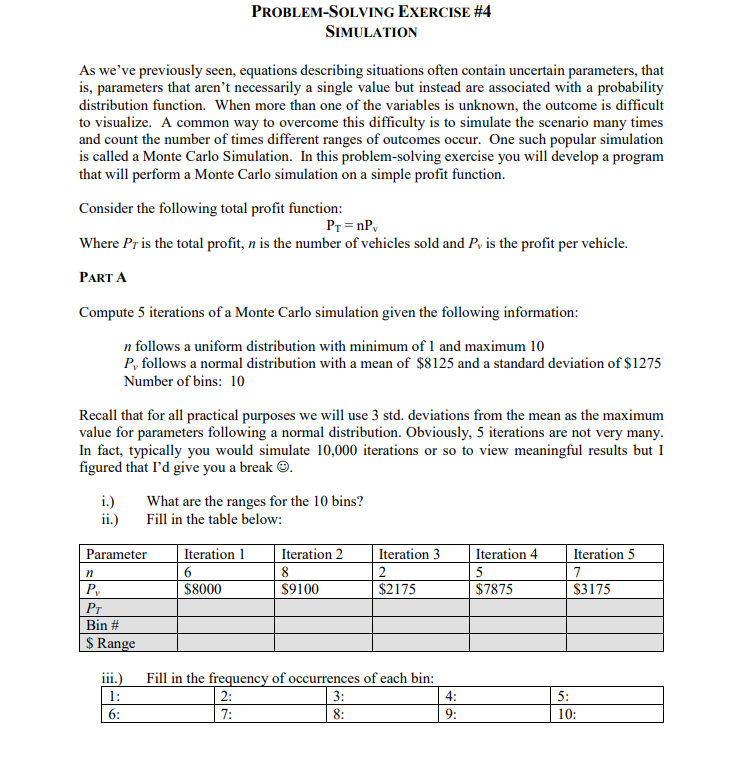

As we've previously seen, equations describing situations often contain uncertain parameters, that is, parameters that aren't necessarily a single value but instead are associated with a probability distribution function. When more than one of the variables is unknown, the outcome is difficult to visualize. A common way to overcome this difficulty is to simulate the scenario many times and count the number of times different ranges of outcomes occur. One such popular simulation is called a Monte Carlo Simulation. In this problem-solving exercise you will develop a program that will perform a Monte Carlo simulation on a simple profit function. Consider the following total profit function: PT=nPy Where Pr is the total profit, n is the number of vehicles sold and P, is the profit per vehicle. PART A Compute 5 iterations of a Monte Carlo simulation given the following information: n follows a uniform distribution with minimum of 1 and maximum 10 P, follows a normal distribution with a mean of $8125 and a standard deviation of $1275 Number of bins: 10 i.) ii.) PROBLEM-SOLVING EXERCISE #4 Recall that for all practical purposes we will use 3 std. deviations from the mean as the maximum value for parameters following a normal distribution. Obviously, 5 iterations are not very many. In fact, typically you would simulate 10,000 iterations or so to view meaningful results but I figured that I'd give you a break Ⓒ. SIMULATION Parameter n Py PT Bin # $ Range iii.) 1: 6: What are the ranges for the 10 bins? Fill in the table below: Iteration 1 6 $8000 Iteration 2 8 $9100 Iteration 3 2 $2175 Fill in the frequency of occurrences of each bin: 2: 7: 3: 8: 4: 9: Iteration 4 5 $7875 Iteration 5 7 $3175 5: 10:

As we've previously seen, equations describing situations often contain uncertain parameters, that is, parameters that aren't necessarily a single value but instead are associated with a probability distribution function. When more than one of the variables is unknown, the outcome is difficult to visualize. A common way to overcome this difficulty is to simulate the scenario many times and count the number of times different ranges of outcomes occur. One such popular simulation is called a Monte Carlo Simulation. In this problem-solving exercise you will develop a program that will perform a Monte Carlo simulation on a simple profit function. Consider the following total profit function: PT=nPy Where Pr is the total profit, n is the number of vehicles sold and P, is the profit per vehicle. PART A Compute 5 iterations of a Monte Carlo simulation given the following information: n follows a uniform distribution with minimum of 1 and maximum 10 P, follows a normal distribution with a mean of $8125 and a standard deviation of $1275 Number of bins: 10 i.) ii.) PROBLEM-SOLVING EXERCISE #4 Recall that for all practical purposes we will use 3 std. deviations from the mean as the maximum value for parameters following a normal distribution. Obviously, 5 iterations are not very many. In fact, typically you would simulate 10,000 iterations or so to view meaningful results but I figured that I'd give you a break Ⓒ. SIMULATION Parameter n Py PT Bin # $ Range iii.) 1: 6: What are the ranges for the 10 bins? Fill in the table below: Iteration 1 6 $8000 Iteration 2 8 $9100 Iteration 3 2 $2175 Fill in the frequency of occurrences of each bin: 2: 7: 3: 8: 4: 9: Iteration 4 5 $7875 Iteration 5 7 $3175 5: 10:

Database System Concepts

7th Edition

ISBN:9780078022159

Author:Abraham Silberschatz Professor, Henry F. Korth, S. Sudarshan

Publisher:Abraham Silberschatz Professor, Henry F. Korth, S. Sudarshan

Chapter1: Introduction

Section: Chapter Questions

Problem 1PE

Related questions

{kind=link}

Question

Transcribed Image Text:As we've previously seen, equations describing situations often contain uncertain parameters, that

is, parameters that aren't necessarily a single value but instead are associated with a probability

distribution function. When more than one of the variables is unknown, the outcome is difficult

to visualize. A common way to overcome this difficulty is to simulate the scenario many times

and count the number of times different ranges of outcomes occur. One such popular simulation

is called a Monte Carlo Simulation. In this problem-solving exercise you will develop a program

that will perform a Monte Carlo simulation on a simple profit function.

