Gregory MankiwPublisher:Cengage Learning

Principles of MicroeconomicsEconomicsISBN:9781305156050Author:N. Gregory MankiwPublisher:Cengage Learning

Economics: Private and Public Choice (MindTap Cou...EconomicsISBN:9781305506725Author:James D. Gwartney, Richard L. Stroup, Russell S. Sobel, David A. MacphersonPublisher:Cengage Learning

Economics: Private and Public Choice (MindTap Cou...EconomicsISBN:9781305506725Author:James D. Gwartney, Richard L. Stroup, Russell S. Sobel, David A. MacphersonPublisher:Cengage Learning Microeconomics: Private and Public Choice (MindTa...EconomicsISBN:9781305506893Author:James D. Gwartney, Richard L. Stroup, Russell S. Sobel, David A. MacphersonPublisher:Cengage Learning

Microeconomics: Private and Public Choice (MindTa...EconomicsISBN:9781305506893Author:James D. Gwartney, Richard L. Stroup, Russell S. Sobel, David A. MacphersonPublisher:Cengage Learning