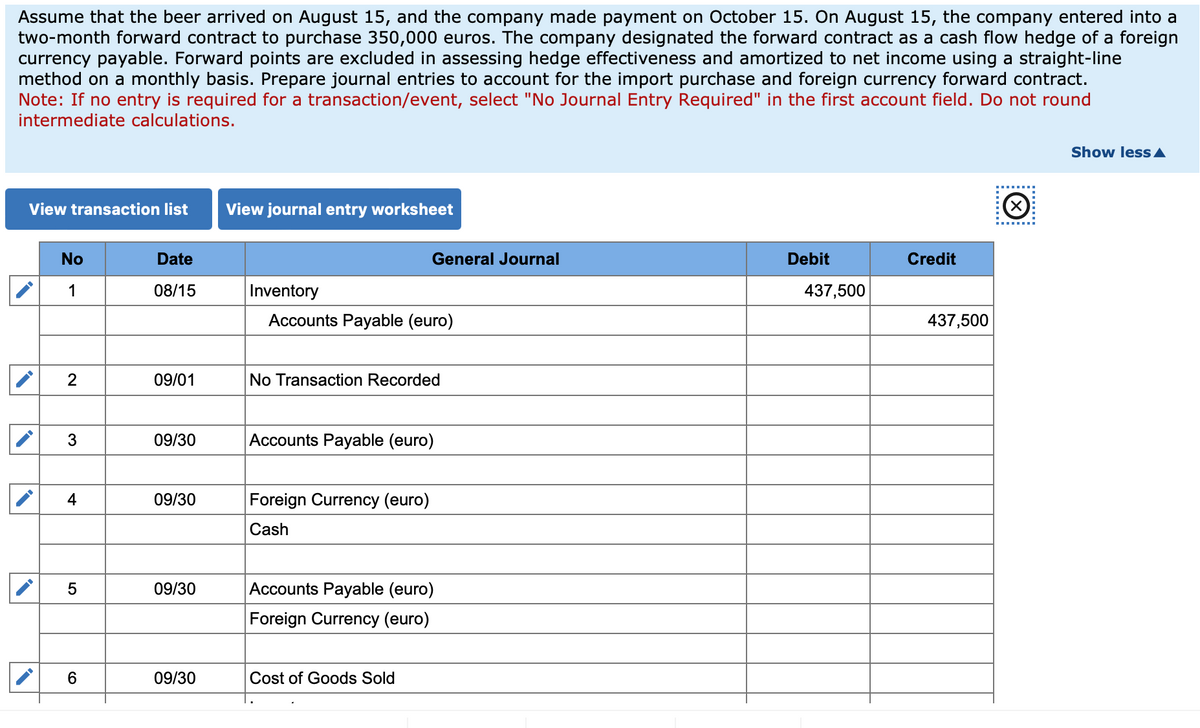

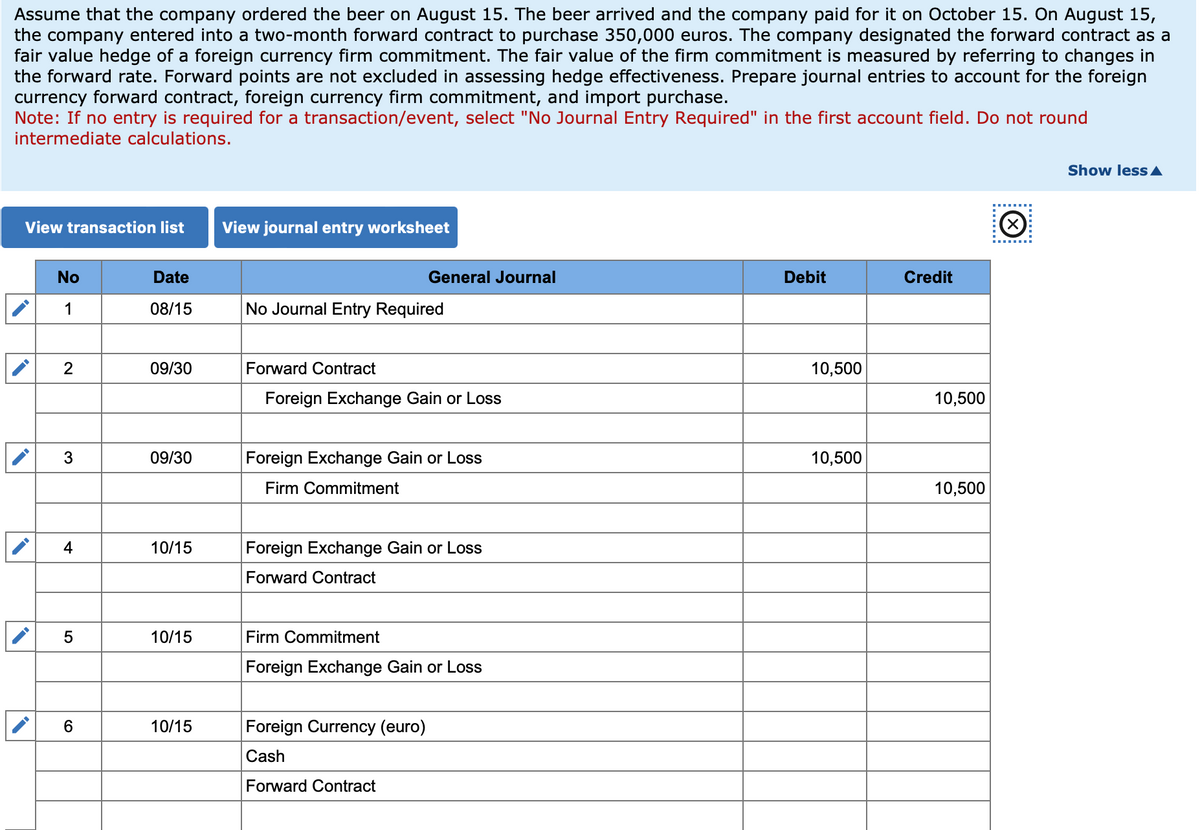

Assume that the beer arrived on August 15, and the company made payment on October 15. On August 15, the company entered into a two-month forward contract to purchase 350,000 euros. The company designated the forward contract as a cash flow hedge of a foreign currency payable. Forward points are excluded in assessing hedge effectiveness and amortized to net income using a straight-line method on a monthly basis. Prepare journal entries to account for the import purchase and foreign currency forward contract. Note: If no entry is required for a transaction/event, select "No Journal Entry Required" in the first account field. Do not round intermediate calculations. (☑ ........ View transaction list View journal entry worksheet No Date 1 08/15 Inventory Accounts Payable (euro) General Journal Debit Credit 437,500 437,500 2 09/01 No Transaction Recorded 3 09/30 Accounts Payable (euro) 4 09/30 Foreign Currency (euro) Cash 5 09/30 Accounts Payable (euro) Foreign Currency (euro) 6 09/30 Cost of Goods Sold Show less▲ Assume that the company ordered the beer on August 15. The beer arrived and the company paid for it on October 15. On August 15, the company entered into a two-month forward contract to purchase 350,000 euros. The company designated the forward contract as a fair value hedge of a foreign currency firm commitment. The fair value of the firm commitment is measured by referring to changes in the forward rate. Forward points are not excluded in assessing hedge effectiveness. Prepare journal entries to account for the foreign currency forward contract, foreign currency firm commitment, and import purchase. Note: If no entry is required for a transaction/event, select "No Journal Entry Required" in the first account field. Do not round intermediate calculations. View transaction list View journal entry worksheet No Date General Journal Debit Credit 1 08/15 No Journal Entry Required 2 09/30 Forward Contract Foreign Exchange Gain or Loss 3 09/30 Foreign Exchange Gain or Loss Firm Commitment 4 10/15 Foreign Exchange Gain or Loss Forward Contract 5 10/15 Firm Commitment Foreign Exchange Gain or Loss 6 10/15 Foreign Currency (euro) Cash Forward Contract ........ 10,500 10,500 10,500 10,500 Show less▲

Pacifico Company, a U.S.-based importer of beer and wine, purchased 1,400 cases of Oktoberfest-style beer from a German supplier for 350,000 euros. Relevant U.S. dollar exchange rates for the euro are as follows:

| Date | Spot Rate | Forward Rate to October 15 | Call Option Premium for October 15 (strike price $1.25) |

|---|---|---|---|

| August 15 | $ 1.25 | $ 1.31 | $ 0.05 |

| September 30 | 1.30 | 1.34 | 0.06 |

