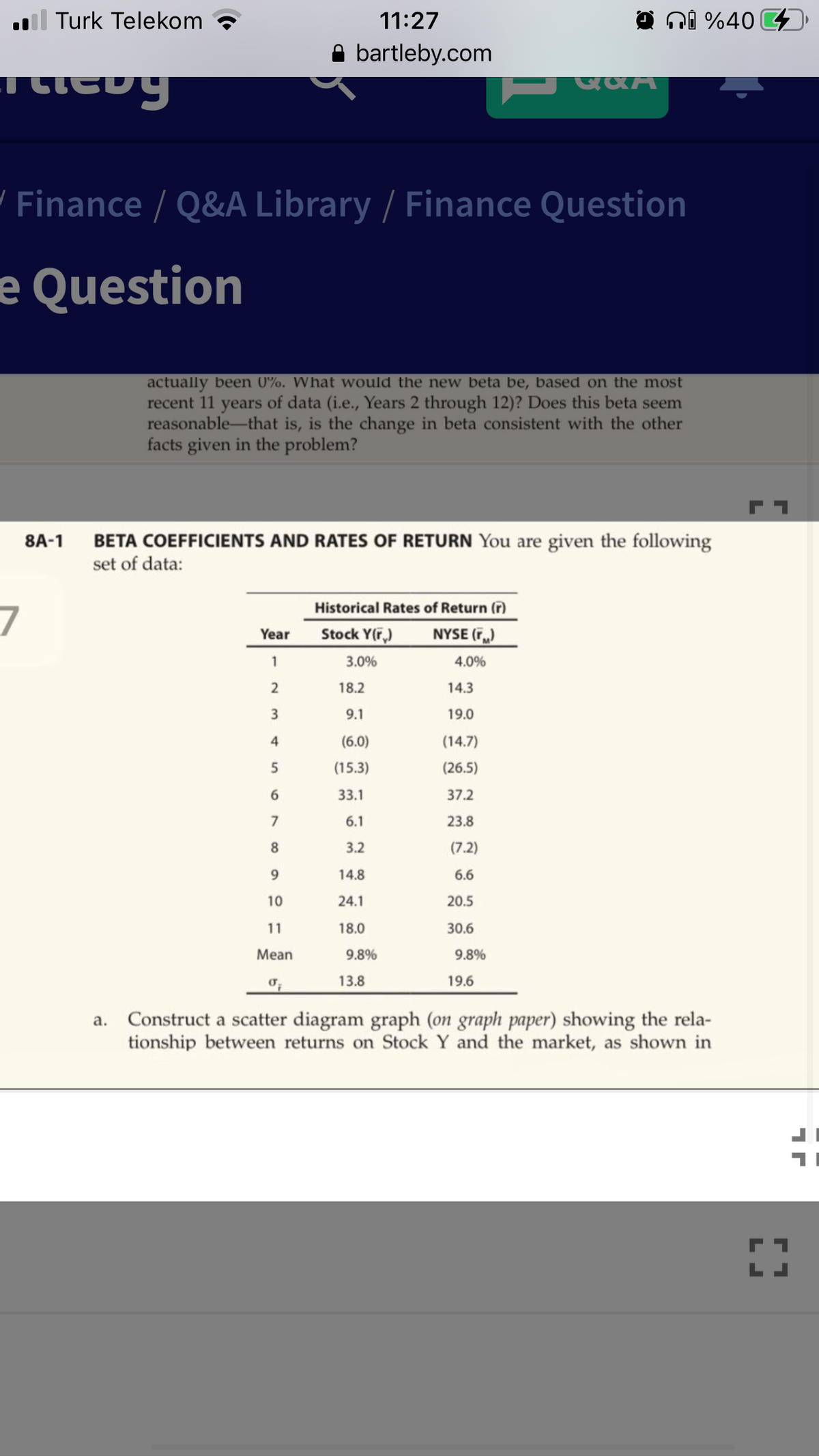

A-1 BETA COEFFICIENTS AND RATES OF RETURN You are given the following set of data: Historical Rates of Return (r) Year Stock Y(F,) NYSE (F.) 1 3.0% 4.0% 18.2 14.3 9.1 19.0 (6.0) (14.7) (15.3) (26.5) 6. 33.1 37.2 6.1 23.8 8. 3.2 (7.2) 9. 14.8 6.6 10 24.1 20.5 11 18.0 30.6 Mean 9.8% 9.8% 13.8 19.6 a. Construct a scatter diagram graph (on graph paper) showing the rela- tionship between returns on Stock Y and the market, as shown in