Consider the following total profit function:

PT=nPv

Where Pr is the total profit, n is the number of vehicles sold and P, is the profit per vehicle.

PART A

Compute 5 iterations of a Monte Carlo simulation given the following information:

n follows a uniform distribution with minimum of 1 and maximum 10

P, follows a normal distribution with a mean of $8125 and a standard deviation of $1275

Number of bins: 10

i.)

ii.)

Parameter

Recall that for all practical purposes we will use 3 std. deviations from the mean as the maximum

value for parameters following a normal distribution. Obviously, 5 iterations are not very many.

In fact, typically you would simulate 10,000 iterations or so to view meaningful results but I

figured that I'd give you a break Ⓒ.

n

Py

PROBLEM-SOLVING EXERCISE #4

PT

Bin #

$ Range

SIMULATION

iii.)

1:

6:

Iteration 1

What are the ranges for the 10 bins?

Fill in the table below:

$8000

Iteration 2

8

$9100

Iteration 3

$2175

Fill in the frequency of occurrences of each bin:

2:

3:

7:

8:

4:

9:

Iteration 4

$7875

5:

Iteration 5

7

$3175

10:

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution!

Trending now

This is a popular solution!

Step by step

Solved in 6 steps with 2 images

Follow-up Questions

Read through expert solutions to related follow-up questions below.

Follow-up Question

Transcribed Image Text:PART B

Write the following three methods and include in the Part D code listing:

public int GetRandomUniform(int min, int max)

This method returns a random number from a uniform distribution between min and max.

public double GetRandomNormal(double mean, double stddev)

This method returns a random number from a normal distribution with a mean of mean and standard

deviation of stddev

public int GetBinIndex(double mini, double maxi, int numbins, double valuetobin)

This method returns the Bin Index given an input minimum of mini, input maximum of maxi,

numbins number of bins, and a value to bin of valuetobin

PART C

Include the methods created in part B to develop a Visual C# .NET program that will simulate the

basic profit calculation, PT = nPv, where n follows a uniform distribution, P, follows a normal

distribution, and the user can input the number of bins and number of iterations. The user must

also input the min and max for n and the mean and standard deviation for Py. Finally, the user can

click a button and the results will be graphed on a bar chart using the Microsoft Chart Control and

the average total profit (PT) will be displayed in a textbox. Turn in a screen shot of the resulting

chart using:

1. Iterations: 10000 Bins: 5

2. Iterations: 10000 Bins: 10

3. Iterations: 10000 Bins: 10

That's three screen shots.

PART D

n-min: 1

n-min: 1

n-min: 1

n-max: 10

n-max: 10

n-max: 10

P-mean: 8250 Py-stddev: 1780

Py-mean: 8250 Py-stddev: 1780

P-mean: 5500

P-stddev: 1200

Extend the Visual C# .NET program developed in part C to simulate the basic profit calculation,

Pr=nPv, where the user can select either a uniform or normal distribution for n using radio buttons

and then must input the appropriate parameters (min and max if they select uniform, mean and

standard deviation if they select normal) and they can similarly select either a uniform or normal

distribution for P, with appropriate parameters depending on the selection. Of course, the user

will input the number of bins and number of iterations. Finally, the user can click a button and the

results will be graphed on a bar chart using the Microsoft Chart Control and the average total profit

(PT) will be displayed in a textbox. Also include in the program any necessary input validation for

all input values. Turn in a listing of the code and a screen shot of the resulting chart using:

1. Iterations: 10000 Bins: 5

2. Iterations: 10000 Bins: 10

n-min: 2

n-mean: 7

n- mean: 12

3. Iterations: 10000 Bins: 10

That's three screen shots and a listing of the code.

n-max: 10 P-mean: 7250

n-stddev: 2 P-min: 1250

n- stddev: 3

Py-min: 2375

P-stddev: 1950

P-max: 6500

Py-max: 5450

Solution

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, computer-science and related others by exploring similar questions and additional content below.Recommended textbooks for you

Database System Concepts

Computer Science

ISBN:

9780078022159

Author:

Abraham Silberschatz Professor, Henry F. Korth, S. Sudarshan

Publisher:

McGraw-Hill Education

Starting Out with Python (4th Edition)

Computer Science

ISBN:

9780134444321

Author:

Tony Gaddis

Publisher:

PEARSON

Digital Fundamentals (11th Edition)

Computer Science

ISBN:

9780132737968

Author:

Thomas L. Floyd

Publisher:

PEARSON

Database System Concepts

Computer Science

ISBN:

9780078022159

Author:

Abraham Silberschatz Professor, Henry F. Korth, S. Sudarshan

Publisher:

McGraw-Hill Education

Starting Out with Python (4th Edition)

Computer Science

ISBN:

9780134444321

Author:

Tony Gaddis

Publisher:

PEARSON

Digital Fundamentals (11th Edition)

Computer Science

ISBN:

9780132737968

Author:

Thomas L. Floyd

Publisher:

PEARSON

C How to Program (8th Edition)

Computer Science

ISBN:

9780133976892

Author:

Paul J. Deitel, Harvey Deitel

Publisher:

PEARSON

Database Systems: Design, Implementation, & Manag…

Computer Science

ISBN:

9781337627900

Author:

Carlos Coronel, Steven Morris

Publisher:

Cengage Learning

Programmable Logic Controllers

Computer Science

ISBN:

9780073373843

Author:

Frank D. Petruzella

Publisher:

McGraw-Hill Education