Micro Forecasts Beta Asset Expected Return (%) Residual Standard Deviation (%) Stock A 20 1.00 60 Stock B 18 2.50 40 Macro Forecasts Expected Return (%) Asset Standard Deviation (%) T-bills 5 0 Passive Equity Portfolio (m) 12 25 a. Calculate expected excess returns, alpha values, and residual variances for these stocks. Instruction: Enter your answer as a percentage (rounded to two decimal places) for expected excess returns and alpha values. Expected excess return on stock A Expected excess return on stock B Alpha of stock A Alpha of stock B 15 % 13 % 8% -4.5% Instruction: Enter your answer as a decimal number rounded to two decimal places for residual variances. Residual variance of stock A 0.36 Residual variance of stock B 16 Instruction: for part b, enter your response as a decimal number rounded to four decimal places. b. Suppose that the portfolio manager follows the Treynor-Black model, and constructs an active portfolio (p) that consists of the above two stocks. The alpha of the active portfolio (p) is -18%, and its residual standard deviation is 150%. What is the Sharpe ratio for the optimal portfolio (consisting of the passive equity portfolio and the active portfolio (p)? What's the M2 of the optimal portfolio?

Micro Forecasts Beta Asset Expected Return (%) Residual Standard Deviation (%) Stock A 20 1.00 60 Stock B 18 2.50 40 Macro Forecasts Expected Return (%) Asset Standard Deviation (%) T-bills 5 0 Passive Equity Portfolio (m) 12 25 a. Calculate expected excess returns, alpha values, and residual variances for these stocks. Instruction: Enter your answer as a percentage (rounded to two decimal places) for expected excess returns and alpha values. Expected excess return on stock A Expected excess return on stock B Alpha of stock A Alpha of stock B 15 % 13 % 8% -4.5% Instruction: Enter your answer as a decimal number rounded to two decimal places for residual variances. Residual variance of stock A 0.36 Residual variance of stock B 16 Instruction: for part b, enter your response as a decimal number rounded to four decimal places. b. Suppose that the portfolio manager follows the Treynor-Black model, and constructs an active portfolio (p) that consists of the above two stocks. The alpha of the active portfolio (p) is -18%, and its residual standard deviation is 150%. What is the Sharpe ratio for the optimal portfolio (consisting of the passive equity portfolio and the active portfolio (p)? What's the M2 of the optimal portfolio?

