Attribution analysis uses the Portfolio Manager's and Benchmark's asset allocations and returns across asset classes. A potential investor wishes to understand the skills of a Portfolio Manager based on the data below: Asset Class Port. Weight BM Weight Port. Return BM Return Equity 20% 60% 6% 8% Bonds 80% 40% 6% 4% Which of the following statement is incorrect O The portfolio manager is worse at market timing than the ability to identify mispriced securities. O The portfolio underperformed the benchmark by 0.40% O The selection effect returns is negative O The Allocation Effect return is -1.60% O The sum of selection effect returns and allocation effect returns equal -0.40%

Attribution analysis uses the Portfolio Manager's and Benchmark's asset allocations and returns across asset classes. A potential investor wishes to understand the skills of a Portfolio Manager based on the data below: Asset Class Port. Weight BM Weight Port. Return BM Return Equity 20% 60% 6% 8% Bonds 80% 40% 6% 4% Which of the following statement is incorrect O The portfolio manager is worse at market timing than the ability to identify mispriced securities. O The portfolio underperformed the benchmark by 0.40% O The selection effect returns is negative O The Allocation Effect return is -1.60% O The sum of selection effect returns and allocation effect returns equal -0.40%

Financial Management: Theory & Practice

16th Edition

ISBN:9781337909730

Author:Brigham

Publisher:Brigham

Chapter25: Portfolio Theory And Asset Pricing Models

Section: Chapter Questions

Problem 2MC

Related questions

Question

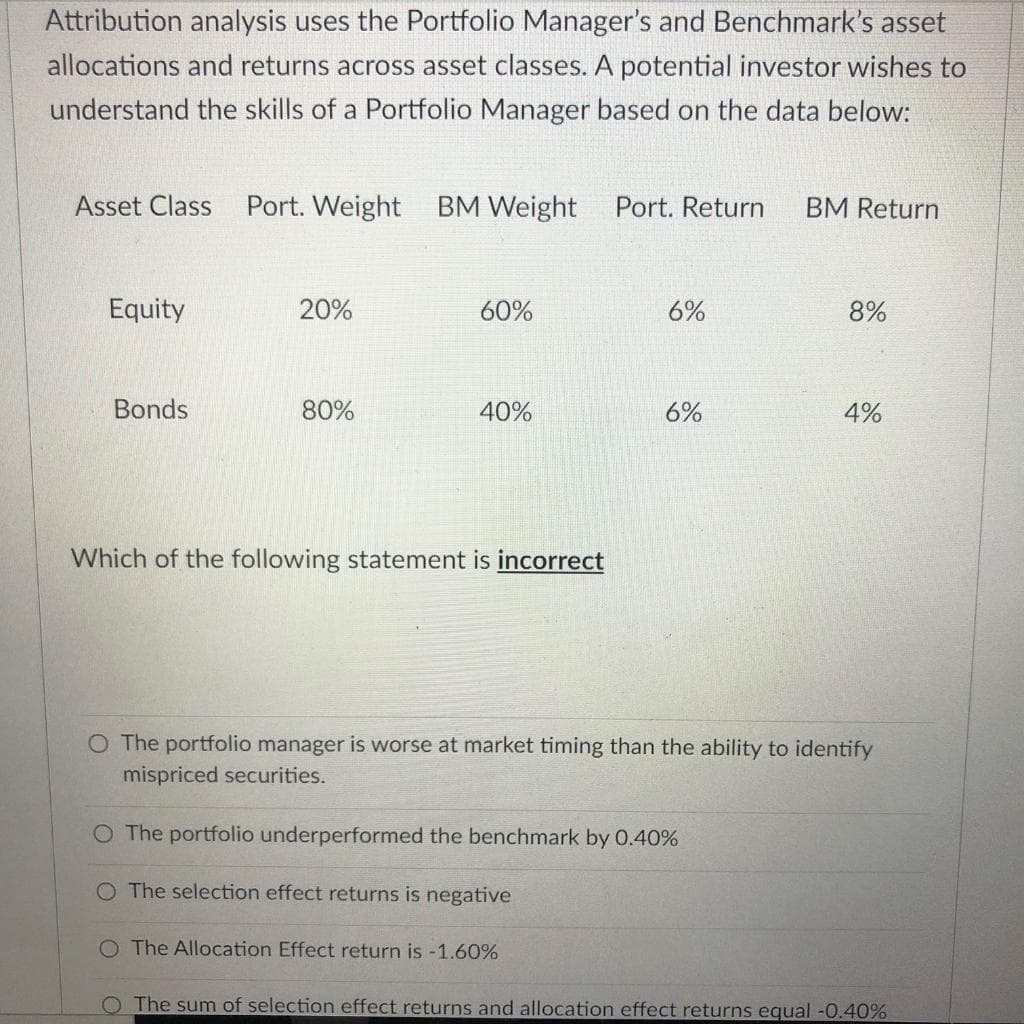

Transcribed Image Text:Attribution analysis uses the Portfolio Manager's and Benchmark's asset

allocations and returns across asset classes. A potential investor wishes to

understand the skills of a Portfolio Manager based on the data below:

Asset Class

Port. Weight

BM Weight

Port. Return

BM Return

Equity

20%

60%

6%

8%

Bonds

80%

40%

6%

4%

Which of the following statement is incorrect

O The portfolio manager is worse at market timing than the ability to identify

mispriced securities.

O The portfolio underperformed the benchmark by 0.40%

O The selection effect returns is negative

O The Allocation Effect return is -1.60%

O The sum of selection effect returns and allocation effect returns equal -0.40%

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

Step by step

Solved in 2 steps with 2 images

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, finance and related others by exploring similar questions and additional content below.Recommended textbooks for you

Intermediate Financial Management (MindTap Course…

Finance

ISBN:

9781337395083

Author:

Eugene F. Brigham, Phillip R. Daves

Publisher:

Cengage Learning

Intermediate Financial Management (MindTap Course…

Finance

ISBN:

9781337395083

Author:

Eugene F. Brigham, Phillip R. Daves

Publisher:

Cengage Learning