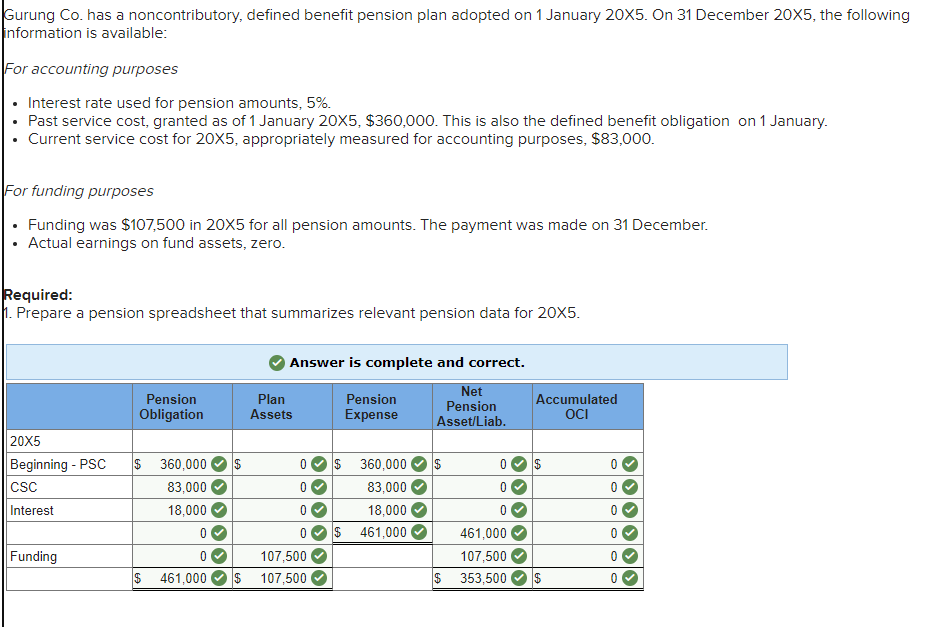

Gurung Co. has a noncontributory, defined benefit pension plan adopted on 1 January 20X5. On 31 December 20X5, the following information is available: For accounting purposes Interest rate used for pension amounts, 5%. Past service cost, granted as of 1 January 20X5, $360,000. This is also the defined benefit obligation on 1 January. Current service cost for 20X5, appropriately measured for accounting purposes, $83,000. For funding purposes Funding was $107,500 in 20X5 for all pension amounts. The payment was made on 31 December. Actual earnings on fund assets, zero. Required: 1. Prepare a pension spreadsheet that summarizes relevant pension data for 20X5. Answer is complete and correct. Pension Obligation Plan Assets Pension Expense Net Pension Asset/Liab. Accumulated OCI 20X5 Beginning - PSC $ 360,000 $ 0 $ 360,000 $ 0 $ 0 CSC 83,000 0 83,000 0 0 Interest 18,000 0 18,000 0 0 0 $ 461,000 461,000 0 Funding 107,500 107,500 0 $ 461,000 $ 107,500 $ 353,500 0 2. Prepare a pension spreadsheet that summarizes relevant pension data for 20X6. The following facts relate to 20X6: • Current service cost for accounting was $128,000. • A plan amendment on 1 January resulted in a past service cost of $56,000 being granted. • Total funding of the pension plan was $134,000, on 31 December 20X6. • Actual return on fund assets was $10,500. • An actuarial revaluation was done to reflect new information about expected turnover rates in the employee population. This resulted in a $51,000 increase in the defined benefit obligation, as of 31 December 20X6. 20X6 Opening CSC Net interest PSC (new) Actuarial gains/losses Revaluation Funding Pension Obligation Answer is complete but not entirely correct. Plan Assets Net Pension Expense Pension Asset/Liab. Accumulated OCI $ 461,000 ( $ 107,500 $ 0 $ 353,500 $ 128,000 23,050 x 128,000 0 5,375 17,675 × 56,000 0 0 ☑ 0 0 0 5,125 51,000 0 56,000 × 0 5,125 5,125 51,000 51,000 0 0 $ 201,675 x 201,675 x 0 134,000 134,000 $ 719,050 $ 252,000 $ 467,050 $ 45,875

