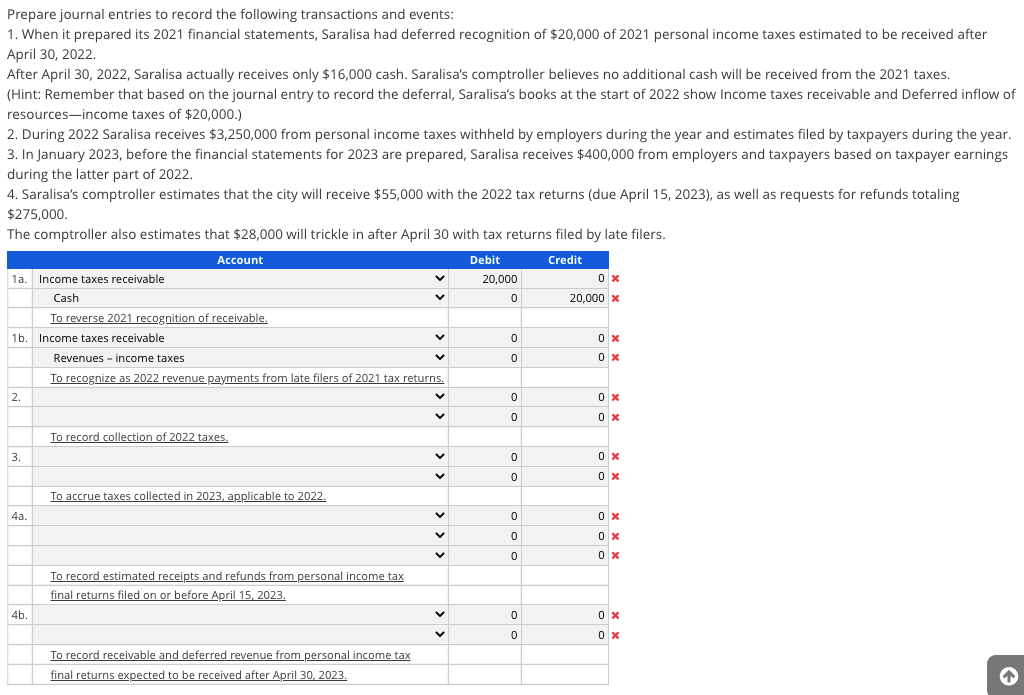

Prepare journal entries to record the following transactions and events: 1. When it prepared its 2021 financial statements, Saralisa had deferred recognition of $20,000 of 2021 personal income taxes estimated to be received after April 30, 2022. After April 30, 2022, Saralisa actually receives only $16,000 cash. Saralisa's comptroller believes no additional cash will be received from the 2021 taxes. (Hint: Remember that based on the journal entry to record the deferral, Saralisa's books at the start of 2022 show Income taxes receivable and Deferred inflow of resources-income taxes of $20,000.) 2. During 2022 Saralisa receives $3,250,000 from personal income taxes withheld by employers during the year and estimates filed by taxpayers during the year. 3. In January 2023, before the financial statements for 2023 are prepared, Saralisa receives $400,000 from employers and taxpayers based on taxpayer earnings during the latter part of 2022. 4. Saralisa's comptroller estimates that the city will receive $55,000 with the 2022 tax returns (due April 15, 2023), as well as requests for refunds totaling $275,000. The comptroller also estimates that $28,000 will trickle in after April 30 with tax returns filed by late filers. Account Debit Credit la. Income taxes receivable 20,000 Cash 20,000 x To reverse 2021 recognition of receivable. 1b. Income taxes receivable 0 x Revenues - income taxes 0 x To recognize as 2022 revenue payments from late filers of 2021 tax returns. 2. 0 x To record collection of 2022 taxes. 3. 0 x To accrue taxes collected in 2023, applicable to 2022. 4a. 0 x To record estimated receipts and refunds from personal income tax final returns filed on or before April 15, 2023. 4b. 0 x To record receivable and deferred revenue from personal income tax final returns expected to be received after April 30, 2023.

Accounting for personal income taxes

Saralisa City, which operates on a calendar year basis, obtains 40 percent of its revenues from personal income taxes. Employers are required to withhold taxes from the earnings of city residents and remit them to the city monthly.

City residents must also make payments, if necessary, with quarterly tax estimates. No later than April 15 of the following year, residents must file tax returns, remitting any additional taxes due to the city or claiming refunds of overpayments.

Saralisa’s accounting policies call for recognizing taxes obtained from income earned during a particular calendar year provided the taxes are received during the year or before April 30 of the following year;

income taxes received after April 30 are recognized as revenues of the year in which received.

Trending now

This is a popular solution!

Step by step

Solved in 2 steps with 1 images