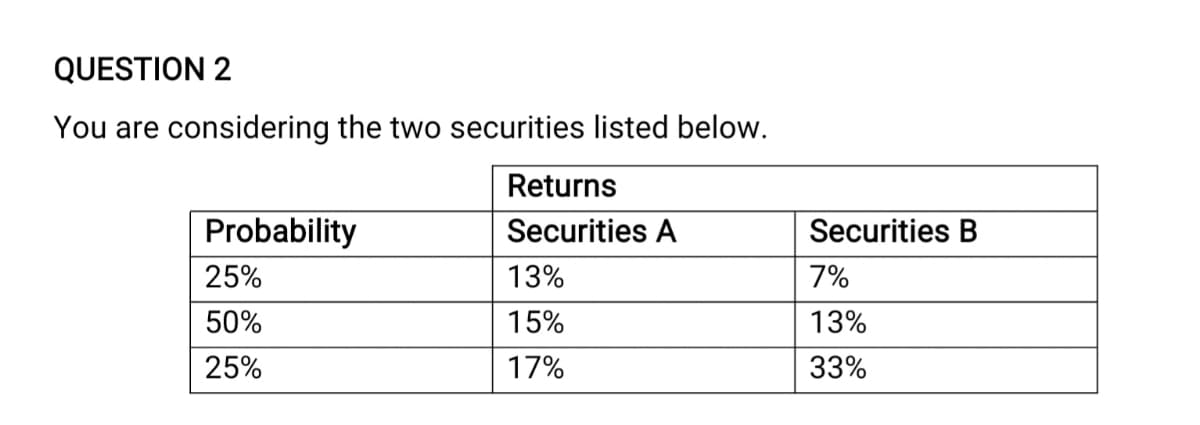

QUESTION 2 You are considering the two securities listed below. Returns Probability Securities A Securities B 25% 13% 7% 50% 15% 13% 25% 17% 33%

Q: Consider the following data for two risk factors (1 and 2) and two securities (J and L): λ0 = 0.07…

A: We’ll answer the first question since the exact one wasn’t specified. Please submit a new question…

Q: Calculate the expected rate of return on this risk-free portfolio? (Hint: Can a particular stock…

A: The Capital Asset Pricing Model (CAPM) describes the relationship between systematic risk and…

Q: Calculate the expected return of portfolio and standard deviation of portfolio of 3 Assets (Security…

A: Given information : Probablity Security B Security C Security D Recession 0.1 -29.50% 24.50%…

Q: Suppose Stock A has ß = 1 and an expected return of 11%. Stock B has a B = 1.5. The risk- free rate…

A: The Capital Asset Pricing Model, Expected return will be calculated as under Ke = Rf + β (Rm -…

Q: When P12 =+1, the standard deviation of a two-security portfolio P is equal to the weighted average…

A: Part B. The portfolios along the (EF) efficient frontier are those that deliver the highest returns…

Q: You have been provided the following data on the securities of three firms, the market portfolio,…

A: By using the above formula we calculate the missing figures for different stocks. Beta of the market…

Q: Assume a portfolio with weights of 0.60 in stocks and 0.40 in bonds. a. What is the rate of…

A: A portfolio is made up diffreent types of financial assets in which investments are made. Here the…

Q: What are the expected returns for stocks Y and Z under the conditions shown below? A0 0.04…

A: Calculation of Expected Return for Stock Y:

Q: Suppose that a portfolio consist of three securities: A, B and C with expected rates of return of…

A: Portfolio refers to basket of different financial assets in which investment is made by single…

Q: eta A $

A: Beta of portfolio is weighted average beta. Portfolio beta = Sum of [ Weigh of each security * Beta…

Q: Security Sinle-index Model Estimates X Y 2 3 1 Bi 1.5 1.3 0.8 o(e.) 3% 1% 2% Given the data for…

