And and Average Returns for Stocks, Bonds, and T-Bills, 1950 to 2017 Long-Term Treasury 1950 to 2017 1950 to 1959 1960 to 1969 1970 to 1979 1980 to 1989 1990 to 1999 2000 to 2009 Average Average Average Average Average Average Average Annual Return 2010 2011 Annual Return 2012 Annual Return 2013 Annual Return 2014 Annual Return 2015 Annual Return 2016 Annual Return 2017 Annual Return Average 2010 to 2017 Stocks 12.7% 20.9 8.7 7.5 18.2 19.0 0.9 15.1 2.1 16.0 32.4 13.7 1.4 12.0 21.8 14.3 Bonds 6.6% 0.0 1.6 5.7 13.5 9.5 8.0 9.4 29.9 3.6 -12.7 25.1 -1.2 1.2 8.4 8.0 T-bills 4.30% 2.00 4.00 6.30 8.90 4.90 2.70 0.01 0.02 0.02 0.07 0.05 0.21 0.51 1.39 0.29 You have a portfolio with an asset allocation of 60 percent stocks, 30 percent long-term Treasury bonds, and 10 percent T-bills. Use these weights and the returns given in the above table to compute the return of the portfolio in the year 2010 and each year since. Then compute the average annual return and standard deviation of the portfolio. (Do not round intermediate calculations. Round your answers to 2 decimal places.)

And and Average Returns for Stocks, Bonds, and T-Bills, 1950 to 2017 Long-Term Treasury 1950 to 2017 1950 to 1959 1960 to 1969 1970 to 1979 1980 to 1989 1990 to 1999 2000 to 2009 Average Average Average Average Average Average Average Annual Return 2010 2011 Annual Return 2012 Annual Return 2013 Annual Return 2014 Annual Return 2015 Annual Return 2016 Annual Return 2017 Annual Return Average 2010 to 2017 Stocks 12.7% 20.9 8.7 7.5 18.2 19.0 0.9 15.1 2.1 16.0 32.4 13.7 1.4 12.0 21.8 14.3 Bonds 6.6% 0.0 1.6 5.7 13.5 9.5 8.0 9.4 29.9 3.6 -12.7 25.1 -1.2 1.2 8.4 8.0 T-bills 4.30% 2.00 4.00 6.30 8.90 4.90 2.70 0.01 0.02 0.02 0.07 0.05 0.21 0.51 1.39 0.29 You have a portfolio with an asset allocation of 60 percent stocks, 30 percent long-term Treasury bonds, and 10 percent T-bills. Use these weights and the returns given in the above table to compute the return of the portfolio in the year 2010 and each year since. Then compute the average annual return and standard deviation of the portfolio. (Do not round intermediate calculations. Round your answers to 2 decimal places.)

Fundamentals of Financial Management, Concise Edition (with Thomson ONE - Business School Edition, 1 term (6 months) Printed Access Card) (MindTap Course List)