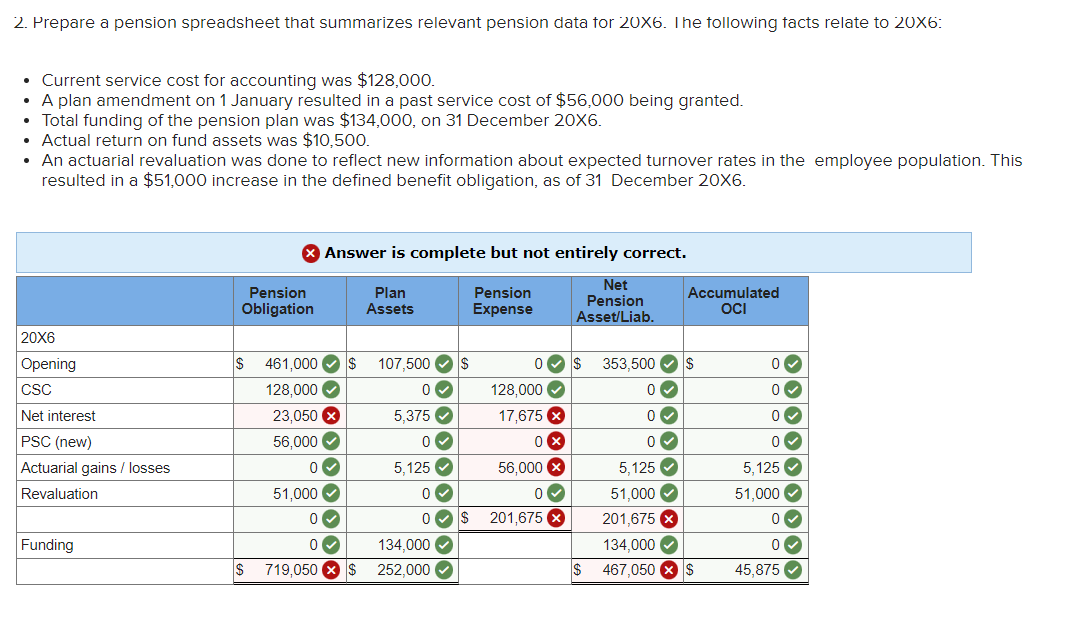

Gurung Co. has a noncontributory, defined benefit pension plan adopted on 1 January 20X5. On 31 December 20X5, the following information is available: For accounting purposes Interest rate used for pension amounts, 5%. Past service cost, granted as of 1 January 20X5, $360,000. This is also the defined benefit obligation on 1 January. Current service cost for 20X5, appropriately measured for accounting purposes, $83,000. For funding purposes Funding was $107,500 in 20X5 for all pension amounts. The payment was made on 31 December. Actual earnings on fund assets, zero. Required: 1. Prepare a pension spreadsheet that summarizes relevant pension data for 20X5. Answer is complete and correct. Pension Obligation Plan Assets Pension Expense Net Pension Asset/Liab. Accumulated OCI 20X5 Beginning - PSC $ 360,000 $ 0 $ 360,000 $ 0 $ 0 CSC 83,000 0 83,000 0 0 Interest 18,000 0 18,000 0 0 0 $ 461,000 461,000 0 Funding 107,500 107,500 0 $ 461,000 $ 107,500 $ 353,500 0 2. Prepare a pension spreadsheet that summarizes relevant pension data for 20X6. The following facts relate to 20X6: • Current service cost for accounting was $128,000. • A plan amendment on 1 January resulted in a past service cost of $56,000 being granted. • Total funding of the pension plan was $134,000, on 31 December 20X6. • Actual return on fund assets was $10,500. • An actuarial revaluation was done to reflect new information about expected turnover rates in the employee population. This resulted in a $51,000 increase in the defined benefit obligation, as of 31 December 20X6. 20X6 Opening CSC Net interest PSC (new) Actuarial gains/losses Revaluation Funding Pension Obligation Answer is complete but not entirely correct. Plan Assets Net Pension Expense Pension Asset/Liab. Accumulated OCI $ 461,000 ( $ 107,500 $ 0 $ 353,500 $ 128,000 23,050 x 128,000 0 5,375 17,675 × 56,000 0 0 ☑ 0 0 0 5,125 51,000 0 56,000 × 0 5,125 5,125 51,000 51,000 0 0 $ 201,675 x 201,675 x 0 134,000 134,000 $ 719,050 $ 252,000 $ 467,050 $ 45,875