A: Expected Return on each security: E_X = alpha_i + Beta_i*E(r_m) = 2 + 1.5*0.08 = 2.12% Similarly,…

Q: Consider the following scenario analysis: Rate of Return Scenario Probability Stocks Bonds…

A: Expected return on a portfolio is the weighted average of expected return of each of its constituent…

Q: The following below are the expected return and betas of the given set of securities. Given that the…

A: Market Risk Premium = Market Risk Premium-Risk Free Rate =13%-7% =6%

Q: Consider the following information about expected returns for two securities, Raven wood Consulting…

A: Probability is a topic of mathematics concerned with numerical explanations of the likelihood of an…

Q: Consider the following table, which gives a security analyst's expected retum on two stocks for two…

A: The table is: Market Return Stock A Stock B 10% 5% 12 20% 25 15

Q: What would be the beta of this portfolio?

A: Beta shows the relation between systematic risk of the investment and the expected return of the…

Q: Consider the following simplified APT model: Factor Expected Risk Premium Market 6.4% Interest…

A: The Arbitrage Pricing Theory (APT) model is the asset pricing model that is used to determine the…

Q: An investor wishes to contruct a portfolio consisting of security 1 and security 2. the expected…

A: Portfolio Return = (R1*W1)+ (R2*W2) Portfolio Risk = square root of [(R1*W1)^2 + (R2*W2)^2 +…

Q: A non-dividend-paying stock has a current price of 800 ngwee. In any unit of time (t, t + 1) the…

A: Given, (a) (u )= 25% Increase in % = 1 + 25% = 1.25 d = 20% Decrease % = 1 - 20% = 0.80 R = 1.04 Up…

Q: Q2) Consider the following information given below and do the following; a) Estimate monthly…

A: In investing, risk and return are highly correlated. Increased potential returns on investment…

Q: 1. Risk free rate represents: a. The market rate of return b. The rate provided by long term…

A: 1. Risk free rate is the rate which is expected by investor with no risks.

Q: Two question is connected So I attached together But the question I want to solve is A.2! I'm…

A: Since we only answer up to 3 sub-parts, we’ll answer the first 3. Please resubmit the question and…

Q: (b') Details of the shares held in a portfolio are given below: Securities Beta Expected Return…

A: Share Percentage Held Expected Return Beta A 26% 14% 1.1 B 18% 10% 0.8 C 31% 18% 1.7 T-Bill…

Q: sisting of the föllowir STOCK OR SECURITY 1. F 2. 3 4. The risk-free rate is 4 pe a. Calculate the…

A: Note : As per our guidelines, we can only answer three subparts at once. Please post other subparts…

Q: Calculate the average returns, variance and standard deviation for three securities X, Y and Z that…

A: Average Return, variance and standard deviation of a security is calculated using the below formula…

Q: Suppose that there are many stocks in the security market and that the characteristics of stocks A…

A: Calculation of risk free rate of return: Excel workings:

Q: E(R) E(R) E(R) A A B.

A: The most appropriate image that represents the risk and returns characteristics of a portfolio is…

Q: Consider the following table, which gives a security analyst's expected return on two stocks and the…

A: Answer - Part A - Calculation of betas of the two stocks : Beta A = Difference in Rate of Return…

Q: Suppose that there are many stocks in the security market and that the characteristics of stocks A…

A: As the correlation between the stocks is -1. Standard deviation for portfolio will be written as:…

Q: 7-11. SML Assume that the risk free rate is 2%, the market risk premium is 5%, and the beta of two…

A: The Capital Asset Pricing Model (CAPM) is an equilibrium model that calculates an asset's risk and…

Q: Three securities have the characteristics described in the following table: A C Return Return Return…

A: Return simply means the benefits received from an investment. When an investor makes an investment,…

Q: A discrete-time financial market has two risky securities, whose prices are S1 (0) = Question 1. 10…

A: Data given: At t=0 Portfolio is worth = 100 w1 = 30% w2 = 70% Price S1(0) = 10 Price S2(0) = 20 At…

