An investor is given the following quotes from a bank: S$ / USS S$ /€ Bid 0.7410 Offer 0.7430 (i.e. S$1 = 74 US cents approximately) 0.5050 (i.e. S$1 = 0.5 euro approximately) 0.5030 Suppose the investor has 1,000 Euros and wants to change them into US dollar Analyse how the investor could determine the amount of US dollars the bank wi give him, Answer to three (3) decimal places.

An investor is given the following quotes from a bank: S$ / USS S$ /€ Bid 0.7410 Offer 0.7430 (i.e. S$1 = 74 US cents approximately) 0.5050 (i.e. S$1 = 0.5 euro approximately) 0.5030 Suppose the investor has 1,000 Euros and wants to change them into US dollar Analyse how the investor could determine the amount of US dollars the bank wi give him, Answer to three (3) decimal places.

Chapter7: International Arbitrage And Interest Rate Parity

Section: Chapter Questions

Problem 33QA

Related questions

Question

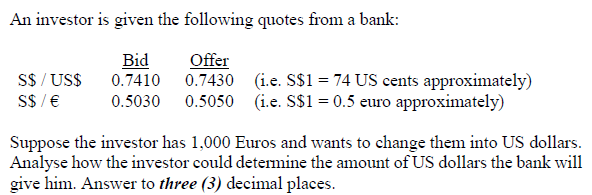

Transcribed Image Text:An investor is given the following quotes from a bank:

Bid

S$ / US$

S$ / €

Offer

0.7430 (i.e. S$1 = 74 US cents approximately)

0.7410

0.5030 0.5050 (i.e. S$1 = 0.5 euro approximately)

Suppose the investor has 1,000 Euros and wants to change them into US dollars.

Analyse how the investor could determine the amount of US dollars the bank will

give him. Answer to three (3) decimal places.

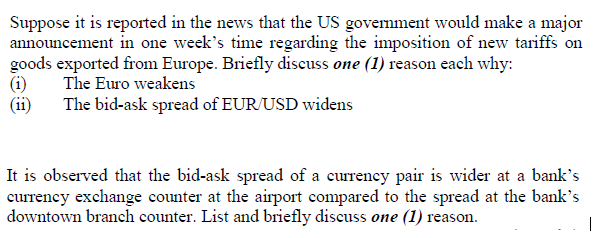

Transcribed Image Text:Suppose it is reported in the news that the US govemment would make a major

announcement in one week's time regarding the imposition of new tariffs on

goods exported from Europe. Briefly discuss one (1) reason each why:

(i)

(ii)

The Euro weakens

The bid-ask spread of EUR/USD widens

It is observed that the bid-ask spread of a currency pair is wider at a bank's

currency exchange counter at the airport compared to the spread at the bank's

downtown branch counter. List and briefly discuss one (1) reason.

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

Step by step

Solved in 3 steps with 2 images

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, finance and related others by exploring similar questions and additional content below.Recommended textbooks for you

Intermediate Financial Management (MindTap Course…

Finance

ISBN:

9781337395083

Author:

Eugene F. Brigham, Phillip R. Daves

Publisher:

Cengage Learning

EBK CONTEMPORARY FINANCIAL MANAGEMENT

Finance

ISBN:

9781337514835

Author:

MOYER

Publisher:

CENGAGE LEARNING - CONSIGNMENT

Intermediate Financial Management (MindTap Course…

Finance

ISBN:

9781337395083

Author:

Eugene F. Brigham, Phillip R. Daves

Publisher:

Cengage Learning

EBK CONTEMPORARY FINANCIAL MANAGEMENT

Finance

ISBN:

9781337514835

Author:

MOYER

Publisher:

CENGAGE LEARNING - CONSIGNMENT