A-1 BETA COEFFICIENTS AND RATES OF RETURN You are given the following set of data: Historical Rates of Return (r) Year Stock Y(F,) NYSE (F.) 1 3.0% 4.0% 18.2 14.3 9.1 19.0 (6.0) (14.7) (15.3) (26.5) 6. 33.1 37.2 6.1 23.8 8. 3.2 (7.2) 9. 14.8 6.6 10 24.1 20.5 11 18.0 30.6 Mean 9.8% 9.8% 13.8 19.6 a. Construct a scatter diagram graph (on graph paper) showing the rela- tionship between returns on Stock Y and the market, as shown in

Financial Management: Theory & Practice

16th Edition

ISBN:9781337909730

Author:Brigham

Publisher:Brigham

Chapter2: Financial Statements, Cash Flow,and Taxes

Section: Chapter Questions

Problem 21SP: Begin with the partial model in the file Ch02 P21 Build a Model.xlsx on the textbooks Web site. a....

Related questions

Question

Transcribed Image Text:l Turk Telekom

11:27

ni %40

bartleby.com

שיגסרב

/ Finance / Q&A Library / Finance Question

e Question

actually been 0%. What would the new beta be, based on the most

recent 11 years of data (i.e., Years 2 through 12)? Does this beta seem

reasonable-that is, is the change in beta consistent with the other

facts given in the problem?

BETA COEFFICIENTS AND RATES OF RETURN You are given the following

set of data:

8A-1

7

Historical Rates of Return (r)

Stock Y(F,)

NYSE (r.)

Year

1

3.0%

4.0%

18.2

14.3

3

9.1

19.0

4

(6.0)

(14.7)

(15.3)

(26.5)

33.1

37.2

7

6.1

23.8

8.

3.2

(7.2)

14.8

6.6

10

24.1

20.5

11

18.0

30.6

Mean

9.8%

9.8%

13.8

19.6

a. Construct a scatter diagram graph (on graph paper) showing the rela-

tionship between returns on Stock Y and the market, as shown in

Transcribed Image Text:l Turk Telekom

11:27

ni %40 4

A bartleby.com

ance / Q&A Library / Finance Question

uestion

Figure 8A.1; then draw a freehand approximation of the regression

line. What is the approximate value of the beta coefficient? (If you have

a calculator with statistical functions, use it to calculate beta.)

b. Give a verbal interpretation of what the regression line and the beta

coefficient show about Stock Y's volatility and relative riskiness as

compared with other stocks.

c. Suppose the scatter of points had been more spread out, but the

regression line was exactly where your present graph shows it. How

would this affect (1) the firm's risk if the stock were held in a one-

asset portfolio and (2) the actual risk premium on the stock if the

CAPM held exactly? How would the degree of scatter (or the correla-

tion coefficient) affect your confidence that the calculated beta will

hold true in the years ahead?

d. Suppose the regression line had been downward sloping and the beta

coefficient had been negative. What would this imply about (1) Stock

Y's relative riskiness and (2) its probable risk premium?

Construct an illustrative probability distribution graph of returns (see

Figure 8.3) for portfolios consisting of (1) only Stock Y, (2) 1% each

of 100 stocks with beta coefficients similar to that of Stock Y, and (3)

all stocks (i.e., the distribution of returns on the market). Use as the

expected rate of return the arithmetic mean as given previously for

both Stock Y and the market, and assume that the distributions are

normal. Are the expected returns "reasonable"; that is, is it reasonable

that f, = fM = 9.8%?

е.

f. Now, suppose that in the next year, Year 12, the market return was

27%, but Firm Y increased its use of debt, which raised its perceived

risk to investors. Do you think that the return on Stock Y in Year 12

could be approximated by this historical characteristic line?

î, = 3.8% + 0.62(r,) = 3.8% + 0.62(27%) = 20.5%

g. Now, suppose r, in Year 12, after the debt ratio was increased, had

actually been 0%. What would the new beta be, based on the most

recent 11 years of data (i.e., Years 2 through 12)? Does this beta seem

reasonable-that is, is the change in beta consistent with the other

facts given in the problem?

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution!

Trending now

This is a popular solution!

Step by step

Solved in 4 steps with 2 images

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, finance and related others by exploring similar questions and additional content below.Recommended textbooks for you