Cost Flow Methods The following three identical units of Item Alpha are purchased during April: Item Alpha Units Cost Apr. Purchase $76 14 Purchase 1 81 28 Purchase 1 83 Total 3 $240 Average cost per unit $80 ($240 + 3 units) Assume that one unit is sold on April 30 for $132. Determine the gross profit for April and ending inventory on April 30 using the (a) first-in, first-out (FIFO); (b) last-in, first-out (LIFO); and (c) weighted average cost methods. Gross Profit Ending Inventory a. First-in, first-out (FIFO) b. Last-in, first-out (LIFO) c. Weighted average cost Feedback YCheck My Wok a. Sales - cost of merchandise sold - gross profit. FIFO means that the first units purchased are assumed to be the first to be sold. Therefore, ending inventory is made up of the most recent purchases. b. Sales - cost of merchandise sold gross profit. LIFO means the last units purchased are assumed to be the first to be sold. Therefore, ending inventory is made up of the first purchases. c. Sales - cost of merchandise sold - gross profit. Average cost means the average cost of all available units purchased is applied to the number of units sold and in ending inventory.

Cost Flow Methods The following three identical units of Item Alpha are purchased during April: Item Alpha Units Cost Apr. Purchase $76 14 Purchase 1 81 28 Purchase 1 83 Total 3 $240 Average cost per unit $80 ($240 + 3 units) Assume that one unit is sold on April 30 for $132. Determine the gross profit for April and ending inventory on April 30 using the (a) first-in, first-out (FIFO); (b) last-in, first-out (LIFO); and (c) weighted average cost methods. Gross Profit Ending Inventory a. First-in, first-out (FIFO) b. Last-in, first-out (LIFO) c. Weighted average cost Feedback YCheck My Wok a. Sales - cost of merchandise sold - gross profit. FIFO means that the first units purchased are assumed to be the first to be sold. Therefore, ending inventory is made up of the most recent purchases. b. Sales - cost of merchandise sold gross profit. LIFO means the last units purchased are assumed to be the first to be sold. Therefore, ending inventory is made up of the first purchases. c. Sales - cost of merchandise sold - gross profit. Average cost means the average cost of all available units purchased is applied to the number of units sold and in ending inventory.

Financial Accounting: The Impact on Decision Makers

10th Edition

ISBN:9781305654174

Author:Gary A. Porter, Curtis L. Norton

Publisher:Gary A. Porter, Curtis L. Norton

Chapter5: Inventories And Cost Of Goods Sold

Section: Chapter Questions

Problem 5.24MCE

Related questions

Topic Video

Question

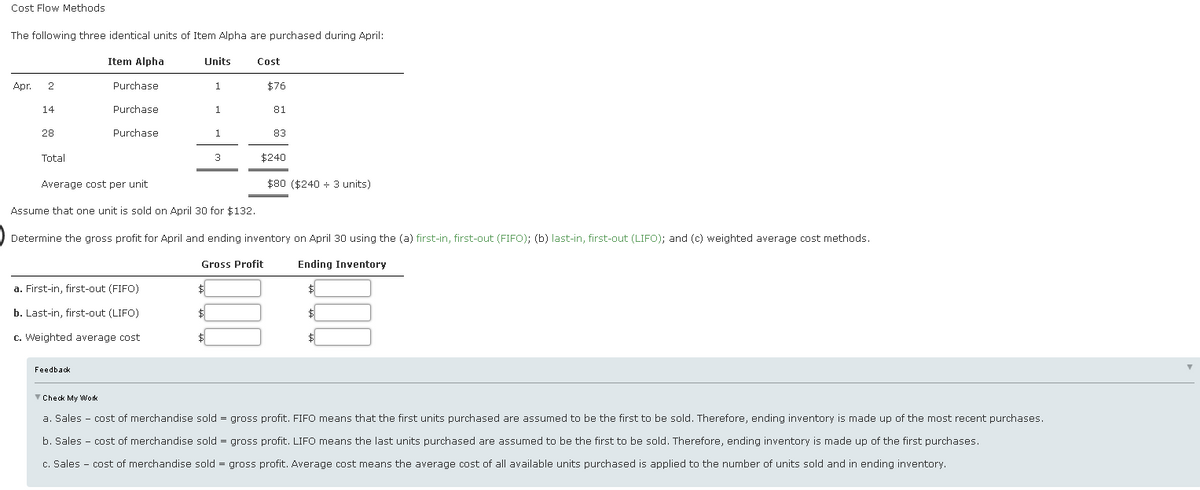

Transcribed Image Text:Cost Flow Methods

The following three identical units of Item Alpha are purchased during April:

Item Alpha

Units

Cost

Apr.

Purchase

1

$76

14

Purchase

1.

81

28

Purchase

1

83

Total

3

$240

Average cost per unit

$80 ($240 + 3 units)

Assume that one unit is sold on April 30 for $132.

Determine the gross profit for April and ending inventory on April 30 using the (a) first-in, first-out (FIFO); (b) last-in, first-out (LIFO); and (c) weighted average cost methods.

Gross Profit

Ending Inventory

a. First-in, first-out (FIFO)

$

b. Last-in, first-out (LIFO)

$

c. Weighted average cost

$

Feedback

V Check My Work

a. Sales - cost of merchandise sold = gross profit. FIFO means that the first units purchased are assumed to be the first to be sold. Therefore, ending inventory is made up of the most recent purchases.

b. Sales - cost of merchandise sold = gross profit. LIFO means the last units purchased are assumed to be the first to be sold. Therefore, ending inventory is made up of the first purchases.

c. Sales - cost of merchandise sold = gross profit. Average cost means the average cost of all available units purchased is applied to the number of units sold and in ending inventory.

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution!

Trending now

This is a popular solution!

Step by step

Solved in 3 steps

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, accounting and related others by exploring similar questions and additional content below.Recommended textbooks for you

Financial Accounting: The Impact on Decision Make…

Accounting

ISBN:

9781305654174

Author:

Gary A. Porter, Curtis L. Norton

Publisher:

Cengage Learning

Financial Accounting

Accounting

ISBN:

9781337272124

Author:

Carl Warren, James M. Reeve, Jonathan Duchac

Publisher:

Cengage Learning

College Accounting, Chapters 1-27

Accounting

ISBN:

9781337794756

Author:

HEINTZ, James A.

Publisher:

Cengage Learning,

Financial Accounting: The Impact on Decision Make…

Accounting

ISBN:

9781305654174

Author:

Gary A. Porter, Curtis L. Norton

Publisher:

Cengage Learning

Financial Accounting

Accounting

ISBN:

9781337272124

Author:

Carl Warren, James M. Reeve, Jonathan Duchac

Publisher:

Cengage Learning

College Accounting, Chapters 1-27

Accounting

ISBN:

9781337794756

Author:

HEINTZ, James A.

Publisher:

Cengage Learning,

Financial Accounting

Accounting

ISBN:

9781305088436

Author:

Carl Warren, Jim Reeve, Jonathan Duchac

Publisher:

Cengage Learning

Survey of Accounting (Accounting I)

Accounting

ISBN:

9781305961883

Author:

Carl Warren

Publisher:

Cengage Learning