It sputtered and squeaked and with a small hesitation followed by an abbreviated lunge, it was finally over: Ol' Reliable, the car Jamie Lee had driven since she first earned her driver's license at the age of 17, completed its last mile. Thirteen years and 140,000 miles later, it was time for a new vehicle. After skimming the Sunday newspaper and browsing the online advertisements, Jamie Lee was ready to visit car dealers to see what vehicles would interest her. She was unsure if she would purchase a car brand new, used, finance with a down payment, or lease. "No money down and only $231 a month," Jamie Lee read, "with approved credit." Sounded like an offer she would be interested in. Jamie Lee knew she had a good credit rating as she made sure she paid all of her bills on time each month, and kept a close eye on her credit score ever since she was the victim of identity theft several years ago. The more she thought about the brand new car, the more excited she became. That new car fit her personality perfectly. As Jamie Lee inquired about the advertised vehicle with the new car salesperson, her excitement quickly turned to dismay. The automobile advertised was available for $231 a month with no money down, based on approved credit, but Jamie Lee unexpectedly found that there were further qualifications in order to get the advertised price. The salesman explained that the information in the fine print of the newspaper advertisement stated that the price was based on all of the following criteria: being active in the military, a college graduate within the last three months, a current lessee of the automobile company, and having a top tier credit score, which he noted was above 800. If Jamie Lee did not meet all of the qualifications, she would not receive the price advertised in the promotion. But, he noted, he could get her in that vehicle, but it would cost her an additional $115 per month. Two hundred and seventy-five dollars was the maximum Jamie budgeted for a monthly payment. This vehicle was outside of her financial plan. Jamie Lee had to start over from scratch. She decided that she must fully research the vehicle purchase process before browsing at another dealership. She felt she was getting caught up in the moment and vowed to do her research before speaking with another salesperson. Complete the table below to compare the costs of buying and leasing a vehicle. Each answer must have a value for the assignment to be complete. Enter "O" for any unused categories. See below for the necessary data. End of lease charges?

It sputtered and squeaked and with a small hesitation followed by an abbreviated lunge, it was finally over: Ol' Reliable, the car Jamie Lee had driven since she first earned her driver's license at the age of 17, completed its last mile. Thirteen years and 140,000 miles later, it was time for a new vehicle. After skimming the Sunday newspaper and browsing the online advertisements, Jamie Lee was ready to visit car dealers to see what vehicles would interest her. She was unsure if she would purchase a car brand new, used, finance with a down payment, or lease. "No money down and only $231 a month," Jamie Lee read, "with approved credit." Sounded like an offer she would be interested in. Jamie Lee knew she had a good credit rating as she made sure she paid all of her bills on time each month, and kept a close eye on her credit score ever since she was the victim of identity theft several years ago. The more she thought about the brand new car, the more excited she became. That new car fit her personality perfectly. As Jamie Lee inquired about the advertised vehicle with the new car salesperson, her excitement quickly turned to dismay. The automobile advertised was available for $231 a month with no money down, based on approved credit, but Jamie Lee unexpectedly found that there were further qualifications in order to get the advertised price. The salesman explained that the information in the fine print of the newspaper advertisement stated that the price was based on all of the following criteria: being active in the military, a college graduate within the last three months, a current lessee of the automobile company, and having a top tier credit score, which he noted was above 800. If Jamie Lee did not meet all of the qualifications, she would not receive the price advertised in the promotion. But, he noted, he could get her in that vehicle, but it would cost her an additional $115 per month. Two hundred and seventy-five dollars was the maximum Jamie budgeted for a monthly payment. This vehicle was outside of her financial plan. Jamie Lee had to start over from scratch. She decided that she must fully research the vehicle purchase process before browsing at another dealership. She felt she was getting caught up in the moment and vowed to do her research before speaking with another salesperson. Complete the table below to compare the costs of buying and leasing a vehicle. Each answer must have a value for the assignment to be complete. Enter "O" for any unused categories. See below for the necessary data. End of lease charges?

Cornerstones of Financial Accounting

4th Edition

ISBN:9781337690881

Author:Jay Rich, Jeff Jones

Publisher:Jay Rich, Jeff Jones

Chapter5: Sales And Receivables

Section: Chapter Questions

Problem 35CE: Notes Receivable Link Communications programs voicemail systems for businesses. For a recent...

Related questions

Question

It sputtered and squeaked and with a small hesitation followed by an abbreviated lunge, it was finally over: Ol' Reliable, the car Jamie Lee had driven since she first earned her driver's license at the age of 17, completed its last mile. Thirteen years and 140,000 miles later, it was time for a new vehicle.

After skimming the Sunday newspaper and browsing the online advertisements, Jamie Lee was ready to visit car dealers to see what vehicles would interest her. She was unsure if she would purchase a car brand new, used, finance with a down payment, or lease. "No money down and only $231 a month," Jamie Lee read, "with approved credit." Sounded like an offer she would be interested in. Jamie Lee knew she had a good credit rating as she made sure she paid all of her bills on time each month, and kept a close eye on her credit score ever since she was the victim of identity theft several years ago. The more she thought about the brand new car, the more excited she became. That new car fit her personality perfectly.

