EXHIBIT 7.64.1 a. Sales recorded, goods not shipped b. Goods shipped, sales not recorded C. Goods shipped to a bad credit risk customer d. Sales billed at the wrong price or wrong quantity е. Product line A sales recorded as Product line B f. Failure to post charges to customers for sales g. January sales recorded in December CONTROL PROCEDURES 1. Sales order approved for credit 2. Prenumbered shipping doc prepared, sequence checked 3. Shipping document quantity compared to sales invoice 4. Prenumbered sales invoices, sequence checked 5. Sales invoice checked to sales order 6. Invoiced prices compared to approved price list 7. General ledger code checked for sales product lines 8. Sales dollar batch totals compared to sales journal 9. Periodic sales total compared to same period accounts receivable postings 10. Accountants have instructions to date sales on the date of shipment 11. Sales entry date compared to shipping doc date 12. Accounts receivable subsidiary totaled and reconciled to accounts receivable control account 13. Intercompany accounts reconciled with subsidiary company records 14. Credit files updated for customer payment history 15. Overdue customer accounts investigated for collection

EXHIBIT 7.64.1 a. Sales recorded, goods not shipped b. Goods shipped, sales not recorded C. Goods shipped to a bad credit risk customer d. Sales billed at the wrong price or wrong quantity е. Product line A sales recorded as Product line B f. Failure to post charges to customers for sales g. January sales recorded in December CONTROL PROCEDURES 1. Sales order approved for credit 2. Prenumbered shipping doc prepared, sequence checked 3. Shipping document quantity compared to sales invoice 4. Prenumbered sales invoices, sequence checked 5. Sales invoice checked to sales order 6. Invoiced prices compared to approved price list 7. General ledger code checked for sales product lines 8. Sales dollar batch totals compared to sales journal 9. Periodic sales total compared to same period accounts receivable postings 10. Accountants have instructions to date sales on the date of shipment 11. Sales entry date compared to shipping doc date 12. Accounts receivable subsidiary totaled and reconciled to accounts receivable control account 13. Intercompany accounts reconciled with subsidiary company records 14. Credit files updated for customer payment history 15. Overdue customer accounts investigated for collection

College Accounting (Book Only): A Career Approach

13th Edition

ISBN:9781337280570

Author:Scott, Cathy J.

Publisher:Scott, Cathy J.

Chapter10: Cash Receipts And Cash Payments

Section: Chapter Questions

Problem 6E: Record general journal entries to correct the errors described below. Assume that the incorrect...

