Videos

Stock Dividends and Stock Splits

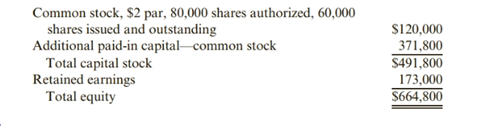

The balance sheet of Castle Corporation includes the following stockholders’ equity section:

Required:

- Assume that Castle issued 60,000 shares for cash at the inception of the corporation and that no new shares have been issued since. Determine how much cash was received for the shares issued at inception.

- Assume that Castle issued 30,000 shares for cash at the inception of the corporation and subsequently declared a 2-for-l stock split. Determine how much cash was received for the shares issued at inception.

- Assume that Castle issued 57,000 shares for cash at the inception of the corporation and that the remaining 3,000 shares were issued as the result of stock dividends when the stock was selling for $53 per share. Determine how much cash was received for the shares issued at inception.

(a)

Introduction:

Common stock is issued by the company to raise finance using equity. It isissued to the investors (who are regarded as stockholders or shareholders, once common stock are issued to them) with no obligation to pay dividend periodically. Common stock is also referred to as common shares.

To calculate:

Cash received on issue of shares.

Answer to Problem 72E

$491,800 was received as cash at the inception of corporation.

Explanation of Solution

Given:

The following equity statement:

| Particulars | $ |

| Common stock, $2 par, 80,000 shares authorized, 60,000 issued and outstanding | 120,000 |

| (+) Additional Paid-in capital − common stock | 371,800 |

| Total Capital Stock | 491,800 |

| Retained Earnings | 173,000 |

| Total Stockholders’ equity | 664,800 |

At the time of inception:

No. of shares issued = 60,000

Par value = $2

Total Par Value of shares issued =

Total Par Value of shares issued =

Total Par Value of shares issued = $120,000

Additional Paid in capital −common stock = $371,800

Journal Entries

| Date | Particulars | Debit ($) | Credit ($) |

| No date given | Cash Dr. Common Stock Additional Paid in capital −common stock (Issue of shares at the inception of corporation.) |

491,800 | 120,000 371,800 |

(b)

Introduction:

A common stock is issued by the company to raise finance using equity. It is issued to the investors (who are regarded as stockholders or shareholders, once common stock is issued to them) with no obligation to pay dividend periodically. Common stock is also referred to as common shares.

To calculate:

Cash received on issue of shares and split stock.

Answer to Problem 72E

$467,210 was received as cash at the inception of corporation.

Explanation of Solution

Given:

The following equity statement:

| Particulars | $ |

| Common stock, $2 par, 80,000 shares authorized, 60,000 issued and outstanding | 120,000 |

| (+) Additional Paid-in capital − common stock | 371,800 |

| Total Capital Stock | 491,800 |

| Retained Earnings | 173,000 |

| Total Stockholders’ equity | 664,800 |

At the time of inception:

No. of shares issued = 60,000

Par value = $2

Total Par Value of shares issued =

Total Par Value of shares issued =

Total Par Value of shares issued = $120,000

Additional Paid in capital −common stock = $371,800

Journal Entries

| Date | Particulars | Debit ($) | Credit ($) |

| No date given | Cash Dr. Common Stock Additional Paid in capital −common stock (Issue of shares at the inception of corporation.) |

491,800 | 120,000 371,800 |

Before stock split:

No. of shares issued = 60,000

Par value = $2

After, 2-for1 stock split:

No. of shares issued =

No. of shares issued = 120,000

Par value =

Par value = $1

No journal entry is recorded on stock. Though,the common stock capital remains same, only its structure i.e. no. of shares outstanding and par value of shares change.

Thus, the cash received from issues of shares and immediate stock split will be same as the cash received from issues of shares.

(c)

Introduction:

A common stock is issued by the company to raise finance using equity. It is issued to the investors (who are regarded as stockholders or shareholders, once common stock is issued to them) with no obligation to pay dividend periodically. Common stock is also referred to as common shares.

To calculate:

Cash received on issues of shares and stock dividend thereof.

Answer to Problem 72E

$491,800 was received as cash at the inception of corporation.

