Computing Impairment of Intangible Assets Stiller Company had the following information for its three intangible assets. 1. Patent: A patent was purchased for $180,000 on June 30, 2018. Stiller estimated the useful life of the patent to be 15 years. On December 31, 2020, the estimated future cash flows attributed to the patent were $153,000. The fair value of the patent was $135,000. 2. Trademark: A trademark was purchased for $9,000 on August 31, 2019. The trademark is considered to have an indefinite life. The fair value of the trademark on December 31, 2020, is $4,500. 3. Goodwill: Stiller recorded goodwill in January 2019, related to a purchase of another company. The carrying value of goodwill is $54,000 on December 31, 2020. On December 31, 2020, the segment for which the goodwill relates had a fair value of $1,044,000. The book value of the net assets of the segment (including goodwill) is $1,080,000. Note: Round each of your answers to the nearest whole dollar. a. Classify each of the intangible assets above as a finite life intangible or an indefinite life intangible. Patent Trademark Indefinite life intangible v Finite life intangible Goodwill Indefinite life intangible b. Determine the carrying value of each asset on December 31, 2020, prior to testing for impairment, assuming that the company uses the straight-line method Carrying value of patent, Dec. 31, 2020, before impairment testing Carrying value of trademark, Dec. 31, 2020, before impairment testing s Carrying value of goodwill, Dec. 31, 2020, before impairment testing amortize intangible assets, and no impairment was reported prior to 2020. 153,000 x 9,000 v 54,000 v c. Test each asset for impairment assuming that the qualitative assessment indicated that further impairment testing was warranted. Determine the carrying value of each asset on December 31, 2020, after impairment testing. Carrying value of patent, Dec. 31, 2020, after impairment testing 15,000 x Carrying value of trademark, Dec. 31, 2020, after impairment testing s 4,500 Carrying value of goodwill, Dec. 31, 2020, after impairment testing 18.000 v

Computing Impairment of Intangible Assets Stiller Company had the following information for its three intangible assets. 1. Patent: A patent was purchased for $180,000 on June 30, 2018. Stiller estimated the useful life of the patent to be 15 years. On December 31, 2020, the estimated future cash flows attributed to the patent were $153,000. The fair value of the patent was $135,000. 2. Trademark: A trademark was purchased for $9,000 on August 31, 2019. The trademark is considered to have an indefinite life. The fair value of the trademark on December 31, 2020, is $4,500. 3. Goodwill: Stiller recorded goodwill in January 2019, related to a purchase of another company. The carrying value of goodwill is $54,000 on December 31, 2020. On December 31, 2020, the segment for which the goodwill relates had a fair value of $1,044,000. The book value of the net assets of the segment (including goodwill) is $1,080,000. Note: Round each of your answers to the nearest whole dollar. a. Classify each of the intangible assets above as a finite life intangible or an indefinite life intangible. Patent Trademark Indefinite life intangible v Finite life intangible Goodwill Indefinite life intangible b. Determine the carrying value of each asset on December 31, 2020, prior to testing for impairment, assuming that the company uses the straight-line method Carrying value of patent, Dec. 31, 2020, before impairment testing Carrying value of trademark, Dec. 31, 2020, before impairment testing s Carrying value of goodwill, Dec. 31, 2020, before impairment testing amortize intangible assets, and no impairment was reported prior to 2020. 153,000 x 9,000 v 54,000 v c. Test each asset for impairment assuming that the qualitative assessment indicated that further impairment testing was warranted. Determine the carrying value of each asset on December 31, 2020, after impairment testing. Carrying value of patent, Dec. 31, 2020, after impairment testing 15,000 x Carrying value of trademark, Dec. 31, 2020, after impairment testing s 4,500 Carrying value of goodwill, Dec. 31, 2020, after impairment testing 18.000 v

