Label the following for this diagram a. Name of options payoff b. identify whether positive or negative premium identify breakeven point d. What is the profit or loss when stock price is $60 at maturity . Suppose you have this options position, should you exercise your right (if any) assuming that the stock price is S60 at maturity Option Payoffs and Profits Long put $40 $20

Label the following for this diagram a. Name of options payoff b. identify whether positive or negative premium identify breakeven point d. What is the profit or loss when stock price is $60 at maturity . Suppose you have this options position, should you exercise your right (if any) assuming that the stock price is S60 at maturity Option Payoffs and Profits Long put $40 $20

Intermediate Financial Management (MindTap Course List)

13th Edition

ISBN:9781337395083

Author:Eugene F. Brigham, Phillip R. Daves

Publisher:Eugene F. Brigham, Phillip R. Daves

Chapter5: Financial Options

Section: Chapter Questions

Problem 3Q

Related questions

Question

answer question d and e only.

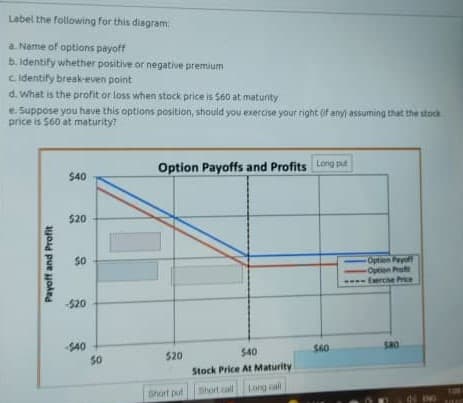

Transcribed Image Text:Label the following for this diagram

a. Name of options payoff

b. identify whether positive or negative premium

cidentify break-even point

d. What is the profit or loss when stock price is S60 at maturity

e. Suppose you have this options position, should you exercise your right if any assuming that the stock

price is S60 at maturity

Option Payoffs and Profits Long pid

$40

$20

Option Peyoff

Opton Pro

Eercie r

520

S40

$60

SHO

$40

520

50

Stock Price At Maturity

Dhort pul

Short all

Long al

94

Payoff and Profit

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

Step by step

Solved in 2 steps

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, finance and related others by exploring similar questions and additional content below.Recommended textbooks for you

Intermediate Financial Management (MindTap Course…

Finance

ISBN:

9781337395083

Author:

Eugene F. Brigham, Phillip R. Daves

Publisher:

Cengage Learning

Intermediate Financial Management (MindTap Course…

Finance

ISBN:

9781337395083

Author:

Eugene F. Brigham, Phillip R. Daves

Publisher:

Cengage Learning