Q: Below is a table of probabilities and expected returns for 2 securities under 3 possible scenarios:…

A: Expected rate of return is the profit or loss on the investor that is assumed to be anticipated by…

Q: Consider the following simplified APT model: Factor Expected Risk Premium Market 6.4% Interest…

A: Arbitrage Pricing Theory The concept behind the multi-factor asset pricing model known as arbitrage…

Q: Security 1 8% 13% 18% Security 2 9% .15 .1 .05 11% .1 .2 .1 13% .05 .1 .15 a) Compute the expected…

A: Security 1=8*(0.15+0.1+0.05)+13*(0.1+0.2+0.1)+18*(0.05+0.1+0.15) =13%

Q: You are expected to assess the stand-alone risk of each of the stock using the Sharpe Ratio. The…

A: Sharpe Rario:- The excess return earned over the risk free return on portfolio to the portfolio’s…

Q: equired: 1. Calculate the expected return for the above stocks. Assume risk free rate is 5%.…

A: This post has three questions. Questions 1 and 3 have been answered below.

Q: Suppose that there are many stocks in the security market and that the characteristics of stocks A…

A: Given:

Q: A financial analyst for the ZZZ Corporation uses the Security Market line to estimate the cost of…

A: In the given question we require to calculate the value of [E(Rm) - Rf ] RE = Cost of Equity = 13%…

Q: Suppose you are given the following information about 2 stocks, what is the expected return of a…

A: Expected return of A is 16% Expected return of B is 8% Weight of Stock A is 55% Weight of Stock B is…

Q: 7. The following data are available to you as portfolio manager: Estimated retum (%) Security A Beta…

A: As per CAPM Expected return = Risk free rate +beta * (market return - risk free rate)

Q: Consider the following simplified APT model: Factor Expected Risk Premium Market 6.4% Interest…

A: Expected return on stock =Risk free rate +risk premium x risk exposure factor Expected return on…

Q: The reward-to-risk ratio for Stock X, in decimal form, is ______. Round your answer to 3 decimal…

A:

Trending now

This is a popular solution!

Step by step

Solved in 3 steps with 3 images

- D1 = $1.25, g = 6.00%, β = 1.15, market risk premium = 5.5%, and risk free rate = 4 %. Find the stock price $28.90 $28.62 $29.36 $30.12QUESTION 3 – Risk and ReturnSintok Corporation has collected information on the following three investments. Which investment is the most favourable based on the information presented?Stock A Stock B Stock CProbability Return Probability Return Probability Return0.15 2% 0.25 -3% 0.1 -5%0.4 7% 0.5 20% 0.4 10%0.3 10% 0.25 25% 0.3 15%0.15 15% 0.2 30%D1 = $1, g = 6.00%, β = 2, market risk premium = 5 %, and risk free rate = 5 %. Find stock price (Hint: r = risk free rate + beta * market risk premium = 5% + 2*5%) $11.11 $8.93 $10.08 $9.56

- Q2 - Returns on stocks X and Y are listed below: Period 1 2 3 4 5 6 7Stock X 4% -2% 5% -1% 10% 7% 12%Stock Y -3% 7% 4% 2% 2% 8% -3% Consider a portfolio of 10% stock X and 90% stock Y. What is the mean of portfolio returns? Please specify your answer in decimal terms and round your answer to the nearest thousandth (e.g., enter 12.3 percent as 0.123).D4) Finance Consider a portfolio composed of shares AAA and BBB as shown in the following table. At 95% confidence level, select the correct statement AAA BBB Value 2,470,000 785,750 % investment 76% 24% Volatilities 2.32 % 2.69 % Correlation for both assets 0.65 Portfolio Value for both assets 3,255,750 a) The Component VaR of the Asset AAA is 92,223 and the component VaR of the Asset BBB is 27955.69 b) The contribution to the VaR of the Asset AAA is 77% and the one of the Asset 2 is 23% c) Both answers are correctFirm A’s D1 = $1.75 / share. Secondly, growth rate = -1.5%. return =14%. Calculate stock price. A) $11.29 B) $12.64 C) $13.27 D) $14.00 E) $14.21