Related questions

Question

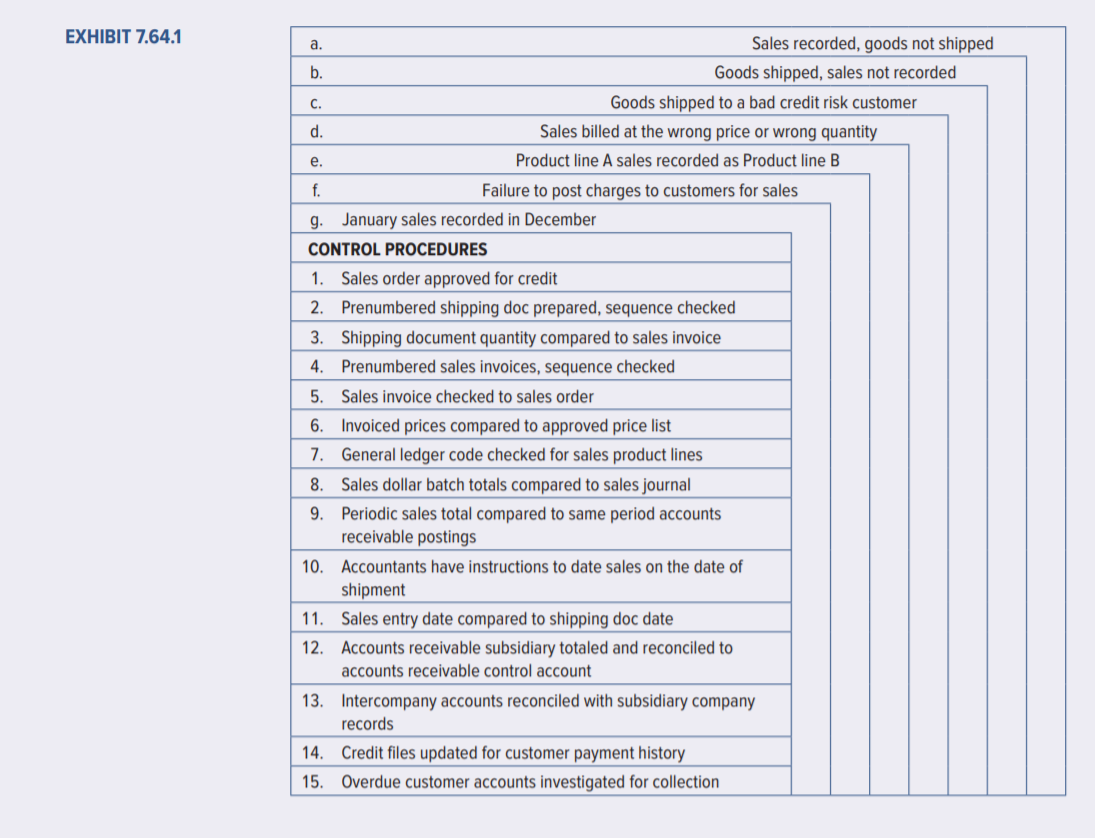

Assertion Associations. Exhibit 7.64.1 contains an arrangement of examples of transaction errors (lettered a–g) and a set of client control procedures and devices (numbered 1–15).

Required:

For each error/control objective, identify the assertion about classes of transactions and events most benefited by the control.

Transcribed Image Text:EXHIBIT 7.64.1

a.

Sales recorded, goods not shipped

b.

Goods shipped, sales not recorded

C.

Goods shipped to a bad credit risk customer

d.

Sales billed at the wrong price or wrong quantity

е.

Product line A sales recorded as Product line B

f.

Failure to post charges to customers for sales

g. January sales recorded in December

CONTROL PROCEDURES

1. Sales order approved for credit

2. Prenumbered shipping doc prepared, sequence checked

3. Shipping document quantity compared to sales invoice

4. Prenumbered sales invoices, sequence checked

5. Sales invoice checked to sales order

6. Invoiced prices compared to approved price list

7. General ledger code checked for sales product lines

8. Sales dollar batch totals compared to sales journal

9. Periodic sales total compared to same period accounts

receivable postings

10. Accountants have instructions to date sales on the date of

shipment

11. Sales entry date compared to shipping doc date

12. Accounts receivable subsidiary totaled and reconciled to

accounts receivable control account

13. Intercompany accounts reconciled with subsidiary company

records

14. Credit files updated for customer payment history

15.

Overdue customer accounts investigated for collection

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution!

Trending now

This is a popular solution!

Step by step

Solved in 3 steps with 5 images

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, accounting and related others by exploring similar questions and additional content below.Recommended textbooks for you

College Accounting (Book Only): A Career Approach

Accounting

ISBN:

9781337280570

Author:

Scott, Cathy J.

Publisher:

South-Western College Pub

College Accounting (Book Only): A Career Approach

Accounting

ISBN:

9781337280570

Author:

Scott, Cathy J.

Publisher:

South-Western College Pub

Century 21 Accounting Multicolumn Journal

Accounting

ISBN:

9781337679503

Author:

Gilbertson

Publisher:

Cengage

Survey of Accounting (Accounting I)

Accounting

ISBN:

9781305961883

Author:

Carl Warren

Publisher:

Cengage Learning