(a) Jessica Ltd sold inventory during the current period to its wholly owned subsidiary, Amelie Ltd, for $15 000. These items previously cost Jessica Ltd $12 000. Amelie Ltd subsequently sold half the items to Ningbo Ltd for $8000. The tax rate is 30%. The group accountant for Jessica Ltd, Li Chen, maintains that the appropriate consolidation adjustment entries are as follows: Sales Dr. 15000 Cost of Sales Cr.13000 Inventory Cr. 2000 Deferred Tax asset Dr.300 Income Tax Expenses Cr.300 Required (i) Discuss whether the entries suggested by Li Chen are correct, explaining on a line-by-line basis the correct adjustment entry. (ii) Determine the consolidation worksheet entries in the following year, assuming the inventory has been –sold, and explain the adjustments on a line-by-line basis

- (a) Jessica Ltd sold inventory during the current period to its wholly owned subsidiary, Amelie Ltd, for $15 000. These items previously cost Jessica Ltd $12 000. Amelie Ltd subsequently sold half the items to Ningbo Ltd for $8000. The tax rate is 30%. The group accountant for Jessica Ltd, Li Chen, maintains that the appropriate consolidation

adjustment entries are as follows:

Sales Dr. 15000

Cost of Sales Cr.13000

Inventory Cr. 2000

Income Tax Expenses Cr.300

Required

- (i) Discuss whether the entries suggested by Li Chen are correct, explaining on a line-by-line basis the correct adjustment entry.

- (ii) Determine the consolidation worksheet entries in the following year, assuming the inventory has been –sold, and explain the adjustments on a line-by-line basis

Consolidated financial statement refers to the financial statements of an economic entity or a group consisting of parent and its subsidiaries. Adjustments are made for intragroup transactions for various external parties. These adjustments are in consistence with the consolidation rules. Net assets and liabilities of the parent as well as the subsidiary company needs to be adjusted in full.

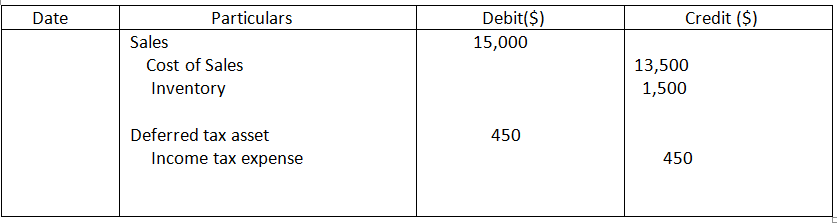

(i) The correct entry will be:

Sales :

Recorded Sales = $ ( 15,000 + 8,000)

= $ 23,000

Group Sales = $ 8,000 (External Entity sales only)

Adjustments = $ 15,000

Cost of Sales:

Recorded = $ 12,000 + 1/2 of $ 15,000

= $ 19,500

Group = 1/2 of $ 15,000

= $ 7,500

Adjustments = $ 12,000

Inventory:

Recorded = 1/2 of $ 15,000

= $ 7,500

Group = 1/2 of $ 12,000

= $ 6,000

Adjustments = $ 1,500

Step by step

Solved in 3 steps with 2 images