As Jamie Lee inquired about the advertised vehicle with the new car salesperson, her excitement quickly turned to dismay. The automobile advertised was available for $231 a month with no money down, based on approved credit, but Jamie Lee unexpectedly found that there were further qualifications in order to get the advertised price. The salesman explained that the information in the fine print of the newspaper advertisement stated that the price was based on all of the following criteria: being active in the military, a college graduate within the last three months, a current lessee of the automobile company, and having a top tier credit score, which he noted was above 800. If Jamie Lee did not meet all of the qualifications, she would not receive the price advertised in the promotion.

But, he noted, he could get her in that vehicle, but it would cost her an additional $115 per month. Two hundred and seventy-five dollars was the maximum Jamie budgeted for a monthly payment. This vehicle was outside of her financial plan.

Jamie Lee had to start over from scratch. She decided that she must fully research the vehicle purchase process before browsing at another dealership. She felt she was getting caught up in the moment and vowed to do her research before speaking with another salesperson.

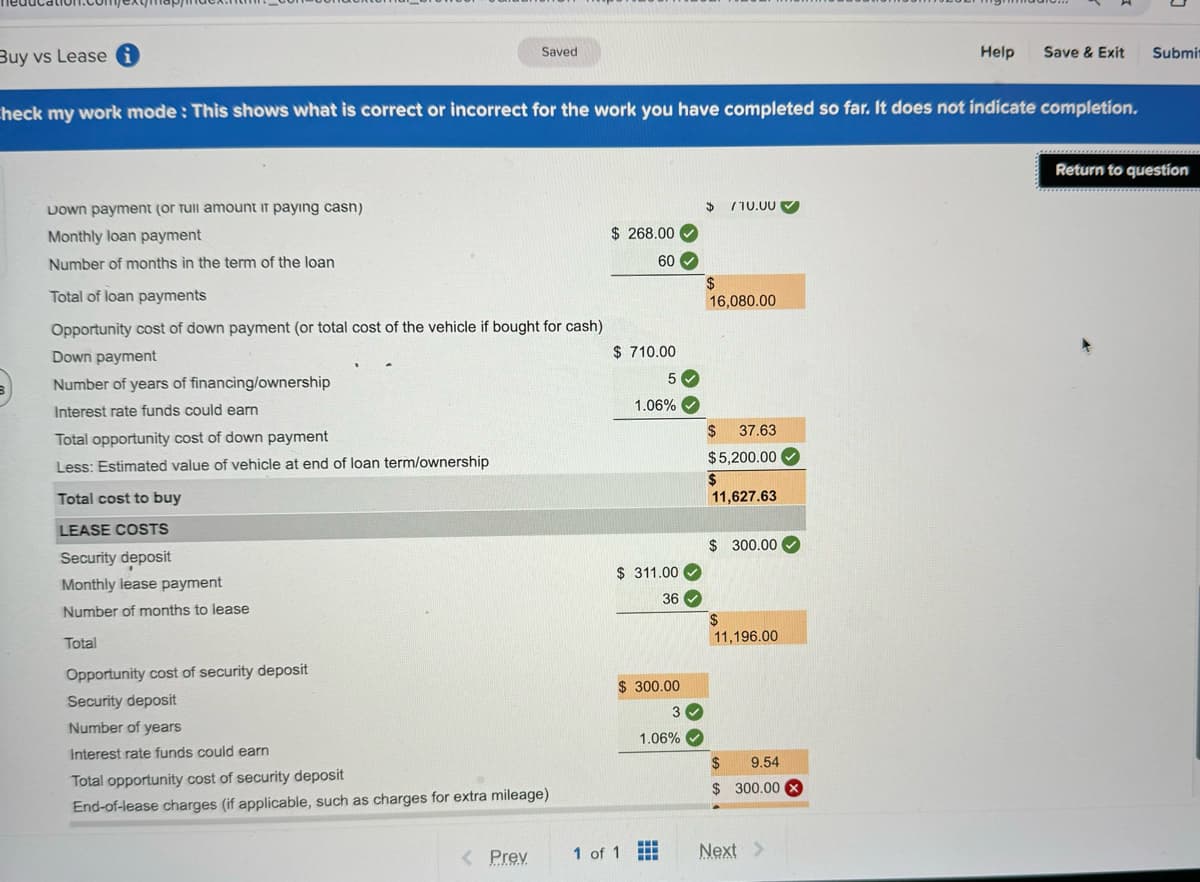

Complete the table below to compare the costs of buying and leasing a vehicle. Each answer must have a value for the assignment to be complete. Enter "O" for any unused categories. See below for the necessary data.

End of lease charges?

Transcribed Image Text:Buy vs Lease i

Saved

Help

Save & Exit

Submit

Check my work mode: This shows what is correct or incorrect for the work you have completed so far. It does not indicate completion.

