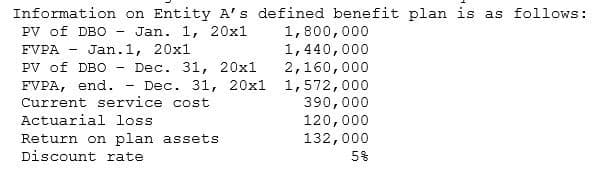

Information on Entity A's defined benefit plan is as follows: 1,800,000 1,440,000 2,160,000 PV of DBO - Jan. 1, 20x1 FVPA Jan.1, 20x1 PV of DBO Dec. 31, 20x1 FVPA, end. - Dec. 31, 20x1 1,572,000 Current service cost 390,000 120,000 Actuarial loss Return on plan assets Discount rate 132,000 5%

Q: An entity provided the following information during the current year: January 1 December 31 Fair…

A: SOLUTION- FAIR VALUE OF ASSET MEANS TO THE ACTUAL VALUE OF ASSET . IT IS NOT SAME AS MARKET VALUE ,…

Q: Information on an entity's plan assets is as follows: Fair value of plan assets, Jan 1 234.000 Fair…

A: Formula: Ending fair value of plan assets = Beginning fair value of assets + Contributions + Actual…

Q: A. At the beginning of current year, an entity provided the following information in connection with…

A: Projected benefit obligation at year-end=Projected benefit obligation+Current service cost+Past…

Q: Company provided the following information for the current year. •Current service cost - 500,000…

A: Employee Benefits includes various obligations of the employer towards the employee, which are in…

Q: Information on an entity's plan assets is as follows: Fair value of plan assets, Jan.1 360,000…

A: Particulars: Ending fair value of plan assets = Beginning value of plan assets + contributions to…

Q: Information on Entity A's defined benefit plan is as follows: PV of DBO - Jan. 1, 20x1 FVPA - Jan.1,…

A: Service cost attributable to the current and past periods and net interest on the net defined…

Q: Service cost $1,000,000 Actual return on plan assets Annual contribution to the plan Amortization of…

A: Pension plan:- A pension plan is defined as the retirement plan that requires an employer of…

Q: Charlton Company provided the following information concerning a defined benefit plan at the…

A: SOLUTION FORMULA- NET REMEASUREMENT GAIN = ACTUAL RETURN ON PLAN ASSETS -(FAIR VALUE OF PLAN ASSETS…

Q: YULETIDE Corporation reported the following data on January 1, 2021: Projected benefit obligation…

A: Defined benefit cost for the current year = Current service costs + Interest costs - Actual interest…

Q: Jeff Irvin Company provided the following information for the current year: Current service cost…

A: Total defined cost = Current service cost + Interest on PBO + Loss on settlement + past service…

Q: ONE Corporation provided the following information: December 31 January 1 P 3,500,000 P 3,900,000…

A: Actual return on plan assets for the current year = Ending Fair value of plan assets + benefit paid…

Q: Richelle Company provided the following information during the current year: 1-Jan 31-Dec…

A: Projected Benefit Obligation The purpose of using the projected benefit obligation which describes…

Q: Richelle Company provided the following information during the current year: January 1 December…

A: Prepaid benefit-cost reported on December 31 = Prepaid / Accrued Benefit Cost-Surplus - Effect on…

Q: Charlton Company provided the following information concerning a defined benefit plan at the…

A: A journal entry is a form of accounting entry that is used to report a business transaction in a…

Q: The following information on a defined benefit plan is provided: FVPA, beg 2,800,000 PVDBO, beg…

A: Defined Benefit Plan: A defined benefit plan is one in which the pension amount and retirement…

Q: Data regarding the defined benefit plan of XYZ Company follows: Present value of defined benefit…

A: Defined Benefit Obligation: A defined benefit plan is a sort of post-employment benefit that ensures…

Q: 14.Ivan Company provided the following information: January1 3,500,000 December 31 Fair value of…

A: Actual return on plan assets for the current year = Ending Fair value of plan assets + benefit paid…

Q: The following information on a defined benefit plan is provided: FVPA, beg…

A: Defined Benefit Plan Defined benefit plan which are provided to the employees of the entity after…

Q: Information on Entity A's defined benefit plan is as follows: PV of DBO - Jan. 1, 20x1 1,800,000…

A: Net defined benefit liability (asset) on year end = PV OF DBO DECEMBER 31 - FVPA DEC 31

Q: Shirley Company obtained the following information at the beginning of the current year prior to the…

A: Calculation Amount $ Current service cost 2,500,000 Add: Unrecognized actuarial…

Q: Jeff Irvin Company provided the following information for the current year: Current service cost…

A: Employee benefits are payments employers make to employees that are beyond the scope of wages.

