How much is the goodwill (gain on bargain ourchase)?

Chapter7: Corporations: Reorganizations

Section: Chapter Questions

Problem 21P

Related questions

Question

How much is the

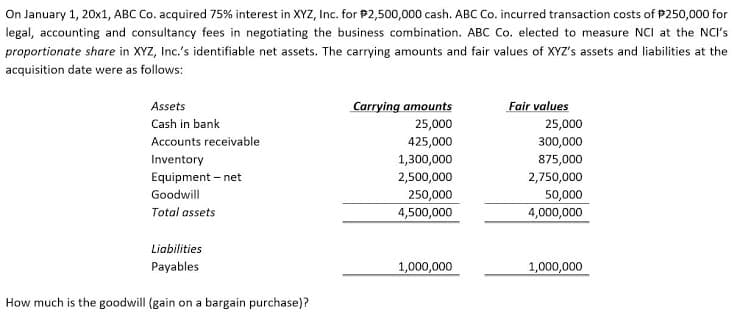

Transcribed Image Text:On January 1, 20x1, ABC Co. acquired 75% interest in XYZ, Inc. for P2,500,000 cash. ABC Co. incurred transaction costs of P250,000 for

legal, accounting and consultancy fees in negotiating the business combination. ABC Co. elected to measure NCI at the NCI's

proportionate share in XYZ, Inc.'s identifiable net assets. The carrying amounts and fair values of XYZ's assets and liabilities at the

acquisition date were as follows:

Carrying amounts

Fair values

Assets

Cash in bank

25,000

25,000

Accounts receivable

425,000

300,000

Inventory

1,300,000

875,000

Equipment – net

2,500,000

2,750,000

Goodwill

250,000

50,000

4,000,000

Total assets

4,500,000

Liabilities

Payables

1,000,000

1,000,000

How much is the goodwill (gain on a bargain purchase)?

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

Step by step

Solved in 2 steps

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, accounting and related others by exploring similar questions and additional content below.Recommended textbooks for you

Intermediate Accounting: Reporting And Analysis

Accounting

ISBN:

9781337788281

Author:

James M. Wahlen, Jefferson P. Jones, Donald Pagach

Publisher:

Cengage Learning