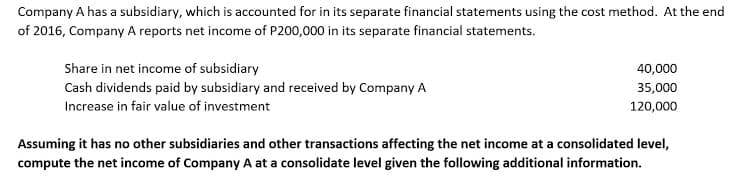

Assuming it has no other subsidiaries and other transactions affecting the net income at a consolidated level, compute the net income of Company A at a consolidate level given the following additional information.

Q: It is the bringing together of separate entities or businesses into one reporting entity. * O Merger…

A: Merger means 2 company's will together form into one company new Acquisition means one company will…

Q: Which of the following is not typical of the journal entries prepared by a parent company to account…

A: Parent company is the one which owns more than 50% stocks of another entity. A parent company…

Q: Explain the impact that a net operating loss of an acquired affiliate has on consolidated figures.

A: Consolidated financial statements: These financial statements are consolidated financial statements…

Q: Answer these questions about consolidation accounting:1. Define parent company. Define subsidiary…

A: Consolidated financial statements: When an investor company holds above 50% in the outstanding stock…

Q: Revenue is recognized when it is earned; therefore revenue earned for a consolidated entity occurs…

A: When one company or its subsidiary company , hold more than 50% share in another company , then…

Q: The single set of financial statements that combines financial information from the separate…

A: Option (a) is incorrect because equity financial statements or Statement of changes in Equity are…

Q: In many cases, EPS is computed based on the parent’s portion of consolidated net income and parent…

A: Answer:

Q: Only the income statement is consolidated on the date of a business combination of a parent company…

A: Consolidated Balance Sheet:-It is a Balance Sheet that consists of assets, liabilities, and…

Q: Consolidated net income for a parent company and its partially owned subsidiary is best defined as…

A: The entity which holds stock of more than 50% in other one is known as a parent or holding entity.…

Q: Explain why transactions between members of a consolidated firm should not be reflected in the…

A: Introduction: Consolidated financial statements are the consolidated audited financials of a company…

Q: In determining controlling interest in consolidated income in the consolidated financial statements,…

A: Controlling interest is defined as the ownership interest in the business with adequate voting stock…

Q: In situations where there are routine inventory sales between parent companies and subsidiaries,…

A: Consolidation of parent company and subsidiary company.

Q: Assuming it has no other subsidiaries and other transactions affecting the net income at a…

A: Given Information: Net Income of Company A = P200,000 Share in net income of Subsidiary = P40,000…

Q: cess of preparing Consolidated Financial Statements involves the elimination of intercompany…

A: In subsidiary account and parent company account there are common transaction which are to be dealt…

Q: The purpose of consolidated accounts are as follows except: Show obligations of the group Show…

A: The purpose of consolidated accounts are as follows except to Show obligations of the subsidiary.

Q: preparation of consolidated financial statements

A: Second option is wrong because the preparation of consolidated financial statements does not…

Q: How is the portion of consolidated earnings to be assigned to the non-controlling interest in…

A:

Q: In the separate financial statement of the parent company, which of the following statements…

A: The correct answer for the above mentioned question is given in the following steps for your…

Q: Consolidated financial statements: a. Consolidated financial statements provide information about…

A: Consolidated financial statements: When an investor company holds above 50% in the outstanding stock…

Q: A. the results of the subsidiary for the period of time that it was controlled to be accounts.…

A: AASB stands for Australian accounting standards board and belongs to the Australian government…

Q: In consolidated financial statements: Multiple Choice the parent's and subsidiary's financial…

A: Please see the next step for the solution

Q: According to PFRS 10 A. A parent entity is required to consolidate its subsidiaries only for…

A: Accounting standards are the rules and regulations provided to business in order to maintain and…

Q: Which of the following is not typical of the journal entries prepared by a parent company to account…

A: Consolidated financial statements are the financial statements of a group consisting of multiple…

Q: what is the balance in the new corporation’s Retained earnings account?

A: Under IFRS -3 a business combination transaction is said to be closed when the net assets of the…

Q: Which of the following income items may affect both Consolidated Net Income attributable to Parent…

A: Consolidation Consolidation means the parent company taken over the shares of subsidiary company…

Q: A) When preparing consolidated financial statement workpapers, unrealized intercompany gains, as a…

A: The accounting of the inter-company is the one which includes the transactions of the company and…

Q: Which of the following statements about pushdown accounting is correct? Select one: a. Pushdown…

A: When a firm buys another company, accountants must document every aspect of the transaction,…

Q: Which of the following is incorrect regarding consolidated financial statements?