Q: An entity provided the following information during the current year: January 1 December 31 Fair…

A: Interest cost = Beginning Projected benefit obligation x discount rate = 4,500,000*10% = 450,000

Q: Information on Entity A’s defined benefit plan is as follows: PV of DBO – Jan. 1, 20x1 2,000,000…

A: Assets Remeauerments gain of loss is recognized to other comprehensive income. Current service cost,…

Q: The actuarial valuation report of an entity shows the following Present value of defined benefit…

A: Amount of Defined Benefit obligation at the beginning of the year ::2,80,000.. Service cost::50,000.…

Q: urrent service cost 500,000 terest on projected benefit obligation 600,000 sterest income on plan…

A: Given: An entity provided the following information for the current year:Current service cost…

Q: The following information on a defined benefit plan is provided: FVPA, beg beg 2,200,000 Current…

A: Defined Benefit Plan Employees of the entity are given with a defined benefit plan after they have…

Q: Jeff Irvin Company provided the following information for the current year: Current service cost…

A: Employee benefit expenses are those expenses which are related with providing benefits to the…

Q: Information on Entity A's defined benefit plan is as follows: 1,800,000 1,440,000 2,160,000 PV of…

A: Service cost attributable to the current and past periods and Net interest on the net defined…

Q: nformation on Entity A's defined benefit plan is as follows: 1,800,000 1,440,000 2,160,000 PV of DBO…

A: Net defined benefit liability (asset) = pv of DBO at December 31 - Fair value of plan assets (…

Q: A Company provided the following information for the current year: Current service cost 500,000…

A: PBO is an integral part of Employer management structure and it stands for "Projected Benefit…

Q: The following information on a de fined benefit plan is provided: FVPA, beg 2,800,000 PVOBO, beg…

A: Employees of the entity are given with a defined benefit plan after they have retired from service.…

Q: The following information on a defined benefit plan is provided: FVPA, beg 4,000,000 PVDBO, beg…

A: OCI is the other comprehensive incomes, which is calculated in financial accounting, It is for the…

Q: ONE Corporation provided the following information: January 1 December 31 P 3,500,000 P 3,900,000…

A: Actual return on plan assets for the current year = Ending Fair value of plan assets + benefit paid…

Q: You are the General Manager of Entity A. You have received the actuarial report for your company’s…

A: Formula: Increase net defined benefit liability=Net defined benefit liability, end.-Net defined…

Q: The following information is made available in relation to the defined benefit plan of Marcos…

A: RECONCILITION OF PLAN ASSETS PARTICULARS PLAN ASSETS FOR YEAR 2022 FAIR VALUE AS ON…

Q: E. Charlton Company provided the following information concerning a defined benefit plan at the…

A: Interest cost = Beginning Projected benefit obligation x discount rate = 5500000*6% = 330,000

Q: Company provided the following information for the current year: Current service cost 500,000…

A: The benefit-cost ratio (BCR) is a profitability indicator used in cost-benefit analysis to determine…

Q: nalyzing Changes in Plan Assets and PBO The following information pertains to a company’s defined…

A: A Projected Benefit Obligation (PBO) is one type of measurement about amount that a company will…

Q: At the beginning of current year, an entity provided the following information in connection with a…

A: Interest cost = Beginning Projected benefit obligation x discount rate = 13000000*10% = 1,300,000

Q: Information on Balinquit Company’s defined benefit plan is shown below: Fair value of plan asset,…

A: PLAN assets are assets or investments held by a long-term employee benefit fund for the purpose of…

Q: Richelle Company provided the following information during the current year: January 1 December…

A: Net Remeasurement Loss = Actuarial Loss on Liability + Loss on Return + Changes in Asset Ceiling

Q: Charlton Company provided the following information concerning a defined benefit plan at the…

A: Fair Value Plan Asset (FVPA) as of December 31=Fair value of plan assets+Projected benefit…

Q: Bounty Company revealed the following information for the current year: Fair Value of plan assets -…

A: Actual return = expected return + actuarial gain

Q: CHOOSE THE LETTER OF THE CORRECT ANSWER What is the employee benefit expense for the current year?…

A: Acuturial gan or loss refers to an increase or decrease in the projections used to value a…

Q: Information on Complicated Company's defined benefit plan is as follows: Fair value of plan assets,…

A: Given that, On January 1, Opening Fair value of plan assets = P480000 Return on plan assets (Actual…

Q: Richelle Company provided the following information during the current year: January 1 December…

A: Employee Benefit Expense = Current Service Cost + Net Interest on Defined Benefit Liability

Q: . An entity provided the following information during the current year: January 1 December 31 Fair…

A: Pension Plan These are the plan where benefits are paid to employees after they retire

Q: An entity provided the following information during the current year: January 1 December 31 Fair…

A: Cost Benefit - It is systematic process in the business to analyze the which decisions to make and…

How much is the total defined benefit cost for 20x1?