8th Edition

ISBN:9781285065137

Author:Eugene F. Brigham, Joel F. Houston

Publisher:Eugene F. Brigham, Joel F. Houston

Chapter8: Risk And Rates Of Return

Section: Chapter Questions

Problem 22SP

Related questions

Question

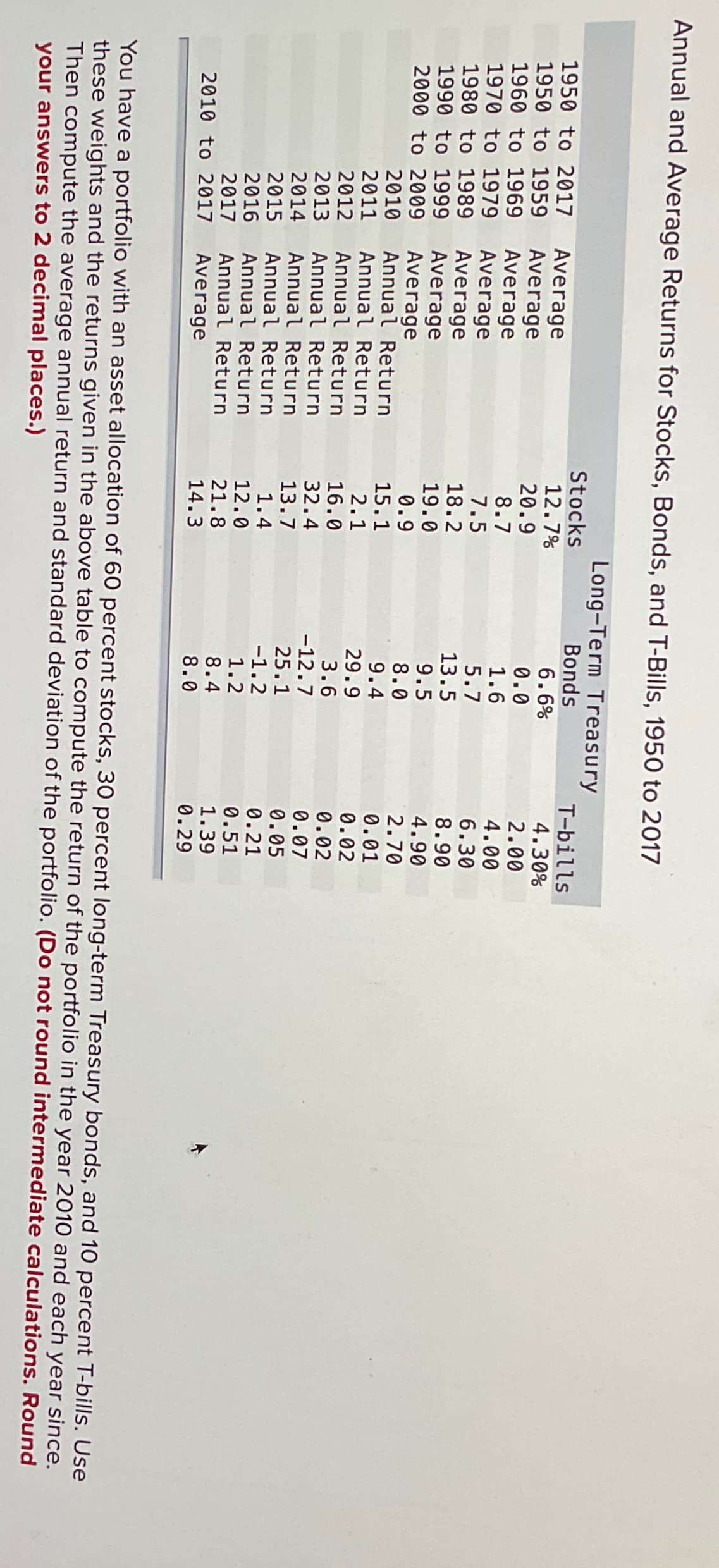

Transcribed Image Text:Annual and Average Returns for Stocks, Bonds, and T-Bills, 1950 to 2017

Long-Term Treasury

1950 to 2017 Average

1950 to 1959

Average

1960 to 1969

Average

1970 to 1979

Average

1980 to 1989

Average

1990 to 1999

Average

2000 to 2009

Average

2010

Annual Return

2011 Annual Return

2012 Annual Return

2013 Annual Return

2014 Annual Return

2015 Annual Return

2016 Annual Return

2017

Annual Return

Average

2010 to 2017

Stocks

12.7%

20.9

8.7

7.5

18.2

19.0

0.9

15.1

2.1

16.0

32.4

13.7

1.4

12.0

21.8

14.3

Bonds

6.6%

0.0

1.6

5.7

13.5

9.5

8.0

9.4

29.9

3.6

-12.7

25.1

-1.2

1.2

8.4

8.0

T-bills

4.30%

2.00

4.00

6.30

8.90

4.90

2.70

0.01

0.02

0.02

0.07

0.05

0.21

0.51

1.39

0.29

You have a portfolio with an asset allocation of 60 percent stocks, 30 percent long-term Treasury bonds, and 10 percent T-bills. Use

these weights and the returns given in the above table to compute the return of the portfolio in the year 2010 and each year since.

Then compute the average annual return and standard deviation of the portfolio. (Do not round intermediate calculations. Round

your answers to 2 decimal places.)

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution!

Trending now

This is a popular solution!

Step by step

Solved in 3 steps with 2 images

Recommended textbooks for you

Fundamentals of Financial Management, Concise Edi…

Finance

ISBN:

9781285065137

Author:

Eugene F. Brigham, Joel F. Houston

Publisher:

Cengage Learning

Fundamentals of Financial Management, Concise Edi…

Finance

ISBN:

9781305635937

Author:

Eugene F. Brigham, Joel F. Houston

Publisher:

Cengage Learning

Fundamentals of Financial Management (MindTap Cou…

Finance

ISBN:

9781285867977

Author:

Eugene F. Brigham, Joel F. Houston

Publisher:

Cengage Learning

Fundamentals of Financial Management, Concise Edi…

Finance

ISBN:

9781285065137

Author:

Eugene F. Brigham, Joel F. Houston

Publisher:

Cengage Learning

Fundamentals of Financial Management, Concise Edi…

Finance

ISBN:

9781305635937

Author:

Eugene F. Brigham, Joel F. Houston

Publisher:

Cengage Learning

Fundamentals of Financial Management (MindTap Cou…

Finance

ISBN:

9781285867977

Author:

Eugene F. Brigham, Joel F. Houston

Publisher:

Cengage Learning

Fundamentals Of Financial Management, Concise Edi…

Finance

ISBN:

9781337902571

Author:

Eugene F. Brigham, Joel F. Houston

Publisher:

Cengage Learning