Foxeye Company provided the following information for the current year: Income from continuing operations Income from discontinued operations Unrealized gain on financial asset – FVPL Unrealized loss on equity investment – FVOCI Unrealized gain on debt investment – FVOCI Unrealized gain on futures contract designated as a cash flow hedge Translation loss on foreign operation Net “remeasurement" gain on defined benefit plan Loss on credit risk of a financial liability at FVPL Revaluation surplus during the year 4,000,000 500,000 800,000 1,000,000 1,200,000 400,000 200,000 600,000 300,000 2,500,000

Foxeye Company provided the following information for the current year: Income from continuing operations Income from discontinued operations Unrealized gain on financial asset – FVPL Unrealized loss on equity investment – FVOCI Unrealized gain on debt investment – FVOCI Unrealized gain on futures contract designated as a cash flow hedge Translation loss on foreign operation Net “remeasurement" gain on defined benefit plan Loss on credit risk of a financial liability at FVPL Revaluation surplus during the year 4,000,000 500,000 800,000 1,000,000 1,200,000 400,000 200,000 600,000 300,000 2,500,000

Intermediate Accounting: Reporting And Analysis

3rd Edition

ISBN:9781337788281

Author:James M. Wahlen, Jefferson P. Jones, Donald Pagach

Publisher:James M. Wahlen, Jefferson P. Jones, Donald Pagach

Chapter21: The Statement Of Cash Flows

Section: Chapter Questions

Problem 14GI: Dunn Company recognized a 5,000 unrealized holding gain on investment in Starbuckss long-term bonds...

Related questions

Question

a. What net amount should be reported as OCI for the current year?

b. What amount should be reported as comprehensive income for the current year?

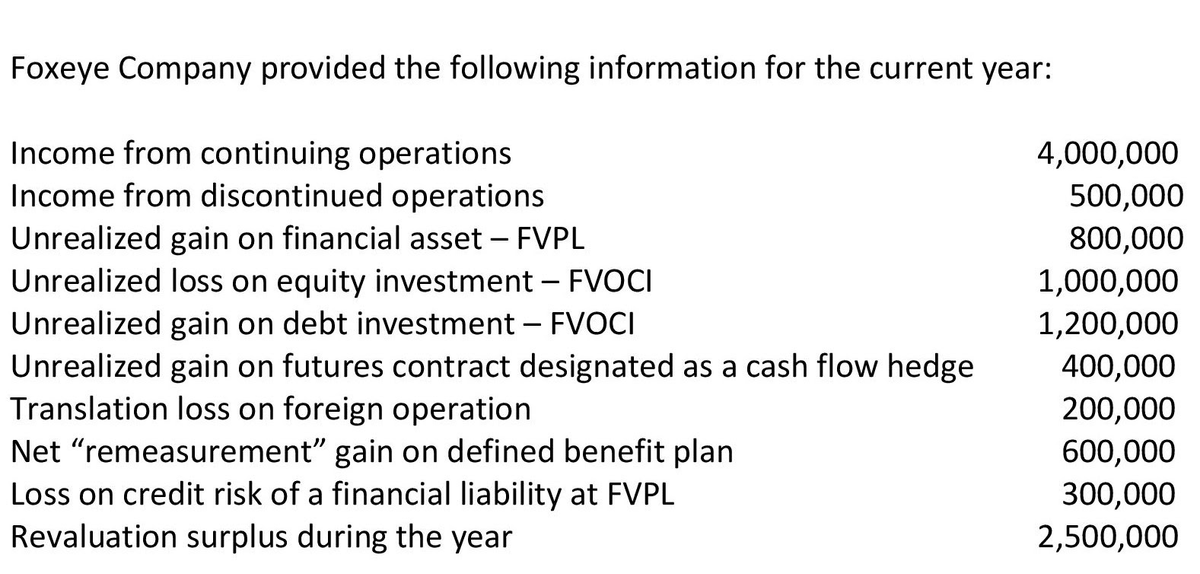

Transcribed Image Text:Foxeye Company provided the following information for the current year:

Income from continuing operations

Income from discontinued operations

4,000,000

500,000

Unrealized gain on financial asset – FVPL

Unrealized loss on equity investment – FVOCI

800,000

1,000,000

Unrealized gain on debt investment – FVOCI

Unrealized gain on futures contract designated as a cash flow hedge

Translation loss on foreign operation

Net "remeasurement" gain on defined benefit plan

Loss on credit risk of a financial liability at FVPL

Revaluation surplus during the year

1,200,000

400,000

200,000

600,000

300,000

2,500,000

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

Step by step

Solved in 2 steps with 2 images

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, accounting and related others by exploring similar questions and additional content below.Recommended textbooks for you

Intermediate Accounting: Reporting And Analysis

Accounting

ISBN:

9781337788281

Author:

James M. Wahlen, Jefferson P. Jones, Donald Pagach

Publisher:

Cengage Learning

Survey of Accounting (Accounting I)

Accounting

ISBN:

9781305961883

Author:

Carl Warren

Publisher:

Cengage Learning

Intermediate Accounting: Reporting And Analysis

Accounting

ISBN:

9781337788281

Author:

James M. Wahlen, Jefferson P. Jones, Donald Pagach

Publisher:

Cengage Learning

Survey of Accounting (Accounting I)

Accounting

ISBN:

9781305961883

Author:

Carl Warren

Publisher:

Cengage Learning