Step by step

Solved in 2 steps

- You are the General Manager of Entity A. You have received the actuarial report for your company’s defined benefit plan. The report shows the following information: PV of DBO – Jan. 1, 20x1 1,500,000 FVPA – Jan. 1, 20x1 1,200,000 PV of DBO – Dec. 31, 20x1 1,800,000 FVPA, end. – Dec. 31, 20x1 1,310,000 Actuarial gain 100,000 Return on plan assets 110,000 Discount rate 5% When reporting on your company’s year-end highlights of financial summary, which of the following will you report to the Board of Directors (the ‘big bosses’)?E. Charlton Company provided the following information concerning a defined benefit plan at the beginning ofcurrent year prior to the adoption of revised PAS 19:Debit CreditFair value of plan assets 4,750,000Unamortized past service cost 1,250,000Projected benefit obligation 5,500,000Unrecognized actuarial gain 850,000The transactions for the current year relating to the defined benefit plan are as follows:Current service cost 925,000Discount rate 6%Actual return on plan assets 485,000Contribution to the plan 1,350,000Benefits paid to retirees 995,000Increase in projected benefit obligation due to changes in actuarial assumptions 150,000Effective in the current year, the entity has applied the provisions of revised PAS 19 in relation to the definedbenefit plan.REQUIRED: 17. Compute the remeasurement related to the defined benefit plan.E. Charlton Company provided the following information concerning a defined benefit plan at the beginning ofcurrent year prior to the adoption of revised PAS 19:Debit CreditFair value of plan assets 4,750,000Unamortized past service cost 1,250,000Projected benefit obligation 5,500,000Unrecognized actuarial gain 850,000The transactions for the current year relating to the defined benefit plan are as follows:Current service cost 925,000Discount rate 6%Actual return on plan assets 485,000Contribution to the plan 1,350,000Benefits paid to retirees 995,000Increase in projected benefit obligation due to changes in actuarial assumptions 150,000Effective in the current year, the entity has applied the provisions of revised PAS 19 in relation to the definedbenefit plan.REQUIRED: 19. Compute for the Fair Value Plan Asset (FVPA) as of December 31.

- E. Charlton Company provided the following information concerning a defined benefit plan at the beginning ofcurrent year prior to the adoption of revised PAS 19:Debit CreditFair value of plan assets 4,750,000Unamortized past service cost 1,250,000Projected benefit obligation 5,500,000Unrecognized actuarial gain 850,000The transactions for the current year relating to the defined benefit plan are as follows:Current service cost 925,000Discount rate 6%Actual return on plan assets 485,000Contribution to the plan 1,350,000Benefits paid to retirees 995,000Increase in projected benefit obligation due to changes in actuarial assumptions 150,000Effective in the current year, the entity has applied the provisions of revised PAS 19 in relation to the definedbenefit plan. Compute the remeasurement related to the defined benefit plan.E. Charlton Company provided the following information concerning a defined benefit plan at the beginning ofcurrent year prior to the adoption of revised PAS 19:Debit CreditFair value of plan assets 4,750,000Unamortized past service cost 1,250,000Projected benefit obligation 5,500,000Unrecognized actuarial gain 850,000The transactions for the current year relating to the defined benefit plan are as follows:Current service cost 925,000Discount rate 6%Actual return on plan assets 485,000Contribution to the plan 1,350,000Benefits paid to retirees 995,000Increase in projected benefit obligation due to changes in actuarial assumptions 150,000Effective in the current year, the entity has applied the provisions of revised PAS 19 in relation to the definedbenefit plan.REQUIRED: 16. Determine the employee benefit expense for the current year.Charlton Company provided the following information concerning a defined benefit plan at the beginning ofcurrent year prior to the adoption of revised PAS 19:Debit CreditFair value of plan assets 4,750,000Unamortized past service cost 1,250,000Projected benefit obligation 5,500,000Unrecognized actuarial gain 850,000The transactions for the current year relating to the defined benefit plan are as follows:Current service cost 925,000Discount rate 6%Actual return on plan assets 485,000Contribution to the plan 1,350,000Benefits paid to retirees 995,000Increase in projected benefit obligation due to changes in actuarial assumptions 150,000Effective in the current year, the entity has applied the provisions of revised PAS 19 in relation to the definedbenefit plan. 18. Prepare journal entry to record the employee benefit expense.19. Compute for the Fair Value Plan Asset (FVPA) as of December 31.20. Compute for the projected benefit obligation on December 31.

