Exercise 5.2 Suppose you pay 5 to buy a European (K = 100, t = 1/2) put option on a given security. Assuming a nominal annual in- terest rate of 6 percent, compounded monthly, find the present value of your return from this investment if (a) S(1/2) = 102; (b) S(1/2) = 98.

Exercise 5.2 Suppose you pay 5 to buy a European (K = 100, t = 1/2) put option on a given security. Assuming a nominal annual in- terest rate of 6 percent, compounded monthly, find the present value of your return from this investment if (a) S(1/2) = 102; (b) S(1/2) = 98.

Chapter11: Managing Transaction Exposure

Section: Chapter Questions

Problem 56QA

Related questions

Question

hi could you please help solve questions 5.2?

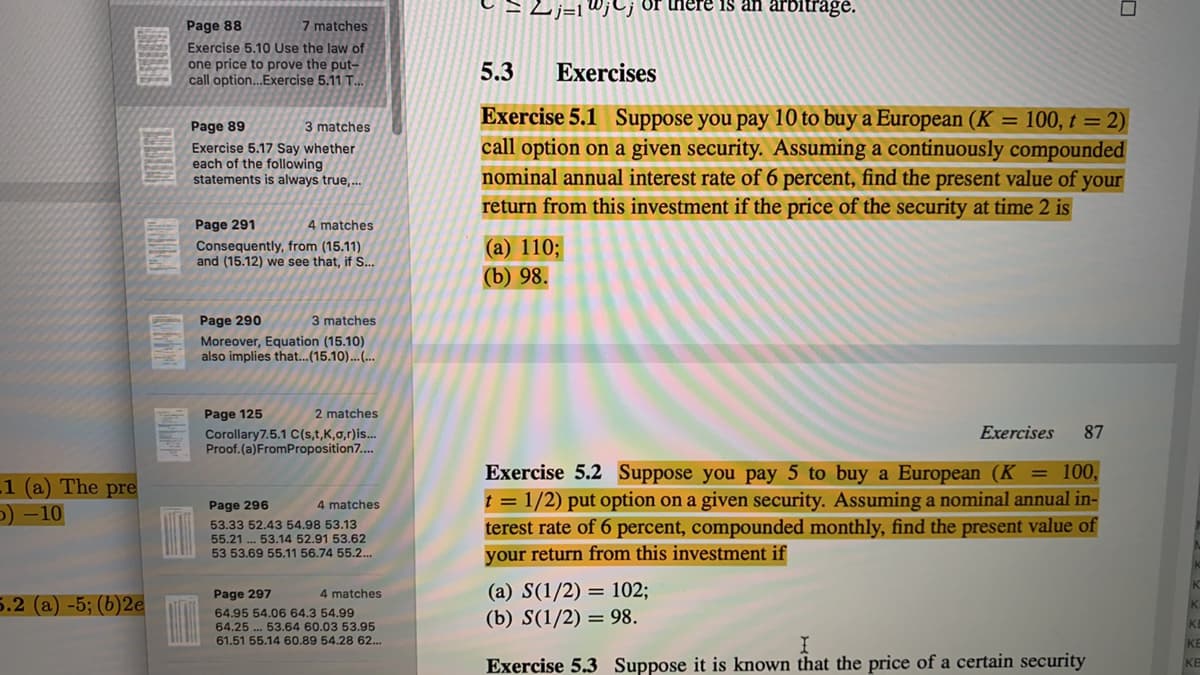

Transcribed Image Text:W;C; Or there is an arbitrage.

Page 88

7 matches

Exercise 5.10 Use the law of

one price to prove the put-

call option..Exercise 5.11 T.

5.3

Exercises

Exercise 5.1 Suppose you pay 10 to buy a European (K = 100, t = 2)

call option on a given security. Assuming a continuously compounded

nominal annual interest rate of 6 percent, find the present value of your

return from this investment if the price of the security at time 2 is

Page 89

3 matches

Exercise 5.17 Say whether

each of the following

statements is always true,..

Page 291

4 matches

Consequently, from (15.11)

and (15.12) we see that, if S..

(a) 110;

(b) 98.

Page 290

3 matches

Moreover, Equation (15.10)

also implies that...(15.10)...(...

Page 125

2 matches

Exercises

87

Corollary7.5.1 C(s,t,K,0,r)is...

Proof.(a)FromProposition7..

Exercise 5.2 Suppose you pay 5 to buy a European (K= 100,

t = 1/2) put option on a given security. Assuming a nominal annual in-

terest rate of 6 percent, compounded monthly, find the present value of

your return from this investment if

1 (a) The pre

O) -10

Page 296

4 matches

53.33 52.43 54.98 53.13

55.21 .. 53.14 52.91 53.62

53 53.69 55.11 56.74 55.2..

(a) S(1/2) = 102;

(b) S(1/2) = 98.

Page 297

4 matches

5.2 (a) -5; (b)2e

64.95 54.06 64.3 54.99

64.25 . 53.64 60.03 53.95

61.51 55.14 60.89 54.28 62..

Exercise 5.3 Suppose it is known that the price of a certain security

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution!

Trending now

This is a popular solution!

Step by step

Solved in 3 steps

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, finance and related others by exploring similar questions and additional content below.Recommended textbooks for you