a.

To evaluate the marginal revenue and Average revenue functions from the table given in the question.

a.

Explanation of Solution

Average revenue is the revenue which is obtained by dividing total revenue by quantity.

Marginal revenue is the additional revenue which is obtained by selling an extra unit of the product.

Formula to find the Marginal revenue (MR) and Average revenue (AR)

| Output | Total Revenue (TR) | Marginal Revenue | Average Revenue |

| 0 | 0 | - | - |

| 1 | 34 |

|

|

| 2 | 66 |

|

|

| 3 | 96 | 30 | 32 |

| 4 | 124 | 28 | 31 |

| 5 | 150 | 26 | 30 |

| 6 | 174 | 24 | 29 |

| 7 | 196 | 22 | 28 |

| 8 | 216 | 20 | 27 |

| 9 | 234 | 18 | 26 |

| 10 | 250 | 16 | 25 |

| 11 | 264 | 14 | 24 |

| 12 | 276 | 12 | 23 |

| 13 | 286 | 10 | 22 |

| 14 | 294 | 8 | 21 |

| 15 | 300 | 6 | 20 |

| 16 | 304 | 4 | 19 |

| 17 | 306 | 2 | 18 |

| 18 | 306 | 0 | 17 |

| 19 | 304 | -2 | 16 |

| 20 | 300 | -4 | 15 |

Introduction: Average revenue is revenue produced per unit of product sold. It plays a part in deciding the income for a company. The average revenue is less than the average (total) expense per unit income. An organization typically aims to generate the amount of production that maximizes income.

b.

To evaluate the marginal cost and Average cost functions from the table given in the question.

b.

Explanation of Solution

Formula to find the MC and AC are:

| Output | Total Cost (TC) | Marginal Cost | Average Revenue |

| 0 | 20 | - | - |

| 1 | 26 |

|

|

| 2 | 34 |

|

|

| 3 | 44 | 10 | 14.7 |

| 4 | 56 | 12 | 14.0 |

| 5 | 70 | 14 | 14.0 |

| 6 | 86 | 16 | 14.3 |

| 7 | 104 | 18 | 14.9 |

| 8 | 124 | 20 | 15.5 |

| 9 | 146 | 22 | 16.2 |

| 10 | 170 | 24 | 17.0 |

| 11 | 196 | 26 | 17.8 |

| 12 | 224 | 28 | 18.7 |

| 13 | 254 | 30 | 19.5 |

| 14 | 286 | 32 | 20.4 |

| 15 | 320 | 34 | 21.3 |

| 16 | 356 | 36 | 22.3 |

| 17 | 394 | 38 | 23.2 |

| 18 | 434 | 40 | 24.1 |

| 19 | 476 | 42 | 25.1 |

| 20 | 520 | 44 | 26.0 |

Introduction: The average cost method assigns a cost to inventory items based on the overall cost of the produced or manufactured goods over a period divided by the total number of products purchased or made. Often known as weighted-average method, is the average cost method.

c.

To evaluate the point where MR = MC and the output level in the graph that maximizes profits.

c.

Explanation of Solution

In economics, profit maximization is the short-term or long-term mechanism by which a firm can decide the levels of price, input, and production that lead to the highest benefit.

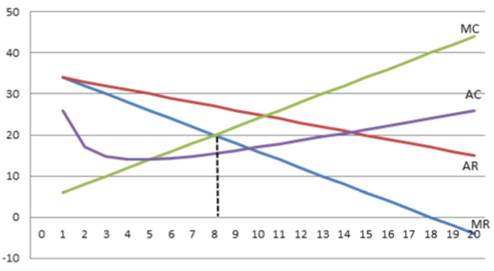

The graph is shown below:

Marginal revenue equals to Marginal cost when Output (Q) = 8, where MC = MR =20

Introduction: Marginal revenue is the rise in revenue arising from the selling of one extra output unit. Although marginal revenue may remain constant for a certain level of production, the law of diminishing returns follows and inevitably slows down as the level of production increases.

d.

To evaluate the point where MR = MC and the output level in the graph that maximizes profits.s

d.

Explanation of Solution

The average cost method assigns a cost to inventory items based on the overall cost of the produced or manufactured goods over a period divided by the total number of products purchased or made. Often known as weighted-average method, is the average cost method.

In economics, profit maximization is the short-term or long-term mechanism by which a firm can decide the levels of price, input, and production that lead to the highest benefit.