Intermediate Accounting: Reporting And Analysis

3rd Edition

ISBN:9781337788281

Author:James M. Wahlen, Jefferson P. Jones, Donald Pagach

Publisher:James M. Wahlen, Jefferson P. Jones, Donald Pagach

Chapter12: Intangibles

Section: Chapter Questions

Problem 8P

Related questions

Question

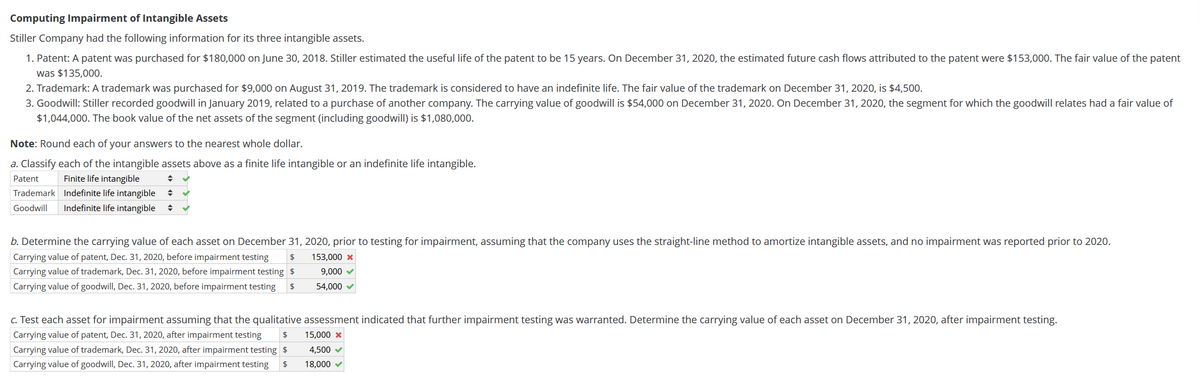

Transcribed Image Text:Computing Impairment of Intangible Assets

Stiller Company had the following information for its three intangible assets.

1. Patent: A patent was purchased for $180,000 on June 30, 2018. Stiller estimated the useful life of the patent to be 15 years. On December 31, 2020, the estimated future cash flows attributed to the patent were $153,000. The fair value of the patent

was $135,000.

2. Trademark: A trademark was purchased for $9,000 on August 31, 2019. The trademark is considered to have an indefinite life. The fair value of the trademark on December 31, 2020, is $4,500.

3. Goodwill: Stiller recorded goodwill in January 2019, related to a purchase of another company. The carrying value of goodwill is $54,000 on December 31, 2020. On December 31, 2020, the segment for which the goodwill relates had a fair value of

$1,044,000. The book value of the net assets of the segment (including goodwill) is $1,080,000.

Note: Round each of your answers to the nearest whole dollar.

a. Classify each of the intangible assets above as a finite life intangible or an indefinite life intangible.

Patent

Finite life intangible

Trademark Indefinite life intangible

Goodwill

Indefinite life intangible

b. Determine the carrying value of each asset on December 31, 2020, prior to testing for impairment, assuming that the company uses the straight-line method to amortize intangible assets, and no impairment was reported prior to 2020.

31, 2020, before impairment testing

Carrying value of trademark, Dec. 31, 2020, before impairment testing $

Carrying value of goodwill, Dec. 31, 2020, before impairment testing

Carrying value of patent,

153,000 x

9,000 v

2$

54,000

c. Test each asset for impairment assuming that the qualitative assessment indicated that further impairment testing was warranted. Determine the carrying value of each asset on December 31, 2020, after impairment testing.

Carrying value of patent, Dec. 31, 2020, after impairment testing

$

15,000 x

Carrying value of trademark, Dec. 31, 2020, after impairment testing $

4,500 v

Carrying value of goodwill, Dec. 31, 2020, after impairment testing

$

18,000 v

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution!

Trending now

This is a popular solution!

Step by step

Solved in 3 steps with 3 images

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, accounting and related others by exploring similar questions and additional content below.Recommended textbooks for you

Intermediate Accounting: Reporting And Analysis

Accounting

ISBN:

9781337788281

Author:

James M. Wahlen, Jefferson P. Jones, Donald Pagach

Publisher:

Cengage Learning

Cornerstones of Financial Accounting

Accounting

ISBN:

9781337690881

Author:

Jay Rich, Jeff Jones

Publisher:

Cengage Learning

Principles of Accounting Volume 1

Accounting

ISBN:

9781947172685

Author:

OpenStax

Publisher:

OpenStax College

Intermediate Accounting: Reporting And Analysis

Accounting

ISBN:

9781337788281

Author:

James M. Wahlen, Jefferson P. Jones, Donald Pagach

Publisher:

Cengage Learning

Cornerstones of Financial Accounting

Accounting

ISBN:

9781337690881

Author:

Jay Rich, Jeff Jones

Publisher:

Cengage Learning

Principles of Accounting Volume 1

Accounting

ISBN:

9781947172685

Author:

OpenStax

Publisher:

OpenStax College

Financial Accounting: The Impact on Decision Make…

Accounting

ISBN:

9781305654174

Author:

Gary A. Porter, Curtis L. Norton

Publisher:

Cengage Learning