(i) Calculate the expected rate of return(r) and risk(o) for the following portfolios: 1.40% security 1 and 60% security 2 II.80% security 1 and 20% security 2 (ii) Given a risk-free rate of 4%, describe how Mr. Adani can use a combination of a risk- free instrument and a risky portfolio with an expected return of 15% to achieve an expected return of 26%.

(i) Calculate the expected rate of return(r) and risk(o) for the following portfolios: 1.40% security 1 and 60% security 2 II.80% security 1 and 20% security 2 (ii) Given a risk-free rate of 4%, describe how Mr. Adani can use a combination of a risk- free instrument and a risky portfolio with an expected return of 15% to achieve an expected return of 26%.

Chapter8: Analysis Of Risk And Return

Section: Chapter Questions

Problem 16P

Related questions

Question

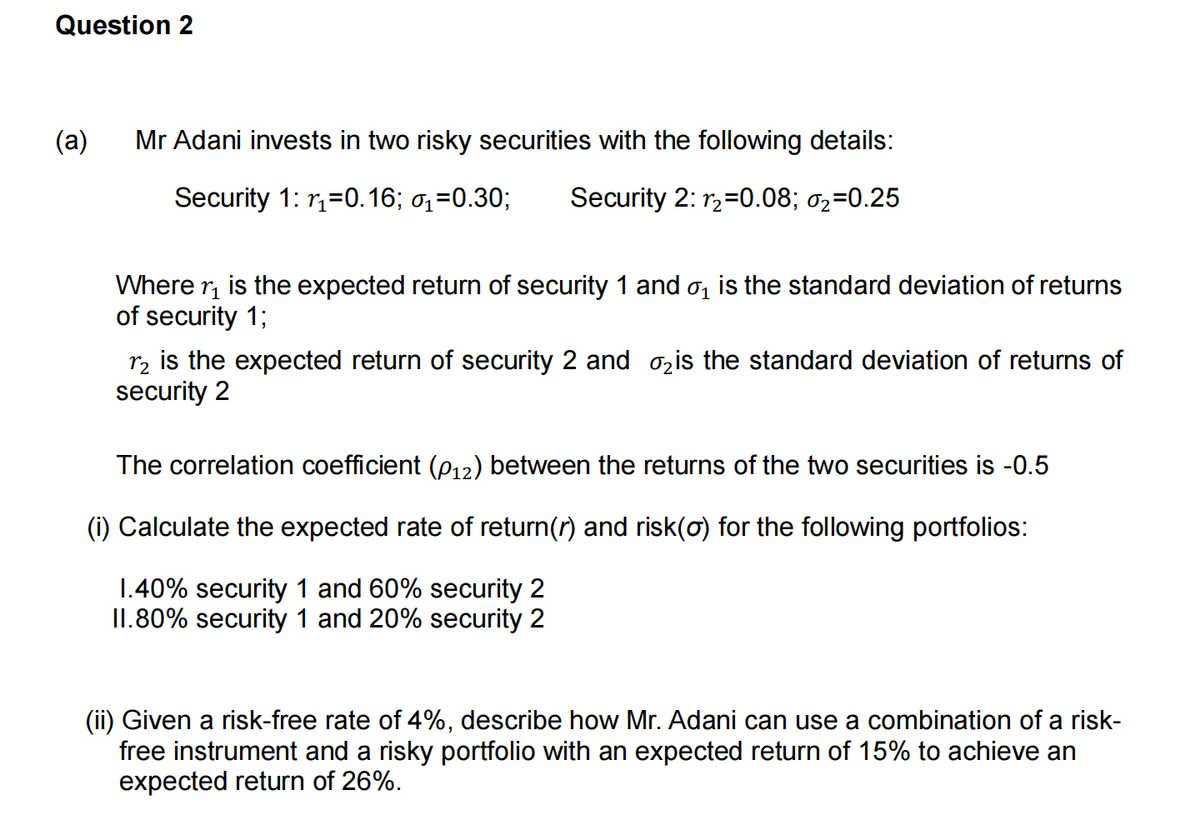

![Appendix: Formula sheet

1. P12 =

012

0102

Where P12: correlation coefficient between security 1 and security 2

012: covariance between security 1 and security 2

₁: standard deviation of security 1

0₂: standard deviation of security 2

2. 012 = 1 Pi [(R₁i — E (R₁)) ((R₂i – E(R₂)]

-

Where 12: covariance between security 1 and security 2

P₁: probabilities of the return at i

3.