| October 15 | 1.33 | 1.33 (spot) | N/A |

The company closes its books and prepares third-quarter financial statements on September 30.

Required:

-

Assume that the beer arrived on August 15, and the company made payment on October 15. There was no attempt to hedge the exposure to foreign exchange risk. Prepare

journal entries to account for this import purchase. -

Assume that the beer arrived on August 15, and the company made payment on October 15. On August 15, the company entered into a two-month forward contract to purchase 350,000 euros. The company designated the forward contract as a

cash flow hedge of a foreign currency payable. Forward points are excluded in assessing hedge effectiveness and amortized to net income using a straight-line method on a monthly basis. Prepare journal entries to account for the import purchase and foreign currency forward contract. -

Assume that the company ordered the beer on August 15. The beer arrived and the company paid for it on October 15. On August 15, the company entered into a two-month forward contract to purchase 350,000 euros. The company designated the forward contract as a fair value hedge of a foreign currency firm commitment. The fair value of the firm commitment is measured by referring to changes in the forward rate. Forward points are not excluded in assessing hedge effectiveness. Prepare journal entries to account for the foreign currency forward contract, foreign currency firm commitment, and import purchase.

-

Assume that the company ordered the beer on August 15. The beer arrived and the company paid for it on October 15. On August 15, the company purchased a two-month call option on 350,000 euros. The company designated the option as a fair value hedge of a foreign currency firm commitment. The fair value of the firm commitment is measured by referring to changes in the spot rate. The time value of the option is excluded from the assessment of hedge effectiveness, and the change in time value is recognized in net income over the life of the option. Prepare journal entries to account for the foreign currency option, foreign currency firm commitment, and import purchase.

-

Assume that, on August 15, the company

forecasted the purchase of beer on October 15. On August 15, the company acquired a two-month call option on 350,000 euros. The company designated the option as a cash value hedge of a forecasted foreign currency transaction. The time value of the option is excluded from the assessment of hedge effectiveness, and the change in time value is recognized in net income over the life of the option. Prepare journal entries to account for the foreign currency option and import purchase.

Trending now

This is a popular solution!

Step by step

Solved in 2 steps