Referring from the tables in part (a) and part (b) and the solution at Q = 8, the table is given below:

| Output | Marginal Cost | Marginal Revenue |

| 8 | 20 | 20 |

Introduction: Marginal revenue is the rise in revenue arising from the selling of one extra output unit. Although marginal revenue may remain constant for a certain level of production, the law of diminishing returns follows and inevitably slows down as the level of production increases. Perfectly competitive firms continue to generate production until marginal revenue is equal to marginal costs.

Want to see more full solutions like this?

Chapter B Solutions

Managerial Economics: Applications, Strategies and Tactics (MindTap Course List)

- Profit loss analysis. Use the revenue and cost functions from Problem 63 in this exercise: where x is in millions of chips, and R(x) and C(x) are in millions of dollars. Both functions have domain (A) Form a profit function P, and graph R, C, and P in the same rectangular coordinate system. (B) Discuss the relationship between the intersection points of the graphs of R and C and the x intercepts of P. (C) Find the x intercepts of P and the break-even points to the nearest thousand chips. (D) Refer to the graph drawn in part (A). Does the maximum profit appear to occur at the same value of x as the maximum revenue? Are the maximum profit and the maximum revenue equal? Explain. (E) Verify your conclusion in part (D) by finding the value of x (to the nearest thousand chips) that produces the maximum profit. Find the maximum profit (to the nearest thousand dollars) Problem 63 Break-even analysis. Use the revenue function from Problem 61 in this exercise and the given cost…arrow_forwardAOF is the only firm selling beer around Isla Vitas, which has a beer fountain in the backyard so the marginal cost of producing beer is 0. There are two groups of consumers: students and non students. The students' beer inverse demand function is p=50-5q, and the non-students' beer inverse demand function is p=10-2q. AOF sells beer in two sizes: 10 ounces bottle and 5 ounces can. Due to a local act, the consumers can only buy either 1 bottle or 1 can of beer. AOF can charge different prices on each bottle and each can of beer, while it cannot tell whether a customer is a student or not. In order to maximize the profits, how much should AOF charge its 10 ounces bottle? Answer: 87.5arrow_forwardAssume that a competitive firm has the total cost function: TC=1q3−40q2+820q+1900TC=1q3-40q2+820q+1900 Suppose the price of the firm's output (sold in integer units) is $650 per unit. Using tables (but not calculus) to find a solution, what is the total profit at the optimal output level? Please specify your answer as an integer.arrow_forward

- Habib Bank Limited estimates equation of demand of its product as: Q = 55 – 0.5P - (where P = price and Q = Quantity of output), and its total cost of production as TC = 20 + Q + 0.2Q2 Where TC = total cost and Q = Quantity of output) Write the equations of the firm’s costs, as a function of Q: Average Total Cost ATC? Average Variable Cost AVC? Average Fixed Cost AFC.? Marginal Cost MC? The output level that will maximize total profit and the amount of revenue and profit that Habib Bank would receive at optimal level of production.? The output level that minimizes average total cost.? please answer all questionsarrow_forwardYou are the manager of a firm that produces products X and Y at zero cost. You know that different types of consumers value your two products differently, but you are unable to identify these consumers individually at the time of the sale. In particular, you know there are three types of consumers (1,000 of each type) with the following valuations for the two products: a. What are your firm’s profits if you charge $40 for product X and $60 for product Y? b. What are your profits if you charge $90 for product X and $160 for product Y? c. What are your profits if you charge $150 for a bundle containing one unit of product X and one unit of product Y? d. What are your firm’s profits if you charge $210 for a bundle containing one unit of X and one unit of Y, but also sell the products individually at a price of $90 for product X and $160 for product Y?arrow_forwardDefine Q to be the level of output produced and sold, and assume that the firm’s cost function is given by the relationship TC = 20 + 5Q + Q2 Furthermore, assume that the demand for the output of the firm is a function of price P given by the relationship Q = 25 - P a. Define total profit as the difference between total revenue and total cost, and express in terms of Q the total profit function for the firm. (Note: Total revenue equals price per unit times the number of units sold.) b. Determine the output level where total profits are maximized. c. Calculate total profits and selling price at the profit-maximizing output level. d. If fixed costs increase from $20 to $25 in the total cost relationship, determine the effects of such an increase on the profit-maximizing output level and total profits.arrow_forward