Intermediate Accounting: Reporting And Analysis

3rd Edition

ISBN:9781337788281

Author:James M. Wahlen, Jefferson P. Jones, Donald Pagach

Publisher:James M. Wahlen, Jefferson P. Jones, Donald Pagach

Chapter19: Accounting For Post Retirement Benefits

Section: Chapter Questions

Problem 5E

Related questions

Question

Please fix the ones with red cross marks. Fill the tables.

Transcribed Image Text:Gurung Co. has a noncontributory, defined benefit pension plan adopted on 1 January 20X5. On 31 December 20X5, the following

information is available:

For accounting purposes

Interest rate used for pension amounts, 5%.

Past service cost, granted as of 1 January 20X5, $360,000. This is also the defined benefit obligation on 1 January.

Current service cost for 20X5, appropriately measured for accounting purposes, $83,000.

For funding purposes

Funding was $107,500 in 20X5 for all pension amounts. The payment was made on 31 December.

Actual earnings on fund assets, zero.

Required:

1. Prepare a pension spreadsheet that summarizes relevant pension data for 20X5.

Answer is complete and correct.

Pension

Obligation

Plan

Assets

Pension

Expense

Net

Pension

Asset/Liab.

Accumulated

OCI

20X5

Beginning - PSC $ 360,000

$

0 $ 360,000

$

0

$

0

CSC

83,000

0

83,000

0

0

Interest

18,000

0

18,000

0

0

0

$ 461,000

461,000

0

Funding

107,500

107,500

0

$ 461,000 $

107,500

$

353,500

0

Transcribed Image Text:2. Prepare a pension spreadsheet that summarizes relevant pension data for 20X6. The following facts relate to 20X6:

• Current service cost for accounting was $128,000.

• A plan amendment on 1 January resulted in a past service cost of $56,000 being granted.

• Total funding of the pension plan was $134,000, on 31 December 20X6.

• Actual return on fund assets was $10,500.

• An actuarial revaluation was done to reflect new information about expected turnover rates in the employee population. This

resulted in a $51,000 increase in the defined benefit obligation, as of 31 December 20X6.

20X6

Opening

CSC

Net interest

PSC (new)

Actuarial gains/losses

Revaluation

Funding

Pension

Obligation

Answer is complete but not entirely correct.

Plan

Assets

Net

Pension

Expense

Pension

Asset/Liab.

Accumulated

OCI

$ 461,000 (

$ 107,500

$

0

$ 353,500

$

128,000

23,050 x

128,000

0

5,375

17,675 ×

56,000

0

0 ☑

0

0

0

5,125

51,000

0

56,000 ×

0

5,125

5,125

51,000

51,000

0

0

$ 201,675 x

201,675 x

0

134,000

134,000

$ 719,050 $ 252,000

$ 467,050 $

45,875

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

Step by step

Solved in 1 steps

Recommended textbooks for you

Intermediate Accounting: Reporting And Analysis

Accounting

ISBN:

9781337788281

Author:

James M. Wahlen, Jefferson P. Jones, Donald Pagach

Publisher:

Cengage Learning

Individual Income Taxes

Accounting

ISBN:

9780357109731

Author:

Hoffman

Publisher:

CENGAGE LEARNING - CONSIGNMENT

Intermediate Accounting: Reporting And Analysis

Accounting

ISBN:

9781337788281

Author:

James M. Wahlen, Jefferson P. Jones, Donald Pagach

Publisher:

Cengage Learning

Individual Income Taxes

Accounting

ISBN:

9780357109731

Author:

Hoffman

Publisher:

CENGAGE LEARNING - CONSIGNMENT