A: Consolidation is the acquisition of a smaller company by a large company. When a company acquires…

Q: Assuming the existence of two companies, A and B, which of the following is not a business…

A: As per IFRS/PFRS 3 Business combination A business combination is said to be exist only when their…

Q: Discuss how the consolidated financial statements reflect: (a) The “single economic entity” concept.

A: Whenever one company has control over another company by investing in its share capital, then one…

Q: What is push-down accounting?a. A requirement that a subsidiary must use the same accounting…

A: Push-down accounting: Its a book keeping method used by companies when they buy out another firm. In…

Q: Choose the correct. Which of the following is the best theoretical justification for consolidated…

A: Consolidated financial statements: When an investor company holds above 50% in the outstanding…

Q: Statement 1: The preparation of consolidated financial statements after acquisition is materially…

A: Consolidated financial statements(CFS): The statements in which all the items of balance sheet i.e.,…

Q: Which of the following statements is not correct in relation to consolidation accounting key terms?…

A: Parent and subsidiary are two types of companies. Parent company is that company who has control…

Q: How is the amount assigned to the non-controlling interest normally determined when a consolidated…

A:

Q: Which of the following regarding the preparation of Consolidated Financial Statement is correct? A.…

A: As per IFRS 10 consolidated financial statements are to be prepared to enable users to get overall…

Q: Which of the following is incorrect regarding consolidated financial statements? a. Consolidation…

A: Consolidation is the acquisition of a smaller company by a large company. When a company acquires…

Q: Consolidated financial statements are the financial statements of a group in which the assets,…

A: As per IAS 27, Consolidated Financial Statements are the financial statements of a group in which…

Q: Assuming the existence of two companies, A and B, which of the following is not a business…

A: Company C is formed to acquire all the assets and liabilities of Company A and Company B. Both…

Q: Which statement is incorrect concerning the preparation of consolidated financial statements? A.…

A: Solution Concept The financial statements of the parent and its subsidiaries shall be consolidated…

Q: entity that is represented by a single set of consolidated financial statements

A: Option a is wrong because economic entity is a distinct entity that does not require consolidated…

Q: When we are preparing consolidated financial statements, will the financial statements of the parent…

A: Consolidation is a term used for merging of several companies of an industry. The assets,…

Q: All the financial statements is consolidated on the date of a business combination of a parent…

A: Parent company and subsidiary company are two companies, in which one company acquires shareholding…

Q: Only the balance sheet is consolidated on the date of a business combination of a parent company and…

A: Consolidated financial statements provide an aggregate financial report of separate legal entities.…

Q: According to PFRS (IFRS) 10: a. A parent entity is required to c

A: The Standard: [IFRS 10:1] a parent entity (an entity that controls one or more other entities) is…

Q: Consolidation financial statements are prepared when a parent-subsidiary relationship exists in…

A: Financial statements show the financial performance/position of the business entity. It is prepared…

Step by step

Solved in 2 steps

- Archie Co. has a subsidiary, which is accounted for in its separate financial statements using the cost method. At the end of 2016, the company reports net income of $20,000 in its separate financial statements. Increase in fair value of investment $12,000 Share in net income of subsidiary $4,000 Cash dividends paid by subsidiary and received by the company $3,500 Assuming it has no other subsidiaries and other transactions affecting the net income at a consolidated level, compute the net income of the company at a consolidate level.Artichoke Co. has a subsidiary, which is accounted for in its separate financial statements using the cost method. At the end of 2032, the company reports net income of $200,000 in its separate financial statements. Cash dividends paid by subsidiary and received by the company $35,000 Increase in fair value of investment $120,000 Share in net income of subsidiary $40,000 Assuming it has no other subsidiaries and other transactions affecting the net income at a consolidated level, compute the net income of the company at a consolidate level.Company A has a subsidiary, which is accounted for in its separate financial statements using the cost method. At the end of 2016, Company A reports net income of P200,000 in its separate financial statements. 8. Assuming it has no other subsidiaries and other transactions affecting the net income at a consolidated level, compute the net income of Company A at a consolidate level given the following additional information:

- The consolidated income statement of P Corp. and its 80% subsidiary follows: P. Corp and Subsidiary Consolidated Income Statement For the year ended December 31, 2013 Sales P402,000 Cost of Goods Sold 246,000 Gross Profit 156,000 Operating expenses 81,000 Consolidated net income 75,000 Non-controlling interest in net income 6,000 Share of P. Corp. in the consolidated net income P69,000 How much of the consolidated net income was the result of the operation of the subsidiary? A. P51,000 B. P24,000 C. P7,500 D. P30,000Selected information from the separate and consolidated income statements of CHAELISA LTD.and as subsidiary, JENSOO INC. for the year ended December 31, 2021 are as follows: CHAELISA LTD. JENSOOINC. ConsolidatedSales P600,000 P420,000 P924,000COGS 450,000 330,000 693,000Gross profit P150,000 P 90,000 P231,000 During 2021, CHAELISA LTD. sold goods to JENSOO INC. at the same mark-up on cost that CHAELISA LTD. uses for all sales. At December 31, 2021, JENSOO INC. had not paid all of these goods and still held 37.5% of them in inventory. Compute for the original cost of goods in JENSOO INC.’s inventory acquired from Apple.White Bright Limited has three subsidiary Companies as on 31st March, 2018. Based upon the information given in the following, ascertain how the Cost of Investment will be treated in the Consolidated Balance Sheet. Particulars Amount in Millions Hazy Limited Clear Limited Sun Limited Investment made 205.00 117.00 145.00 Percent of Shares Owned 60% 65% 75% Assets at the time of Investment 625.40 314.84 443.75 Liabilities at the time of Investment 260.44 134.84 329.55 don't give hand written answers plz

- On January 1, 20x6, Parent Corporation purchased 80% of Subsidiary Company's outstanding stock for P620,000. At that date, all of Subsidiary's assets and liabilities had market valu. approximately equal to their book valu. and no goodwill was includ. in the purchase price. The following information was available for 20x6: income from own operations of Parent, P150,000, operating loss of Subsidiary, P20,000. Dividends paid in 20x6 by Parent, P75,000; by Subsidiary to Parent, P12,000.1 On July 1, 20x6, there was a downstream sale of equipment at a gain of P25,000. The equipment is expected to have a remaining useful life of 10 years from the date of sale. Also, on January 1, 20x6, there was an upstream sale of furniture at a loss of P7,500. The furniture is expected to have a useful life of five years from the date of sale. Non-controlling interest is measured at fair value. How much is the consolidated net income attributable to the parent shareholders' equity?Presidio’s appraisal of Mason's fair values deemed three accounts to be undervalued: Inventory by $8,350, Land by $16,000, and Buildings by $30,200. Presidio plans to maintain Mason’s separate legal identity and to operate Mason as a wholly owned subsidiary. Required: Prepare Presidio's journal entries to record its acquisition of Mason, related professional fees paid, and stock acquisition costs. Separately determine each individual amount that Presidio Company would report in its consolidated balance sheet following the acquisition of Mason. Include in Presidio's retained earnings any adjustments to income accounts from part (a). To verify the answers found in part (b), adjust Presidio's column of accounts for the journal entries in part (a) and then prepare a worksheet to consolidate the balance sheets of these two companies at the acquisition date.A Parent corporation purchased 25% of the outstanding common shares of Subsidiary Limited for $2,500,000 on January 1, 2020. The following relates to Subsidiary since the acquisition date: Year Net Income Other Comprehensive Income Dividends Paid 2020 $ 51,800 $11,400 $74,000 2021 148,000 29,600 74,000 Required: Assume that Parent is a private company. Even though it has significant influence, it chose to use the cost method to account for its investment. Prepare ALL the journal entries that Parent should make regarding this investment in Year 2020 and Year 2021

- Computing the noncontrolling interests equity balance Assume the following facts relating to an 90% owned subsidiary company: BOY stockholders’ equity $1,300,000 BOY AAP assets 169,000 Net income of subsidiary (not including [A] asset depreciation and amortization) 312,000 AAP assets depreciation and amortization expense 52,000 Dividends declared and paid by subsidiary 26,000 a. Compute the net income attributable to noncontrolling interests for the year. b. Compute the amount reported as noncontrolling equity at the end of the year.Parent and its 80% owned Subsidiary report the following at December 31 of the current year: Parent Net Income, P100,000; Parent Dividends, P20,000, Parent Land, P500,000. Subsidiary Net Income, P80,000; Subsidiary Dividends, P10,000; Subsidiary Land, P300,000. On June 1, of the current year, Subsidiary sold land to Parent reporting a gain on sale of P10,000. The gain is included in the net income reported by the Subsidiary. 1. Determine the equity holders of parent’s net income and the non-controlling interest net income. 2. Determine the non-controlling interest net income.Assuming there have been no intercompany transactions, which of the following is an incorrect statement concerning the financial statement or statements of a parent and its 60% owned subsidiary? *a. Consolidated financial statements would include 100% of the assets and liabilities of the subsidiary.b. Answer not givenc. If the parent does not prepare consolidated financial statements, it must use the equity method of accounting.d. Net income of the parent would be the same whether or not consolidated statements were prepared.e. The non-controlling interest in net assets would not be shown on the consolidated balance sheet.