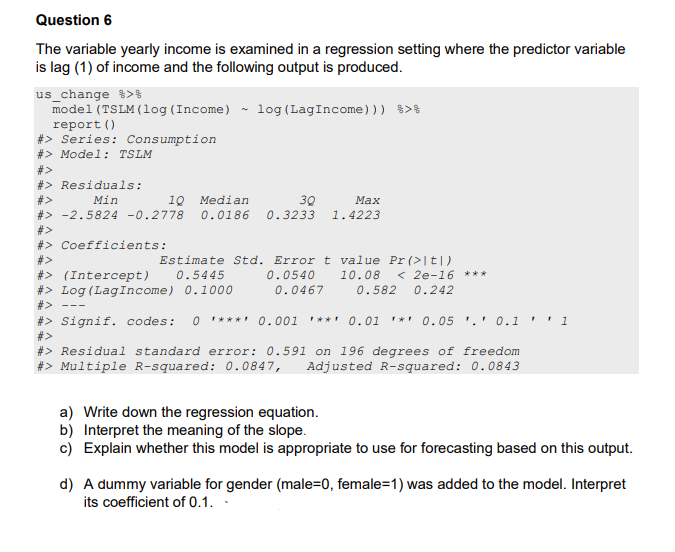

Question 6 The variable yearly income is examined in a regression setting where the predictor variable is lag (1) of income and the following output is produced. us_change %>8 model (TSLM (log (Income) log (LagIncome))) %>% report() #> Series: Consumption #> Model: TSLM #> #> Residuals: #> Min 10 Median 30 #> -2.5824 -0.2778 0.0186 0.3233 <# #> #> Coefficients: Max 1.4223 Estimate Std. Error t value Pr (>|t|) 0.0540 10.08 < 2e-16 *** 0.0467 0.582 0.242 #> (Intercept) 0.5445 #> Log (LagIncome) 0.1000 #> --- #> Signif. codes: 0 ***** 0.001*** 0.01 * 0.05. 0.1 #> #> Residual standard error: 0.591 on 196 degrees of freedom #> Multiple R-squared: 0.0847, Adjusted R-squared: 0.0843 1 a) Write down the regression equation. b) Interpret the meaning of the slope. c) Explain whether this model is appropriate to use for forecasting based on this output.

Question 6 The variable yearly income is examined in a regression setting where the predictor variable is lag (1) of income and the following output is produced. us_change %>8 model (TSLM (log (Income) log (LagIncome))) %>% report() #> Series: Consumption #> Model: TSLM #> #> Residuals: #> Min 10 Median 30 #> -2.5824 -0.2778 0.0186 0.3233 <# #> #> Coefficients: Max 1.4223 Estimate Std. Error t value Pr (>|t|) 0.0540 10.08 < 2e-16 *** 0.0467 0.582 0.242 #> (Intercept) 0.5445 #> Log (LagIncome) 0.1000 #> --- #> Signif. codes: 0 ***** 0.001*** 0.01 * 0.05. 0.1 #> #> Residual standard error: 0.591 on 196 degrees of freedom #> Multiple R-squared: 0.0847, Adjusted R-squared: 0.0843 1 a) Write down the regression equation. b) Interpret the meaning of the slope. c) Explain whether this model is appropriate to use for forecasting based on this output.

Trigonometry (MindTap Course List)

8th Edition

ISBN:9781305652224

Author:Charles P. McKeague, Mark D. Turner

Publisher:Charles P. McKeague, Mark D. Turner

Chapter4: Graphing And Inverse Functions

Section: Chapter Questions

Problem 6GP: If your graphing calculator is capable of computing a least-squares sinusoidal regression model, use...

Related questions

Question

Transcribed Image Text:Question 6

The variable yearly income is examined in a regression setting where the predictor variable

is lag (1) of income and the following output is produced.

us_change %>%

model (TSLM (log (Income) ~ log (LagIncome))) %>%

report ()

#> Series: Consumption

#> Model: TSLM

#>

#> Residuals:

Min

10 Median

30

#> -2.5824 -0.2778 0.0186 0.3233

#>

#> Coefficients:

Max

1.4223

#>

#> (Intercept) 0.5445

#> Log (LagIncome) 0.1000

#>

Estimate Std. Error t value Pr (>|t|)

0.0540 10.08 < 2e-16 ***

0.0467 0.582 0.242

#> Signif. codes: 0 ***** 0.001 **** 0.01 * 0.05. 0.1

#>

#> Residual standard error: 0.591 on 196 degrees of freedom

#> Multiple R-squared: 0.0847, Adjusted R-squared: 0.0843

1

a) Write down the regression equation.

b) Interpret the meaning of the slope.

c) Explain whether this model is appropriate to use for forecasting based on this output.

d) A dummy variable for gender (male=0, female=1) was added to the model. Interpret

its coefficient of 0.1..

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

Step by step

Solved in 4 steps

Recommended textbooks for you

Trigonometry (MindTap Course List)

Trigonometry

ISBN:

9781305652224

Author:

Charles P. McKeague, Mark D. Turner

Publisher:

Cengage Learning

Trigonometry (MindTap Course List)

Trigonometry

ISBN:

9781305652224

Author:

Charles P. McKeague, Mark D. Turner

Publisher:

Cengage Learning