R₁i: rate of return of security 1 at i

R₂i: rate of return of security 2 at i

E (R₁) expected rate of return of security 1

E (R₂) expected rate of return of security 2

02-012

W1(min)+02-2012

Where W₁(min): the weight of security 1 given the minimum variance in the two

securities case

012: covariance between security 1 and security 2

₁: standard deviation of security 1

0₂: standard deviation of security 2

o2: variance of security 2

4.02= w202 + w20₂ + 2w₁W₂010₂P12

Where

: variance of the portfolio

w₁: weighting of security 1

w₂: weighting of security 2

0₁: standard deviation of security 1

0₂: standard deviation of security 2

P12: correlation coefficient between security 1and security 2

5. VaR (0) = P (ασνΔt - μΔt)

Where P: investment position

a: one tailed probability of z value

σ: volatility (standard deviation)

At: time horizon/holding period

μ: expected annual return

(1+R₂) T

(1+Rpv)T

Where F: risk adjusted factor

6. F=-

RPV: the cost of capital of the project

R₁: the risk free rate

1-fd

fu-fa'

Where p: the probability of the cash flow Cu generated by the project

f and fa: deviation factors

o: the standard deviation

At: time horizon of the project

7. p=

fu=e°√At i fa=—=;

fu](/v2/_next/image?url=https%3A%2F%2Fcontent.bartleby.com%2Fqna-images%2Fquestion%2F55a2f5e2-2562-4a63-8199-89250e06b38a%2F1430b15c-85cd-4afe-aef1-cdc18ed44b2f%2Feqrbss7_processed.png&w=3840&q=75)

Transcribed Image Text:Appendix: Formula sheet

1. P12 =

012

0102

Where P12: correlation coefficient between security 1 and security 2

012: covariance between security 1 and security 2

₁: standard deviation of security 1

0₂: standard deviation of security 2

2. 012 = 1 Pi [(R₁i — E (R₁)) ((R₂i – E(R₂)]

-

Where 12: covariance between security 1 and security 2

P₁: probabilities of the return at i

3.

R₁i: rate of return of security 1 at i

R₂i: rate of return of security 2 at i

E (R₁) expected rate of return of security 1

E (R₂) expected rate of return of security 2

02-012

W1(min)+02-2012

Where W₁(min): the weight of security 1 given the minimum variance in the two

securities case

012: covariance between security 1 and security 2

₁: standard deviation of security 1

0₂: standard deviation of security 2

o2: variance of security 2

4.02= w202 + w20₂ + 2w₁W₂010₂P12

Where

: variance of the portfolio

w₁: weighting of security 1

w₂: weighting of security 2

0₁: standard deviation of security 1

0₂: standard deviation of security 2

P12: correlation coefficient between security 1and security 2

5. VaR (0) = P (ασνΔt - μΔt)

Where P: investment position

a: one tailed probability of z value

σ: volatility (standard deviation)

At: time horizon/holding period

μ: expected annual return

(1+R₂) T

(1+Rpv)T

Where F: risk adjusted factor

6. F=-

RPV: the cost of capital of the project

R₁: the risk free rate

1-fd

fu-fa'

Where p: the probability of the cash flow Cu generated by the project

f and fa: deviation factors

o: the standard deviation

At: time horizon of the project

7. p=

fu=e°√At i fa=—=;

fu

Transcribed Image Text:Question 2

(a)

Mr Adani invests in two risky securities with the following details:

Security 1: r₁=0.16; ₁=0.30; Security 2:1₂=0.08; 0₂=0.25

Where ₁ is the expected return of security 1 and ₁ is the standard deviation of returns

of security 1;

12 is the expected return of security 2 and ₂ is the standard deviation of returns of

security 2

The correlation coefficient (P12) between the returns of the two securities is -0.5

(i) Calculate the expected rate of return(r) and risk(o) for the following portfolios:

1.40% security 1 and 60% security 2

II.80% security 1 and 20% security 2

(ii) Given a risk-free rate of 4%, describe how Mr. Adani can use a combination of a risk-

free instrument and a risky portfolio with an expected return of 15% to achieve an

expected return of 26%.

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

Step by step

Solved in 4 steps with 2 images

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, finance and related others by exploring similar questions and additional content below.Recommended textbooks for you

EBK CONTEMPORARY FINANCIAL MANAGEMENT

Finance

ISBN:

9781337514835

Author:

MOYER

Publisher:

CENGAGE LEARNING - CONSIGNMENT

Intermediate Financial Management (MindTap Course…

Finance

ISBN:

9781337395083

Author:

Eugene F. Brigham, Phillip R. Daves

Publisher:

Cengage Learning

EBK CONTEMPORARY FINANCIAL MANAGEMENT

Finance

ISBN:

9781337514835

Author:

MOYER

Publisher:

CENGAGE LEARNING - CONSIGNMENT

Intermediate Financial Management (MindTap Course…

Finance

ISBN:

9781337395083

Author:

Eugene F. Brigham, Phillip R. Daves

Publisher:

Cengage Learning