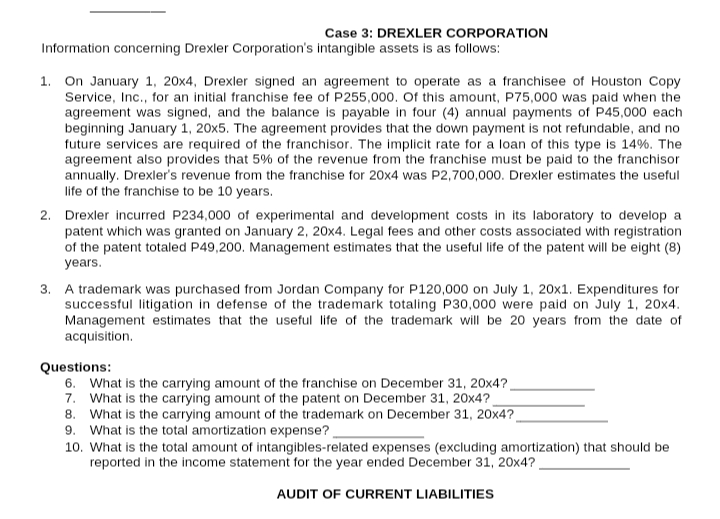

Case 3: DREXLER CORPORATION Information concerning Drexler Corporation's intangible assets is as follows: 1. On January 1, 20x4, Drexler signed an agreement to operate as a franchisee of Houston Copy Service, Inc., for an initial franchise fee of P255,00o. Of this amount, P75,000 was paid when the agreement was signed, and the balance is payable in four (4) annual payments of P45,000 each beginning January 1, 20x5. The agreement provides that the down payment is not refundable, and no future services are required of the franchisor. The implicit rate for a loan of this type is 14%. The agreement also provides that 5% of the revenue from the franchise must be paid to the franchisor annually. Drexler's revenue from the franchise for 20x4 was P2,700,000. Drexler estimates the useful life of the franchise to be 10 years. 2. Drexler incurred P234,000 of experimental and development costs in its laboratory to develop a patent which was granted on January 2, 20x4. Legal fees and other costs associated with registration of the patent totaled P49,200. Management estimates that the useful life of the patent will be eight (8) years. 3. A trademark was purchased from Jordan Company for P120,000 on July 1, 20x1. Expenditures for successful litigation in defense of the trademark totaling P30,000 were paid on July 1, 20x4.

Case 3: DREXLER CORPORATION Information concerning Drexler Corporation's intangible assets is as follows: 1. On January 1, 20x4, Drexler signed an agreement to operate as a franchisee of Houston Copy Service, Inc., for an initial franchise fee of P255,00o. Of this amount, P75,000 was paid when the agreement was signed, and the balance is payable in four (4) annual payments of P45,000 each beginning January 1, 20x5. The agreement provides that the down payment is not refundable, and no future services are required of the franchisor. The implicit rate for a loan of this type is 14%. The agreement also provides that 5% of the revenue from the franchise must be paid to the franchisor annually. Drexler's revenue from the franchise for 20x4 was P2,700,000. Drexler estimates the useful life of the franchise to be 10 years. 2. Drexler incurred P234,000 of experimental and development costs in its laboratory to develop a patent which was granted on January 2, 20x4. Legal fees and other costs associated with registration of the patent totaled P49,200. Management estimates that the useful life of the patent will be eight (8) years. 3. A trademark was purchased from Jordan Company for P120,000 on July 1, 20x1. Expenditures for successful litigation in defense of the trademark totaling P30,000 were paid on July 1, 20x4.

Financial & Managerial Accounting

13th Edition

ISBN:9781285866307

Author:Carl Warren, James M. Reeve, Jonathan Duchac

Publisher:Carl Warren, James M. Reeve, Jonathan Duchac

Chapter13MJ: Mornin' Joe

Section: Chapter Questions

Problem 2IFRS

Related questions

Question

Transcribed Image Text:Case 3: DREXLER CORPORATION

Information concerning Drexler Corporation's intangible assets is as follows:

1. On January 1, 20x4, Drexler signed an agreement to operate as a franchisee of Houston Copy

Service, Inc., for an initial franchise fee of P255,000. Of this amount, P75,000 was paid when the

agreement was signed, and the balance is payable in four (4) annual payments of P45,000 each

beginning January 1, 20x5. The agreement provides that the down payment is not refundable, and no

future services are required of the franchisor. The implicit rate for a loan of this type is 14%. The

agreement also provides that 5% of the revenue from the franchise must be paid to the franchisor

annually. Drexler's revenue from the franchise for 20x4 was P2,700,000. Drexler estimates the useful

life of the franchise to be 10 years.

2. Drexler incurred P234,000 of experimental and development costs in its laboratory to develop a

patent which was granted on January 2, 20x4. Legal fees and other costs associated with registration

of the patent totaled P49,200. Management estimates that the useful life of the patent will be eight (8)

years.

3. A trademark was purchased from Jordan Company for P120,000 on July 1, 20x1. Expenditures for

successful litigation in defense of the trademark totaling P30,000 were paid on July 1, 20x4.

Management estimates that the useful life of the trademark will be 20 years from the date of

acquisition.

Questions:

6. What is the carrying amount of the franchise on December 31, 20x4?

7. What is the carrying amount of the patent on December 31, 20x4?

8. What is the carrying amount of the trademark on December 31, 20x4?

9. What is the total amortization expense?

10. What is the total amount of intangibles-related expenses (excluding amortization) that should be

reported in the income statement for the year ended December 31, 20x4?

AUDIT OF CURRENT LIABILITIES

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution!

Trending now

This is a popular solution!

Step by step

Solved in 3 steps with 2 images

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, accounting and related others by exploring similar questions and additional content below.Recommended textbooks for you

Financial & Managerial Accounting

Accounting

ISBN:

9781285866307

Author:

Carl Warren, James M. Reeve, Jonathan Duchac

Publisher:

Cengage Learning

Financial & Managerial Accounting

Accounting

ISBN:

9781285866307

Author:

Carl Warren, James M. Reeve, Jonathan Duchac

Publisher:

Cengage Learning