Explanation of Solution

Given:

The following equity statement:

| Particulars | $ |

| Common stock, $2 par, 80,000 shares authorized, 60,000 issued and outstanding | 120,000 |

| (+) Additional Paid-in capital − common stock | 371,800 |

| Total Capital Stock | 491,800 |

| Retained Earnings | 173,000 |

| Total Stockholder’s equity | 664,800 |

At the time of inception:

No. of shares issued = 57,000

Par value = $2

Total Par Value of shares issued =

Total Par Value of shares issued =

Total Par Value of shares issued = $114,000

Additional Paid in capital (for 60,000) common stock = $371,800

Additional Paid in capital (for 57,000) common stock =

Additional Paid in capital (for 57,000) common stock = $353,210

Journal Entries

| Date | Particulars | Debit ($) | Credit ($) |

| No date given | Cash Dr. Common Stock Additional Paid in capital −common stock (Issue of shares at the inception of corporation.) |

467,210 | 114,000 353,210 |

Stock Dividend = 3,000 shares

Market Value of shares = $53

Par Value of shares = $2

Total Par value of stock dividend =

Total Par value of stock dividend =

Total Par value of stock dividend = $6,000

Total Market value of stock dividend =

Total Market value of stock dividend =

Total Market value of stock dividend = $159,000

Additional Paid in capital = Total Market value of stock dividend - Total Par value

Additional Paid in capital = $159,000 - $6,000

Additional Paid in capital = $153,000

Journal Entries

| Date | Particulars | Debit ($) | Credit ($) |

| No date given | Retained Earnings Dr. Common Stock Additional Paid in capital −common stock (Issue of shares at the inception of corporation.) |

159,000 | 6,000 153,000 |

The first effect of both dividends (cash and stock) is on Retained Earnings of the company. If stock dividend is paid then, the second effect is on common stock and additional paid in capital account as new shares are issued as dividends which further increase the balance of these accounts.

Thus, stock dividend don’t involve any cash transaction and the amount received at the time of inception remains $467,210 (i.e. the amount received on issues of shares).

Want to see more full solutions like this?

Chapter 10 Solutions

Cornerstones of Financial Accounting

- Selected stock transactions The following selected accounts appear in the ledger of Parks Construction Inc. at the beginning of the current year: During the year, the corporation completed a number of transactions affecting the stockholders equity. They are summarized as follows: a. Issued 400,000 shares of common stock at 11, receiving cash. b. Issued 5,000 shares of preferred 2% stock at 90. c. Purchased 150,000 shares of treasury common for 10 per share. d. Sold 80,000 shares of treasury common for 13 per share. e. Sold 20,000 shares of treasury common for 9 per share. f. Declared cash dividends of 1.50 per share on preferred stock and 0.06 per share on common stock. g. Paid the cash dividends. Instructions Journalize the entries to record the transactions. Identify each entry by letter.arrow_forwardSTOCK SUBSCRIPTIONS AND TREASURY STOCK Nash Roth formed a corporation and had the following organization costs and stock transactions during the year: June 30 Incurred the following costs of incorporation: Incorporation fees 800 Attorney's fees 9,000 Promotion fees 8,000 July 15 Issued 7,000 shares of 10 par common stock for 73,000 cash. Aug. 1 Received subscriptions for 8,000 shares of 10 par common stock for 81,500. 15 Issued 16,000 shares of 10 par common stock in exchange for a building and fixtures with a fair market value of 165,000. 31 Received a payment of 51,500 for the common stock subscription. Sept. 3 Purchased 2,000 shares of its own 10 par common stock for 11 a share. 18 Received the balance in full for the common stock subscription and issued the stock. 30 Sold 800 shares of its treasury stock for 11.50 a share. Oct. 15 Issued 3,000 shares of 40 par, 5% preferred stock in exchange for land with a fair market value of 125,000. 31 Sold 400 shares of its treasury stock for 10.75 a share. REQUIRED Prepare journal entries for these transactions.arrow_forwardStock Dividend Comparison Although Oriole Company has enough retained earnings legally to declare a dividend, its working capital is low. The board of directors is considering a stock dividend instead of a cash dividend. The common stock is currently selling at 34 per share. The following is Orioles current shareholders equity: Required: 1. Assuming a 15% stock dividend is declared and issued, prepare the shareholders equity section immediately after the date of issuance. 2. Assuming, instead, that a 30% stock dividend is declared and issued, prepare the shareholders equity section immediately after the date of issuance. 3. Next Level What unusual result do you notice when you compare your answers from Requirement 1 with Requirement 2? From a theoretical standpoint, how might this have been avoided?arrow_forward