- A4 5c Consider the following information on three stocks in four possible future states of the economy: State of economy Probability of state of economy Stock A Stock B Stock C Boom 0.3 0.35 0.45 0.38 Good 0.3 0.15 0.20 0.12 Poor 0.3 0.05 –0.10 –0.05 Bust 0.1 0.00 –0.30 –0.10 stock A: State of economy Probability Rate of return Average (a) (b) (c) (d = b × c)(d = b × c) Boom 0.3 0.35 0.105 Good 0.3 0.15 0.045 Poor 0.3 0.05 0.015 Bust 0.1 0 0 Expected rate of return 0.165 stock B: State of economy Probability Rate of return Average (a) (b) (c) (d = b × c)(d = b × c) Boom 0.3 0.45 0.135 Good 0.3 0.2 0.06 Poor 0.3 -0.1 -0.03 Bust 0.1 -0.3 -0.03 Expected rate of return 0.135 Stock C: State of economy Probability Rate of return Average (a) (b) (c) (d = b × c)(d = b…Data: S0 = 107; X = 110; 1+r = 1.12. The two possibilities for ST are 155 and 95. (Round to 2 decimal places). a. The range of S is 60 while that of P is 15 across the two states. What is the hedge ratio of the put? Hedge ratio ? b. Form a portfolio of one share of stock and four puts. What is the (nonrandom) payoff to this portfolio? Nonrandom payoff c. What is the present value of the portfolio? Present value d. Given that the stock is currently selling at 107, calculate the put value. Put valueQuestion: There are three securities in the market. The following chart shows their possible payoffs: &n... Edit question There are three securities in the market. The following chart shows their possible payoffs: State Probabilityof Outcome Return on Security 1 Return on Security 2 Return on Security 3 1 .14 .199 .199 .049 2 .36 .149 .099 .099 3 .36 .099 .149 .149 4 .14 .049 .049 .199 a-1. What is the expected return of each security? (Do not round intermediate calculations and enter your answers as a percent rounded to 2 decimal places, e.g., 32.16.) Answer 12.40% a-2. What is the standard deviation of each security? (Do not round intermediate calculations and enter your answers as a percent rounded to 2 decimal places, e.g., 32.16.) Answer 4.50% b-1. What are the covariances between the pairs of securities? (A negative answer should be indicated by a minus sign. Do not round intermediate calculations and round your…

- INV 2-3a You are exploring the use of APT in making investment choices. You have identified three factors labelled F1, F2, and F3 with corresponding risk premia RP1 = 4%, RP2 = 5%, and RP3 = 2%. A stock with ticker ABC has historically shown returns which have followed the equation: rABC=0.12+.75F1+1.0F2+.5F3+eABC a. What is the equilibrium rate of return for stock ABC using the APT, if the T-bill rate is 4%?Q2) Calculate Expected return and standard deviation of returns if the investor purchases the stock at $290 Event Probability Share Price Dividend A .10 330 4 B .15 320 3 C .30 300 3 D .20 290 4 E .25 280 4Condition Probability Grn Bond Stock A Stock B Market Recession 0.1 8.0% -22% 28% -13% Below average 0.2 8.0% -2% 14.7% 1% Average 0.4 8.0% 20% 0% 15% Above average 0.2 8.0% 35% -10% 29% Boom 0.1 8.0% 50% -20% 43% Expected Return 8% 17.4% 1.74% ? Standard Deviation 0% ? 13.36% 15.34% Beta 0 1.29 ? 1 Required Construct the SML of the above four alternative. Clearly indicate stock A and stock B have been under/over or fairly priced.