Required: a) As part of your risk assessment procedures for Healthcare Bhd, identify and provide a possible explanation for the unusual changes in the income statement. b) Confirmation of the end-of-year bank and account receivables balances are important audit procedures. Discuss the audit objectives pertaining to the procedures.

Required: a) As part of your risk assessment procedures for Healthcare Bhd, identify and provide a possible explanation for the unusual changes in the income statement. b) Confirmation of the end-of-year bank and account receivables balances are important audit procedures. Discuss the audit objectives pertaining to the procedures.

Financial Reporting, Financial Statement Analysis and Valuation

8th Edition

ISBN:9781285190907

Author:James M. Wahlen, Stephen P. Baginski, Mark Bradshaw

Publisher:James M. Wahlen, Stephen P. Baginski, Mark Bradshaw

Chapter6: Accounting Quality

Section: Chapter Questions

Problem 10QE: Checkpoint Systems is a leading provider of source tagging, handheld labeling systems, retail...

Related questions

Question

Please solve all questions please

Sales cycle

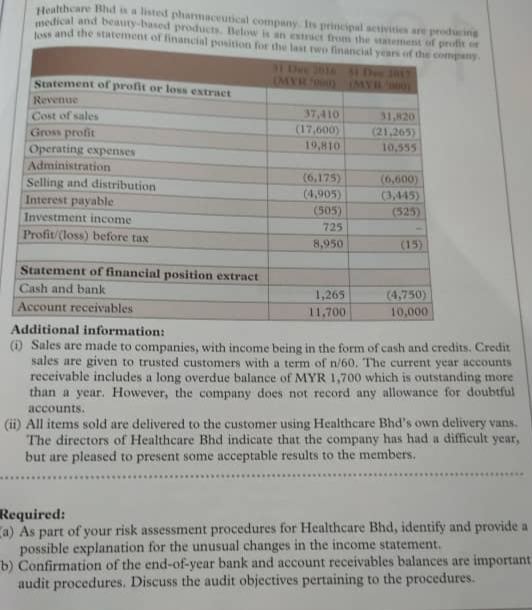

Transcribed Image Text:Healthcare Bhd is a listed pharmaceutical comnpany. Its principal sctivities are producins

edical and beauty-based products. Below is an extract from the statement of profit ot

Nast and the statement of financial position for the last two financial years of the company.

31 Dee 2614 De 7

(MYR 0) IMYR

Statement of profit or loss extract

Revenue

37,410

(17,600)

Cost of sales

31,820

Gross profit

(21,265)

19,810

10,555

Operating expenses

Administration

Selling and distribution

Interest payable

(6,175)

(6,600)

(4,905)

(3,445)

(505)

(525)

Investment income

725

Profit/(loss) before tax

8,950

(15)

Statement of financial position extract

Cash and bank

1,265

(4,750)

Account receivables

11,700

10,000

Additional information:

(i) Sales are made to companies, with income being in the form of cash and credits. Credit

sales are given to trusted customers with a term of n/60. The current year accounts

receivable includes a long overdue balance of MYR 1,700 which is outstanding more

than a year. However, the company does not record any allowance for doubtful

accounts.

(ii) All items sold are delivered to the customer using Healthcare Bhd's own delivery vans.

The directors of Healthcare Bhd indicate that the company has had a difficult year,

but are pleased to present some acceptable results to the members.

Required:

a) As part of your risk assessment procedures for Healthcare Bhd, identify and provide a

possible explanation for the unusual changes in the income statement.

b) Confirmation of the end-of-year bank and account receivables balances are important

audit procedures. Discuss the audit objectives pertaining to the procedures.

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution!

Trending now

This is a popular solution!

Step by step

Solved in 2 steps

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, accounting and related others by exploring similar questions and additional content below.Recommended textbooks for you

Financial Reporting, Financial Statement Analysis…

Finance

ISBN:

9781285190907

Author:

James M. Wahlen, Stephen P. Baginski, Mark Bradshaw

Publisher:

Cengage Learning

Financial Reporting, Financial Statement Analysis…

Finance

ISBN:

9781285190907

Author:

James M. Wahlen, Stephen P. Baginski, Mark Bradshaw

Publisher:

Cengage Learning