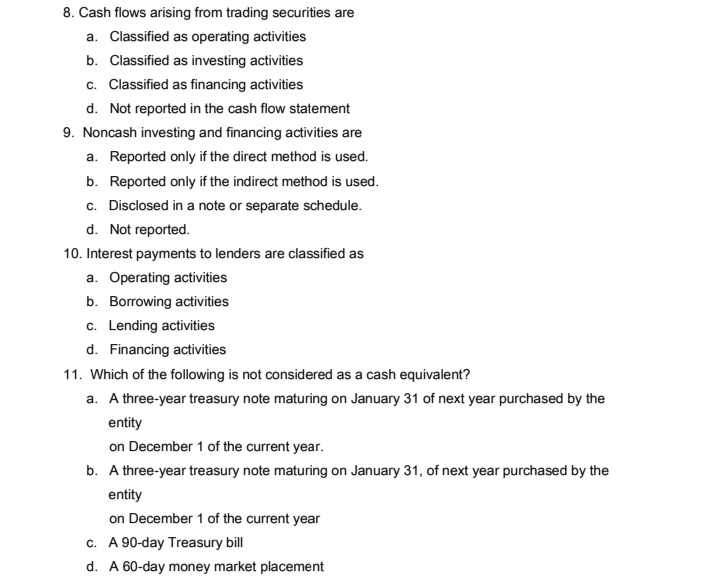

8. Cash flows arising from trading securities are a. Classified as operating activities b. Classified as investing activities c. Classified as financing activities d. Not reported in the cash flow statement

8. Cash flows arising from trading securities are a. Classified as operating activities b. Classified as investing activities c. Classified as financing activities d. Not reported in the cash flow statement

Auditing: A Risk Based-Approach (MindTap Course List)

11th Edition

ISBN:9781337619455

Author:Karla M Johnstone, Audrey A. Gramling, Larry E. Rittenberg

Publisher:Karla M Johnstone, Audrey A. Gramling, Larry E. Rittenberg

Chapter10: Auditing Cash, Marketable Securities, And Complex Financial Instruments

Section: Chapter Questions

Problem 3RQSC: Match the following assertions with their associated description: (a) existence/occurrence, (b)...

Related questions

Question

Answer

Transcribed Image Text:8. Cash flows arising from trading securities are

a. Classified as operating activities

b. Classified as investing activities

c. Classified as financing activities

d. Not reported in the cash flow statement

9. Noncash investing and financing activities are

a. Reported only if the direct method is used.

b. Reported only if the indirect method is used.

c. Disclosed in a note or separate schedule.

d. Not reported.

10. Interest payments to lenders are classified as

a. Operating activities

b. Borrowing activities

c. Lending activities

d. Financing activities

11. Which of the fllowing is not considered as a cash equivalent?

a. A three-year treasury note maturing on January 31 of next year purchased by the

entity

on December 1 of the current year.

b. A three-year treasury note maturing on January 31, of next year purchased by the

