Consider an inverse floating rate coupon bond with 1 year remaining to maturity. On maturity, bondholders are expected to receive $100 face value. Coupons are paid quarterly and the current 3-mth LIBOR observed rate is 5.234% p.a. The annual coupon rate is specified as: Annual coupon rate = 20% p.a. – 3C where Cis the annual 3-mth LIBOR rate. Assume, for simplicity, that the annual 3-mth LIBOR rate will never exceed 6.67% p.a. (so that the annual coupon rate defined above is always a positive number). The following table shows the current LIBOR continuously compounded rate with different maturities: Maturity LIBOR Maturity LIBOR 5.0% р.a. 5.1% р.a. 5.2% р.a. 5.3% р.a. 5.3% р,а. 5.4% p.a. 5.5% р.а. 5.5% p.a. 5.6% p.a. 5.7% p.a. 1 7 2 8 3 4 10 11 5.8% p.a. 12 5.9% p.a For example, the 1-mth LIBOR is 5.0% p.a. compounded continuously. You can treat the LIBOR rates presented in table above as the discount rates/spot rates with different maturities. Required: What is the current price of the inverse floating rate coupon bond? Show all of your workings.

Consider an inverse floating rate coupon bond with 1 year remaining to maturity. On maturity, bondholders are expected to receive $100 face value. Coupons are paid quarterly and the current 3-mth LIBOR observed rate is 5.234% p.a. The annual coupon rate is specified as: Annual coupon rate = 20% p.a. – 3C where Cis the annual 3-mth LIBOR rate. Assume, for simplicity, that the annual 3-mth LIBOR rate will never exceed 6.67% p.a. (so that the annual coupon rate defined above is always a positive number). The following table shows the current LIBOR continuously compounded rate with different maturities: Maturity LIBOR Maturity LIBOR 5.0% р.a. 5.1% р.a. 5.2% р.a. 5.3% р.a. 5.3% р,а. 5.4% p.a. 5.5% р.а. 5.5% p.a. 5.6% p.a. 5.7% p.a. 1 7 2 8 3 4 10 11 5.8% p.a. 12 5.9% p.a For example, the 1-mth LIBOR is 5.0% p.a. compounded continuously. You can treat the LIBOR rates presented in table above as the discount rates/spot rates with different maturities. Required: What is the current price of the inverse floating rate coupon bond? Show all of your workings.

Chapter8: Analysis Of Risk And Return

Section: Chapter Questions

Problem 9P

Related questions

Question

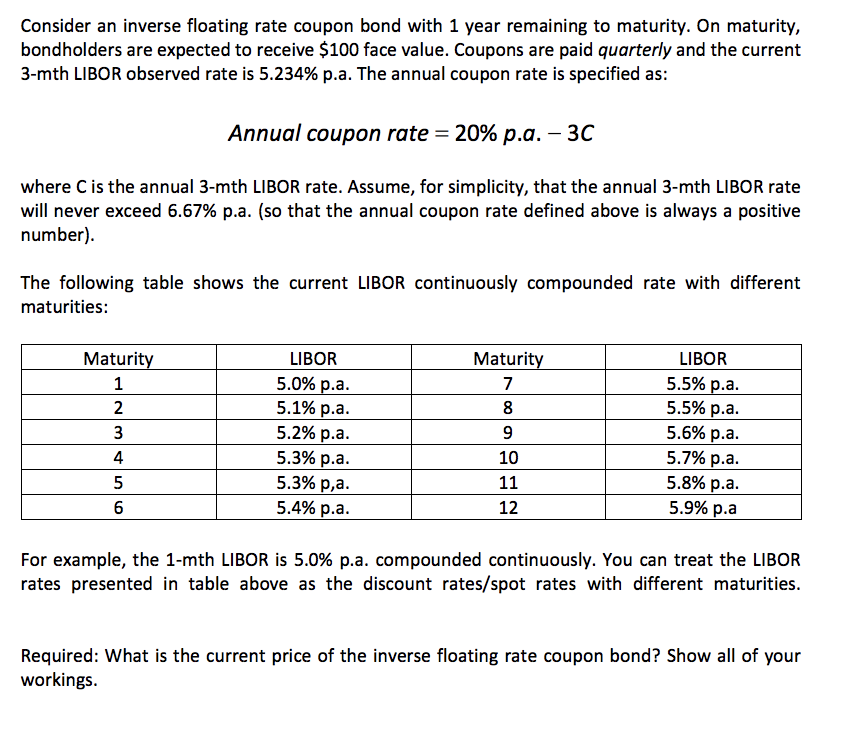

Transcribed Image Text:Consider an inverse floating rate coupon bond with 1 year remaining to maturity. On maturity,

bondholders are expected to receive $100 face value. Coupons are paid quarterly and the current

3-mth LIBOR observed rate is 5.234% p.a. The annual coupon rate is specified as:

Annual coupon rate = 20% p.a. – 30

where Cis the annual 3-mth LIBOR rate. Assume, for simplicity, that the annual 3-mth LIBOR rate

will never exceed 6.67% p.a. (so that the annual coupon rate defined above is always a positive

number).

The following table shows the current LIBOR continuously compounded rate with different

maturities:

Maturity

LIBOR

Maturity

LIBOR

5.0% р.а.

5.1% р.а.

5.2% р.а.

5.3% p.a.

5.3% p,a.

5.4% p.a.

5.5% p.a.

5.5% р.a.

5.6% p.a.

5.7% р.a.

5.8% p.a.

1

7

2

8

3

4

10

11

6

12

5.9% p.a

For example, the 1-mth LIBOR is 5.0% p.a. compounded continuously. You can treat the LIBOR

rates presented in table above as the discount rates/spot rates with different maturities.

Required: What is the current price of the inverse floating rate coupon bond? Show all of your

workings.

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution!

Trending now

This is a popular solution!

Step by step

Solved in 7 steps with 2 images

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, finance and related others by exploring similar questions and additional content below.Recommended textbooks for you

EBK CONTEMPORARY FINANCIAL MANAGEMENT

Finance

ISBN:

9781337514835

Author:

MOYER

Publisher:

CENGAGE LEARNING - CONSIGNMENT

Intermediate Financial Management (MindTap Course…

Finance

ISBN:

9781337395083

Author:

Eugene F. Brigham, Phillip R. Daves

Publisher:

Cengage Learning

EBK CONTEMPORARY FINANCIAL MANAGEMENT

Finance

ISBN:

9781337514835

Author:

MOYER

Publisher:

CENGAGE LEARNING - CONSIGNMENT

Intermediate Financial Management (MindTap Course…

Finance

ISBN:

9781337395083

Author:

Eugene F. Brigham, Phillip R. Daves

Publisher:

Cengage Learning