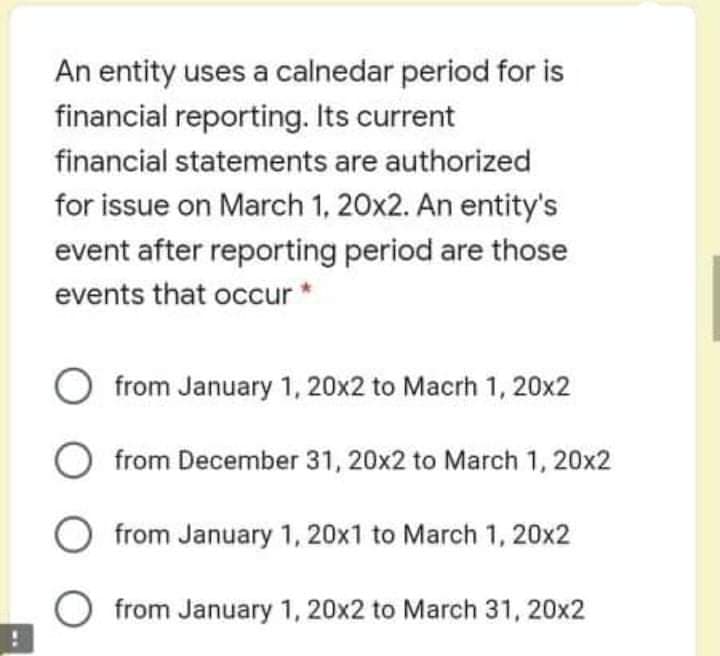

An entity uses a calnedar period for is financial reporting. Its current financial statements are authorized for issue on March 1, 20x2. An entity's event after reporting period are those events that occur

An entity uses a calnedar period for is financial reporting. Its current financial statements are authorized for issue on March 1, 20x2. An entity's event after reporting period are those events that occur

Auditing: A Risk Based-Approach to Conducting a Quality Audit

10th Edition

ISBN:9781305080577

Author:Karla M Johnstone, Audrey A. Gramling, Larry E. Rittenberg

Publisher:Karla M Johnstone, Audrey A. Gramling, Larry E. Rittenberg

Chapter17: Other Services Provided By Audit Firms

Section: Chapter Questions

Problem 45RSCQ

Related questions

Question

Transcribed Image Text:An entity uses a calnedar period for is

financial reporting. Its current

financial statements are authorized

for issue on March 1, 20x2. An entity's

event after reporting period are those

events that occur*

from January 1, 20x2 to Macrh 1, 20x2

O from December 31, 20x2 to March 1, 20x2

from January 1, 20x1 to March 1, 20x2

from January 1, 20x2 to March 31, 20x2

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

Step by step

Solved in 2 steps

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, accounting and related others by exploring similar questions and additional content below.Recommended textbooks for you

Auditing: A Risk Based-Approach to Conducting a Q…

Accounting

ISBN:

9781305080577

Author:

Karla M Johnstone, Audrey A. Gramling, Larry E. Rittenberg

Publisher:

South-Western College Pub

Cornerstones of Financial Accounting

Accounting

ISBN:

9781337690881

Author:

Jay Rich, Jeff Jones

Publisher:

Cengage Learning

Individual Income Taxes

Accounting

ISBN:

9780357109731

Author:

Hoffman

Publisher:

CENGAGE LEARNING - CONSIGNMENT

Auditing: A Risk Based-Approach to Conducting a Q…

Accounting

ISBN:

9781305080577

Author:

Karla M Johnstone, Audrey A. Gramling, Larry E. Rittenberg

Publisher:

South-Western College Pub

Cornerstones of Financial Accounting

Accounting

ISBN:

9781337690881

Author:

Jay Rich, Jeff Jones

Publisher:

Cengage Learning

Individual Income Taxes

Accounting

ISBN:

9780357109731

Author:

Hoffman

Publisher:

CENGAGE LEARNING - CONSIGNMENT