entity

on December 1 of the current year

c. A 90-day Treasury bill

d. A 60-day money market placement

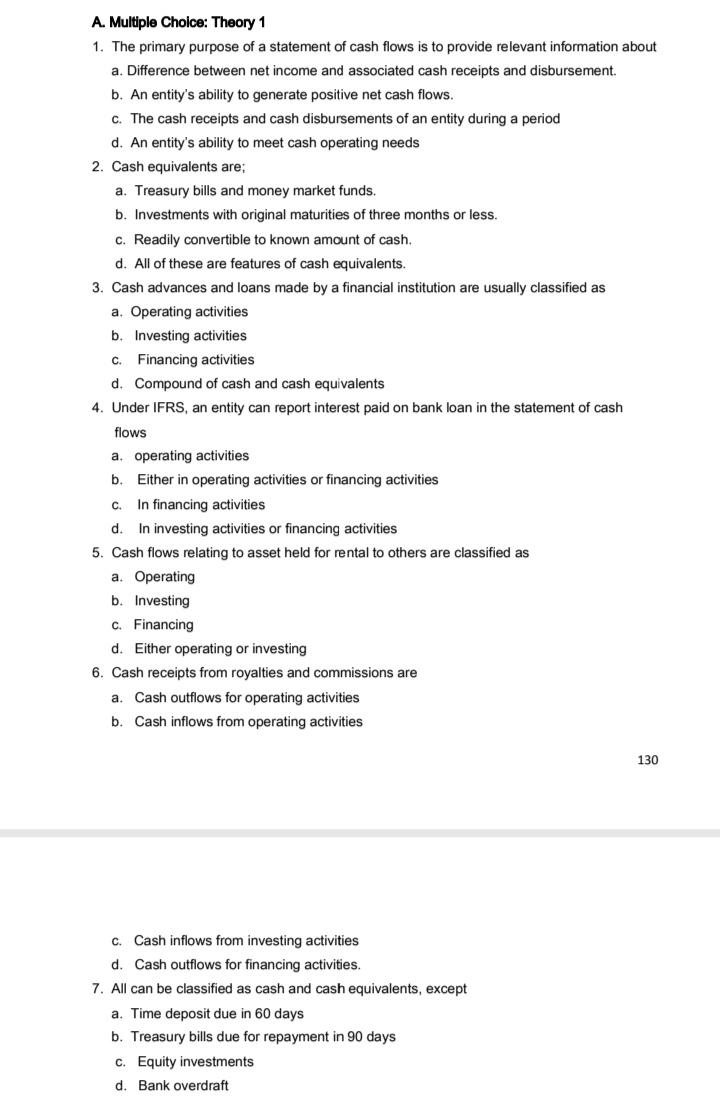

Transcribed Image Text:A. Multiple Choice: Theory 1

1. The primary purpose of a statement of cash flows is to provide relevant information about

a. Difference between net income and associated cash receipts and disbursement.

b. An entity's ability to generate positive net cash flows.

c. The cash receipts and cash disbursements of an entity during a period

d. An entity's ability to meet cash operating needs

2. Cash equivalents are;

a. Treasury bills and money market funds.

b. Investments with original maturities of three months or less.

c. Readily convertible to known amount of cash.

d. All of these are features of cash equivalents.

3. Cash advances and loans made by a financial institution are usually classified as

a. Operating activities

b. Investing activities

c. Financing activities

d. Compound of cash and cash equivalents

4. Under IFRS, an entity can report interest paid on bank loan in the statement of cash

flows

a. operating activities

b.

Either in operating activities or financing activities

In financing activities

d. In investing activities or financing activities

5. Cash flows relating to asset held for rental to others are classified as

C.

a. Operating

b. Investing

c. Financing

d. Either operating or investing

6. Cash receipts from royalties and commissions are

a. Cash outflows for operating activities

b. Cash inflows from operating activities

130

C.

Cash inflows from investing activities

d. Cash outflows for financing activities.

7. All can be classified as cash and cash equivalents, except

a. Time deposit due in 60 days

b. Treasury bills due for repayment in 90 days

c. Equity investments

d. Bank overdraft

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

Step by step

Solved in 2 steps

Recommended textbooks for you

Auditing: A Risk Based-Approach (MindTap Course L…

Accounting

ISBN:

9781337619455

Author:

Karla M Johnstone, Audrey A. Gramling, Larry E. Rittenberg

Publisher:

Cengage Learning

Financial Accounting: The Impact on Decision Make…

Accounting

ISBN:

9781305654174

Author:

Gary A. Porter, Curtis L. Norton

Publisher:

Cengage Learning

Intermediate Accounting: Reporting And Analysis

Accounting

ISBN:

9781337788281

Author:

James M. Wahlen, Jefferson P. Jones, Donald Pagach

Publisher:

Cengage Learning

Auditing: A Risk Based-Approach (MindTap Course L…

Accounting

ISBN:

9781337619455

Author:

Karla M Johnstone, Audrey A. Gramling, Larry E. Rittenberg

Publisher:

Cengage Learning

Financial Accounting: The Impact on Decision Make…

Accounting

ISBN:

9781305654174

Author:

Gary A. Porter, Curtis L. Norton

Publisher:

Cengage Learning

Intermediate Accounting: Reporting And Analysis

Accounting

ISBN:

9781337788281

Author:

James M. Wahlen, Jefferson P. Jones, Donald Pagach

Publisher:

Cengage Learning

Cornerstones of Financial Accounting

Accounting

ISBN:

9781337690881

Author:

Jay Rich, Jeff Jones

Publisher:

Cengage Learning

Managerial Accounting

Accounting

ISBN:

9781337912020

Author:

Carl Warren, Ph.d. Cma William B. Tayler

Publisher:

South-Western College Pub

Intermediate Financial Management (MindTap Course…

Finance

ISBN:

9781337395083

Author:

Eugene F. Brigham, Phillip R. Daves

Publisher:

Cengage Learning