- Charlton Company provided the following information concerning a defined benefit plan at the beginning ofcurrent year prior to the adoption of revised PAS 19:Debit CreditFair value of plan assets 4,750,000Unamortized past service cost 1,250,000Projected benefit obligation 5,500,000Unrecognized actuarial gain 850,000The transactions for the current year relating to the defined benefit plan are as follows:Current service cost 925,000Discount rate 6%Actual return on plan assets 485,000Contribution to the plan 1,350,000Benefits paid to retirees 995,000Increase in projected benefit obligation due to changes in actuarial assumptions 150,000Effective in the current year, the entity has applied the provisions of revised PAS 19 in relation to the definedbenefit plan.REQUIRED: Prepare journal entry to recognize the transitional effect of adopting revised PAS 19.Charlton Company provided the following information concerning a defined benefit plan at the beginning ofcurrent year prior to the adoption of revised PAS 19:Debit CreditFair value of plan assets 4,750,000Unamortized past service cost 1,250,000Projected benefit obligation 5,500,000Unrecognized actuarial gain 850,000The transactions for the current year relating to the defined benefit plan are as follows:Current service cost 925,000Discount rate 6%Actual return on plan assets 485,000Contribution to the plan 1,350,000Benefits paid to retirees 995,000Increase in projected benefit obligation due to changes in actuarial assumptions 150,000Effective in the current year, the entity has applied the provisions of revised PAS 19 in relation to the definedbenefit plan.REQUIRED: Prepare journal entry to record the employee benefit expense.Information about the defined benefit plan of the company is shown belowFair value on plan asset, January 1, 2021 3,000,000Contribution to the fund 1,500,000Return on plan assets 160,000Defined benefit liability. December 31, 2021 410,000Defined benefit obligation, December 31, 2021 4,550,000What is the balance of the fair value on plan asset as of December 31, 2021?

- Fair value of plan assets 4,750,000Unamortized past service cost 1,250,000Projected benefit obligation 5,500,000Unrecognized actuarial gain 850,000The transactions for the current year relating to the defined benefit plan are as follows:Current service cost 925,000Discount rate 6%Actual return on plan assets 485,000Contribution to the plan 1,350,000Benefits paid to retirees 995,000Increase in projected benefit obligation due to changes in actuarial assumptions 150,000Effective in the current year, the entity has applied the provisions of revised PAS 19 in relation to the definedbenefit plan.REQUIRED:15. Prepare journal entry to recognize the transitional effect of adopting revised PAS 19.16. Determine the employee benefit expense for the current year.17. Compute the remeasurement related to the defined benefit plan.18. Prepare journal entry to record the employee benefit expense.19. Compute for the Fair Value Plan Asset (FVPA) as of December 31.20. Compute for the projected benefit…#14Stefan company provided the following information in relation to a defined benefit plan for thecurrent year:January 1 December 31Fair value of plan assets 1,300,000 1,500,000Projected benefit obligation 1,000,000 1,050,000Prepaid/accrued benefit cost-surplus 300,000 450,000Asset ceiling 100,000 150,000Effect of asset ceiling 200,000 300,000Current service cost 50,000Contribution to the plan 175,000Benefits paid 75,000Discount rate 10%What is the net remeasurement loss for the current year? 85,000 pls provide solution for this answerA. At the beginning of current year, an entity provided the following information in connection with adefined benefit plan: Fair value of plan assets 10,000,000Projected benefit obligation (13,000,000)Prepaid /accrued benefit cost (3,000,000) The entity revealed the following transactions affecting the plan for the current year: Current service cost 2,500,000Past service cost - remaining vesting period of covered employees is 5 years 1,200,000Contribution to the plan 3,500,000Benefits paid to retirees 3,000,000Actual return on plan assets 1,500,000 Decrease in projected benefit obligation due to change in actuarial assumptions 400,000Discount rate 10%Expected return on plan assets 12% Compute the projected benefit obligation at year-end What amount should be reported as accrued or prepaid benefit cost at year-end