- Suppose that two European electronics companies, Siemens (Firm S) and Alcatel-Lucent (Firm T), jointly hold a patent on a component used in airport radar systems. - Demand for the component is given by the following function \[ P=1,000-Q \] - The total cost functions of manufacturing and selling the component for the respective firms are \[ \begin{array}{c} T C_{S}=70,000+5 Q_{S}+0.25 Q_{S}^{2} \\ T C_{T}=110,000+5 Q_{T}+0.15 Q_{T}^{2} \end{array} \] Assume that the firms agreed to form cartel and calculate the joint profit.arrow_forwardAssume that a competitive firm has the total cost function: TC=1q3−40q2+880q+2000 T C = 1 q 3 - 40 q 2 + 880 q + 2000 Suppose the price of the firm's output (sold in integer units) is $550 per unit. Create tables (but do not use calculus) with columns representing cost, revenue, and profit to find a solution. How many units should the firm produce to maximize profit? Please specify your answer as an integer. What is the total profit at the optimal output level? Please specify your answer as an integer.arrow_forwardProfit maximization using total cost and total revenue curves Suppose Caroline runs a small business that manufactures shirts. Assume that the market for shirts is a competitive market, and the market price is $20 per shirt. The following graph shows Caroline's total cost curve. Use the blue points (circle symbol) to plot total revenue and the green points (triangle symbol) to plot profit for shirts quantities zero through seven (inclusive) that Caroline produces. Caroline's profit is maximized when she produces______ shirts. When she does this, the marginal cost of the last shirt she produces is ______, which is (GREATER OR LESS) than the price Caroline receives for each shirt she sells. The marginal cost of producing an additional shirt (that is, one more shirt than would maximize her profit) is _____, which is (GREATER OR LESS) than the price Caroline receives for each shirt she sells. Therefore, Caroline's profit-maximizing quantity corresponds to the…arrow_forward

- Suppose you are working as the CEO of an airline. One of your airline's wide-body aircraft operates in a two-class configuration with 500 economy seats and 200 business seats. On the routes the wide-body aircraft flies, the airline's marginal cost per passenger is $1,000 in economy and $1,500 in business. According to the airline's internal data, the willingness to pay (WTP) of leisure pax for economy travel is $2,000, while their WTP for business travel is $2,500. On the other hand, business pax' WTP for economy travel is $4,500, while their WTP for business travel is $10,000. Finally, airlines charge different fares for economy and business, and there are more pax with WTP's as specified above than the number of seats in each class. The maximum certified capacity for this widebody aircraft is 500 seats in economy, so the airline cannot increase the number of seats in this class any further. But if airlines deliberately degrade service in economy even further (e.g. by offering less…arrow_forwardSuppose a firm’s inverse demand curve is given by P = 120 - .5Q and its cost equation is C = 420 + 60Q + Q2. a. Find the firm’s optimal quantity, price, and profit (1) by using the profit and marginal profit equations and (2) by setting MR equal to MC. Also provide a graph of MR and MC. b. Suppose instead that the firm can sell any and all of its output at the fixed market price P 120. Find the firm’s optimal output.arrow_forwardJointJuice produces a prepackaged joint support supplement for relief of joint pain with 180 tablets per bottle and operates in a perfectly competitive market. Basically, all the firms in this competitive market have technologies (production and cost conditions) that are the same as JointJuice’s. Suppose JointJuice’s total cost function is given by the following where q is JointJuice’s quantity of packages per day: C(q) = 250 + 6q + 0.1q^2 The market demand function for the output in this market is given by: Q = 1848 - 2P If there are 20 identical firms in this industry, find the market equilibrium price for the prepackaged supplements. Calculate JointJuice’s optimal output level and profits given the market price for the product. If JointJuice is typical of the firms in this industry calculate the firm’s long-run equilibrium output, price, and profit level. Suppose the situation changes. JointJuice has its plant in Portland Oregon. The local government passes a new tax on…arrow_forward

Managerial Economics: Applications, Strategies an...EconomicsISBN:9781305506381Author:James R. McGuigan, R. Charles Moyer, Frederick H.deB. HarrisPublisher:Cengage Learning

Managerial Economics: Applications, Strategies an...EconomicsISBN:9781305506381Author:James R. McGuigan, R. Charles Moyer, Frederick H.deB. HarrisPublisher:Cengage Learning