On January 1, BB Acquired 60 percent of the outstanding voting stock of SS for P260,000 cash consideration. The remaining 40 percent of SS had an acquisition date fair value of P65,000. On January 1, SS possessed equipment (5-year life) that was undervalued on its books P25,000. SS also had developed several secret formulas that BB assessed at P50,000. Theses formulas, although not recorded on SS's financial records, were estimated to have a 20-year future life. BB also determined that the inventory of SS is overvalued by P10,000. 80% of these inventories remain unsold by the end of the year. As of December 31, the financial statements appeared as follows: BB P (300, 000) P (200, 000) Revenues (from sales and dividends) Cost of goods sold Expenses 140, 000 20, 000 P (140, 000) P (110, 000) 80, 000 10, 000 Net Income Retained earnings 1/1 P (300, 000) P (150, 000) (140, 000) -0- Net Income (110, 000) 10,000 Dividends paid Retained earnings 12/31 P (440, 000) P (250, 000) Cash and Receivables P 210, 000 P90, 000 110, 000 -0- 150, 000 260, 000 440, 000 P 1,060, 000 Inventory Investment in SS Equipment (net) Total Assets 300, 000 P500, 000 P (420, 000) P (150, 000) (200, 000) (440, 000) P (1,060,000) P (500, 000) Liabilities Common stock (100, 000) (250, 000) Retained earnings 12/31 Total Liabilities and Equities Determine the consolidated assets as of December 31.

On January 1, BB Acquired 60 percent of the outstanding voting stock of SS for P260,000 cash consideration. The remaining 40 percent of SS had an acquisition date fair value of P65,000. On January 1, SS possessed equipment (5-year life) that was undervalued on its books P25,000. SS also had developed several secret formulas that BB assessed at P50,000. Theses formulas, although not recorded on SS's financial records, were estimated to have a 20-year future life. BB also determined that the inventory of SS is overvalued by P10,000. 80% of these inventories remain unsold by the end of the year. As of December 31, the financial statements appeared as follows: BB P (300, 000) P (200, 000) Revenues (from sales and dividends) Cost of goods sold Expenses 140, 000 20, 000 P (140, 000) P (110, 000) 80, 000 10, 000 Net Income Retained earnings 1/1 P (300, 000) P (150, 000) (140, 000) -0- Net Income (110, 000) 10,000 Dividends paid Retained earnings 12/31 P (440, 000) P (250, 000) Cash and Receivables P 210, 000 P90, 000 110, 000 -0- 150, 000 260, 000 440, 000 P 1,060, 000 Inventory Investment in SS Equipment (net) Total Assets 300, 000 P500, 000 P (420, 000) P (150, 000) (200, 000) (440, 000) P (1,060,000) P (500, 000) Liabilities Common stock (100, 000) (250, 000) Retained earnings 12/31 Total Liabilities and Equities Determine the consolidated assets as of December 31.

Intermediate Accounting: Reporting And Analysis

3rd Edition

ISBN:9781337788281

Author:James M. Wahlen, Jefferson P. Jones, Donald Pagach

Publisher:James M. Wahlen, Jefferson P. Jones, Donald Pagach

Chapter13: Investments And Long-term Receivables

Section: Chapter Questions

Problem 8MC

Related questions

Question

100%

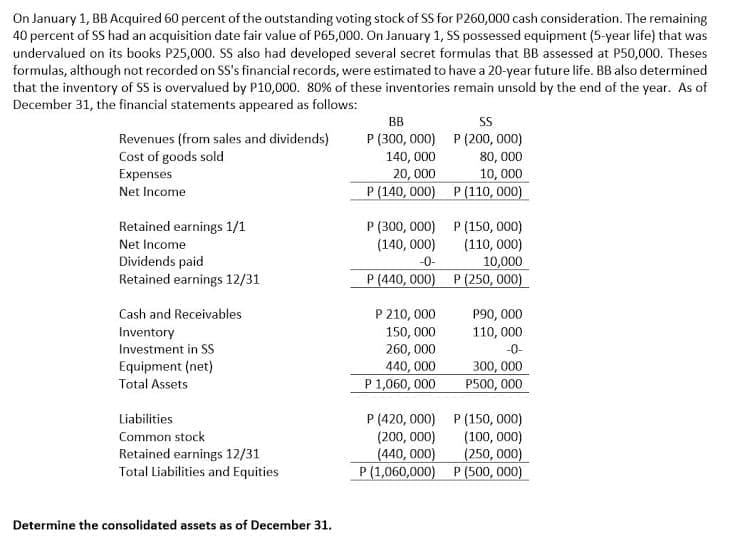

Transcribed Image Text:On January 1, BB Acquired 60 percent of the outstanding voting stock of SS for P260,000 cash consideration. The remaining

40 percent of SS had an acquisition date fair value of P65,000. On January 1, SS possessed equipment (5-year life) that was

undervalued on its books P25,000. SS also had developed several secret formulas that BB assessed at P50,000. Theses

formulas, although not recorded on SS's financial records, were estimated to have a 20-year future life. BB also determined

that the inventory of SS is overvalued by P10,000. 80% of these inventories remain unsold by the end of the year. As of

December 31, the financial statements appeared as follows:

BB

Revenues (from sales and dividends)

Cost of goods sold

Expenses

P (300, 000) P (200, 000)

140, 000

20, 000

P (140, 000) P (110, 000)

80, 000

10, 000

Net Income

Retained earnings 1/1

P (300, 000) P (150, 000)

(110, 000)

10,000

P (440, 000) P (250, 000)

Net Income

(140, 000)

Dividends paid

Retained earnings 12/31

-0-

P 210, 000

150, 000

260, 000

440, 000

P 1,060, 000

Cash and Receivables

P90, 000

110, 000

Inventory

Investment in SS

Equipment (net)

Total Assets

-0-

300, 000

P500, 000

Liabilities

P (420, 000) P (150, 000)

(200, 000)

(440, 000)

P (1,060,000) P (500, 000)

Common stock

(100, 000)

(250, 000)

Retained earnings 12/31

Total Liabilities and Equities

Determine the consolidated assets as of December 31.

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution!

Trending now

This is a popular solution!

Step by step

Solved in 3 steps with 4 images

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, accounting and related others by exploring similar questions and additional content below.Recommended textbooks for you

Intermediate Accounting: Reporting And Analysis

Accounting

ISBN:

9781337788281

Author:

James M. Wahlen, Jefferson P. Jones, Donald Pagach

Publisher:

Cengage Learning

Cornerstones of Financial Accounting

Accounting

ISBN:

9781337690881

Author:

Jay Rich, Jeff Jones

Publisher:

Cengage Learning

Intermediate Accounting: Reporting And Analysis

Accounting

ISBN:

9781337788281

Author:

James M. Wahlen, Jefferson P. Jones, Donald Pagach

Publisher:

Cengage Learning

Cornerstones of Financial Accounting

Accounting

ISBN:

9781337690881

Author:

Jay Rich, Jeff Jones

Publisher:

Cengage Learning

Financial Reporting, Financial Statement Analysis…

Finance

ISBN:

9781285190907

Author:

James M. Wahlen, Stephen P. Baginski, Mark Bradshaw

Publisher:

Cengage Learning