Down payment (or Tull amount if paying cash)

Monthly loan payment

Number of months in the term of the loan

Total of loan payments

Opportunity cost of down payment (or total cost of the vehicle if bought for cash)

Down payment

B

Number of years of financing/ownership

Interest rate funds could earn

Total opportunity cost of down payment

Less: Estimated value of vehicle at end of loan term/ownership

Total cost to buy

LEASE COSTS

Security deposit

Monthly lease payment

Number of months to lease

Total

Opportunity cost of security deposit

Security deposit

Number of years

Interest rate funds could earn

Total opportunity cost of security deposit

End-of-lease charges (if applicable, such as charges for extra mileage)

$

710.00

$ 268.00

60

$

16,080.00

$ 710.00

5

1.06%

$ 37.63

$5,200.00

$

11,627.63

$ 300.00

$ 311.00

36

$

11,196.00

$ 300.00

3

1.06%

$

9.54

$ 300.00 X

< Prev

1 of 1

Next >

Return to question

![Research for Nissan Versa Sedan 2016

*4 speed automatic

"Air conditioning

*Bluetooth® hands-free phone system

Credit Purchase

Total price of car

Down payment (-)

Amount financed

Length of time

Interest rate

Monthly payment

$ 15,875.00

$ 710.00

$.15,165.00

60 MONTHS

$ 268.00

Total price of car

Acquisition fee (+)

Adjusted capitalized cost

Length of time

3.66%

Security deposit

Monthly payment

Savings account interest earned rate = 1.06%

Lease

$ 15,875.00

$655.00

$ 16,530.00

36 MONTHS

$ 300.00

Estimated value of car at end of loan - $5,200

www.nissanusa.com

• Jamie Lee intends to use the car for at least five years before selling or trading it for a small SUV.

Note that there is a $400 rebate offer for cash purchase.

•

The tax is calculated using the Total cost of vehicle.

Total cost of vehicle

Tax

Tags and registration (delivery/set up fees)

$ 15,875.00

[3%]

$ 79.00

Answer is complete but not entirely correct.

2017 Nissan Versa Sedan

PURCHASE COSTS

Total vehicle costs

Down payment (or full amount if paying cash)

$

16,351.25

$ 710.00

<Prev

1 of 1

Next >

$ 311.00

Return to question](/v2/_next/image?url=https%3A%2F%2Fcontent.bartleby.com%2Fqna-images%2Fquestion%2F913dd8a1-24ac-4d15-9ae0-4e3b8e5cde99%2F0cf72d9b-50c6-4a49-b6bb-81601c7fbeab%2Fm0jd9n_processed.jpeg&w=3840&q=75)

Transcribed Image Text:Research for Nissan Versa Sedan 2016

*4 speed automatic

"Air conditioning

*Bluetooth® hands-free phone system

Credit Purchase

Total price of car

Down payment (-)

Amount financed

Length of time

Interest rate

Monthly payment

$ 15,875.00

$ 710.00

$.15,165.00

60 MONTHS

$ 268.00

Total price of car

Acquisition fee (+)

Adjusted capitalized cost

Length of time

3.66%

Security deposit

Monthly payment

Savings account interest earned rate = 1.06%

Lease

$ 15,875.00

$655.00

$ 16,530.00

36 MONTHS

$ 300.00

Estimated value of car at end of loan - $5,200

www.nissanusa.com

• Jamie Lee intends to use the car for at least five years before selling or trading it for a small SUV.

Note that there is a $400 rebate offer for cash purchase.

•

The tax is calculated using the Total cost of vehicle.

Total cost of vehicle

Tax

Tags and registration (delivery/set up fees)

$ 15,875.00

[3%]

$ 79.00

Answer is complete but not entirely correct.

2017 Nissan Versa Sedan

PURCHASE COSTS

Total vehicle costs

Down payment (or full amount if paying cash)

$

16,351.25

$ 710.00

<Prev

1 of 1

Next >

$ 311.00

Return to question

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution!

Trending now

This is a popular solution!

Step by step

Solved in 3 steps

Recommended textbooks for you

Cornerstones of Financial Accounting

Accounting

ISBN:

9781337690881

Author:

Jay Rich, Jeff Jones

Publisher:

Cengage Learning

Intermediate Accounting: Reporting And Analysis

Accounting

ISBN:

9781337788281

Author:

James M. Wahlen, Jefferson P. Jones, Donald Pagach

Publisher:

Cengage Learning

Financial Accounting: The Impact on Decision Make…

Accounting

ISBN:

9781305654174

Author:

Gary A. Porter, Curtis L. Norton

Publisher:

Cengage Learning

Cornerstones of Financial Accounting

Accounting

ISBN:

9781337690881

Author:

Jay Rich, Jeff Jones

Publisher:

Cengage Learning

Intermediate Accounting: Reporting And Analysis

Accounting

ISBN:

9781337788281

Author:

James M. Wahlen, Jefferson P. Jones, Donald Pagach

Publisher:

Cengage Learning

Financial Accounting: The Impact on Decision Make…

Accounting

ISBN:

9781305654174

Author:

Gary A. Porter, Curtis L. Norton

Publisher:

Cengage Learning