Chapter8: Analysis Of Risk And Return

Section: Chapter Questions

Problem 12P

Related questions

Question

Need help with B part

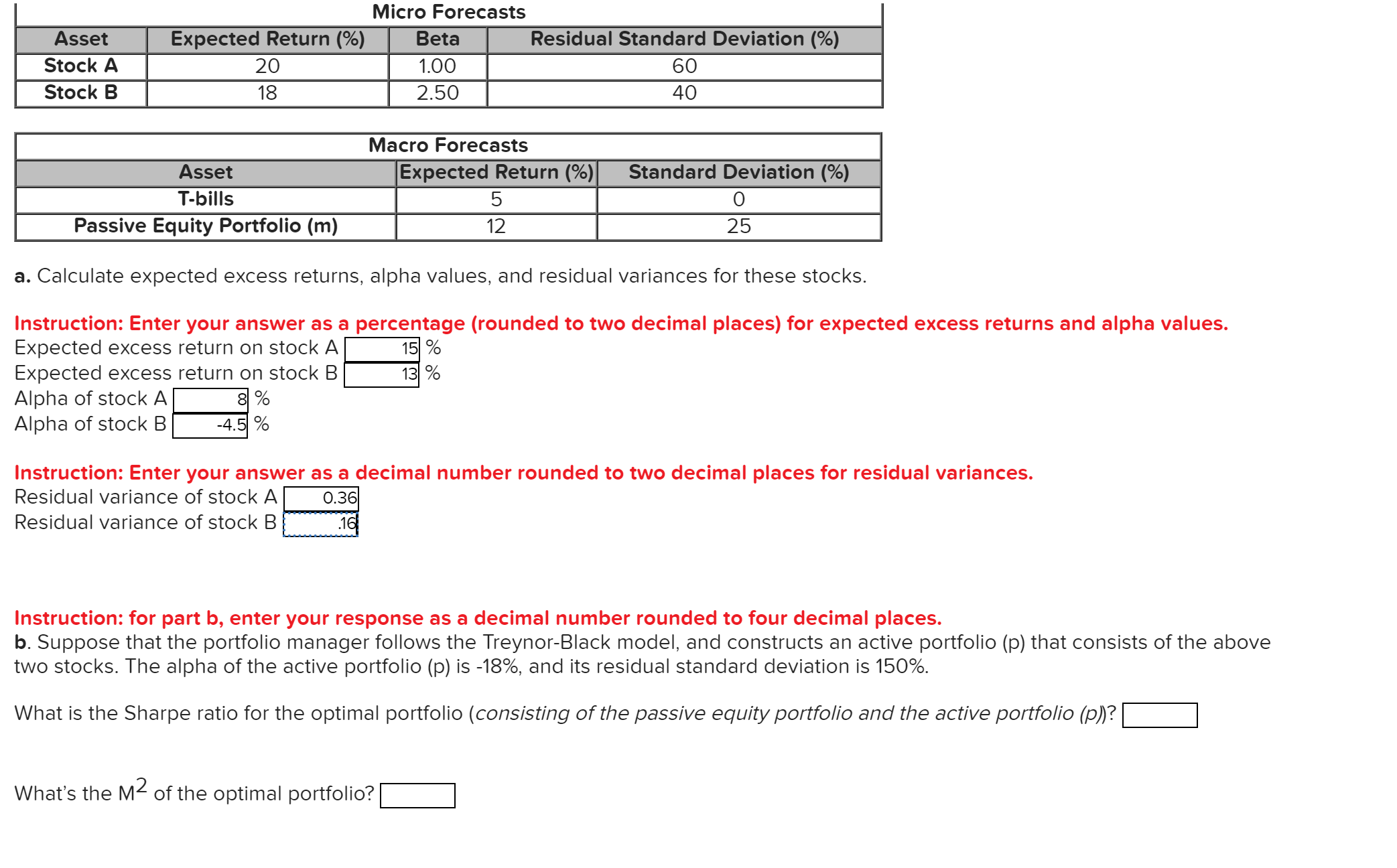

Transcribed Image Text:Micro Forecasts

Beta

Asset

Expected Return (%)

Residual Standard Deviation (%)

Stock A

20

1.00

60

Stock B

18

2.50

40

Macro Forecasts

Expected Return (%)

Asset

Standard Deviation (%)

T-bills

5

0

Passive Equity Portfolio (m)

12

25

a. Calculate expected excess returns, alpha values, and residual variances for these stocks.

Instruction: Enter your answer as a percentage (rounded to two decimal places) for expected excess returns and alpha values.

Expected excess return on stock A

Expected excess return on stock B

Alpha of stock A

Alpha of stock B

15 %

13 %

8%

-4.5%

Instruction: Enter your answer as a decimal number rounded to two decimal places for residual variances.

Residual variance of stock A

0.36

Residual variance of stock B

16

Instruction: for part b, enter your response as a decimal number rounded to four decimal places.

b. Suppose that the portfolio manager follows the Treynor-Black model, and constructs an active portfolio (p) that consists of the above

two stocks. The alpha of the active portfolio (p) is -18%, and its residual standard deviation is 150%.

What is the Sharpe ratio for the optimal portfolio (consisting of the passive equity portfolio and the active portfolio (p)?

What's the M2 of the optimal portfolio?

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution!

Trending now

This is a popular solution!

Step by step

Solved in 2 steps with 2 images

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, finance and related others by exploring similar questions and additional content below.Recommended textbooks for you

EBK CONTEMPORARY FINANCIAL MANAGEMENT

Finance

ISBN:

9781337514835

Author:

MOYER

Publisher:

CENGAGE LEARNING - CONSIGNMENT

Intermediate Financial Management (MindTap Course…

Finance

ISBN:

9781337395083

Author:

Eugene F. Brigham, Phillip R. Daves

Publisher:

Cengage Learning

EBK CONTEMPORARY FINANCIAL MANAGEMENT

Finance

ISBN:

9781337514835

Author:

MOYER

Publisher:

CENGAGE LEARNING - CONSIGNMENT

Intermediate Financial Management (MindTap Course…

Finance

ISBN:

9781337395083

Author:

Eugene F. Brigham, Phillip R. Daves

Publisher:

Cengage Learning