- STOCK SUBSCRIPTIONS AND TREASURY STOCK Rogers Hart formed a corporation and had the following organization costs and stock transactions during the year: June 30 Incurred the following costs of incorporation: July 15 Issued 8,000 shares of 10 par common stock for 82,000 cash. Aug. 1 Received subscriptions for 10,000 shares of 10 par common stock for 101,500. 15 Issued 10,000 shares of 10 par common stock in exchange for a building with a fair market value of 104,800. 31 Received a payment of 51,500 for the common stock subscription. Sept. 3 Purchased 1,000 shares of its own 10 par common stock for 11 a share. 18 Received the balance in full for the common stock subscription and issued the stock. 30 Sold 500 shares of its treasury stock for 11.70 a share. Oct. 15 Issued 4,000 shares of 25 par, 8 % preferred stock in exchange for land with a fair market value of 105,000. 31 Sold 500 shares of its treasury stock for 10.50 a share. REQUIRED Prepare journal entries for these transactions.arrow_forwardEffective May 1, the shareholders of Baltimore Corporation approved a 2-for-1 split of the companys common stock and an increase in authorized common shares from 100,000 shares (par value 20 per share) to 200,000 shares (par value 10 per share). Baltimores shareholders equity items immediately before issuance of the stock split shares were as follows: What should be the balances in Baltimores Additional Paid-in Capital and Retained Earnings accounts immediately after the stock split is effected?arrow_forwardNutritious Pet Food Companys board of directors declares a cash dividend of $1.00 per common share on November 12. On this date, the company has issued 12,000 shares but 2,000 shares are held as treasury shares. What is the journal entry to record the declaration of this dividend?arrow_forward

- Treasury Stock Transactions Garrett Inc. had no treasury stock at the beginning of the year. During February, Garrett purchased 12,600 shares of treasury stock at $23 per share. In May, Garrett sold 4,500 of the treasury shares for $25 per share. In November, Garrett sold the remaining treasury shares for $18 per share. Required: Prepare journal entries for the February, May, and November treasury stock transactions.arrow_forwardCASH DIVIDENDS, STOCK DIVIDEND, AND STOCK SPLIT During the year ended December 31, 20--, Baggio Company completed the following transactions: Apr. 15 Declared a semiannual dividend of 0.65 per share on preferred stock and 0.45 per share on common stock to shareholders of record on May 5, payable on May 10. Currently, 6,000 shares of 50 par preferred stock and 70,000 shares of 1 par common stock are outstanding. May 10 Paid the cash dividends. Oct. 15 Declared semiannual dividend of 0.65 per share on preferred stock and 0.45 per share on common stock to shareholders of record on November 5, payable on November 20. Nov. 20 Paid the cash dividends. 22 Declared a 10% stock dividend to shareholders of record on December 8, distributable on December 16. Market value of the common stock was estimated at 15 per share. Dec. 16 Issued certificates for common stock dividend. 20 Board of directors declared a two-for-one common stock split. REQUIRED Prepare journal entries for the transactions.arrow_forward

Cornerstones of Financial AccountingAccountingISBN:9781337690881Author:Jay Rich, Jeff JonesPublisher:Cengage Learning

Cornerstones of Financial AccountingAccountingISBN:9781337690881Author:Jay Rich, Jeff JonesPublisher:Cengage Learning College Accounting, Chapters 1-27AccountingISBN:9781337794756Author:HEINTZ, James A.Publisher:Cengage Learning,

College Accounting, Chapters 1-27AccountingISBN:9781337794756Author:HEINTZ, James A.Publisher:Cengage Learning, Principles of Accounting Volume 1AccountingISBN:9781947172685Author:OpenStaxPublisher:OpenStax College

Principles of Accounting Volume 1AccountingISBN:9781947172685Author:OpenStaxPublisher:OpenStax College Intermediate Accounting: Reporting And AnalysisAccountingISBN:9781337788281Author:James M. Wahlen, Jefferson P. Jones, Donald PagachPublisher:Cengage Learning

Intermediate Accounting: Reporting And AnalysisAccountingISBN:9781337788281Author:James M. Wahlen, Jefferson P. Jones, Donald PagachPublisher:Cengage Learning Financial AccountingAccountingISBN:9781337272124Author:Carl Warren, James M. Reeve, Jonathan DuchacPublisher:Cengage Learning

Financial AccountingAccountingISBN:9781337272124Author:Carl Warren, James M. Reeve, Jonathan DuchacPublisher:Cengage Learning Financial And Managerial AccountingAccountingISBN:9781337902663Author:WARREN, Carl S.Publisher:Cengage Learning,

Financial And Managerial AccountingAccountingISBN:9781337902663Author:WARREN, Carl S.Publisher:Cengage Learning,