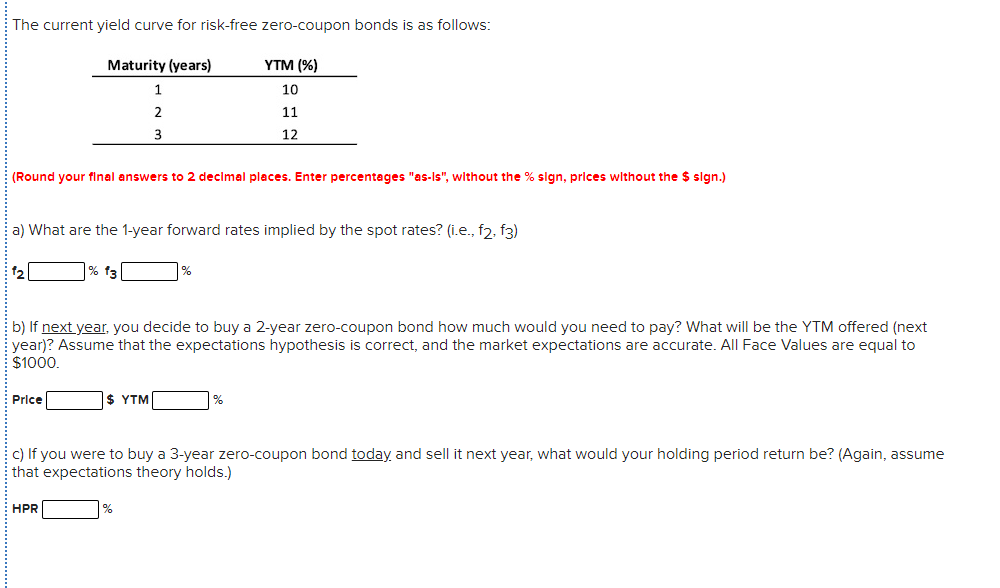

The current yield curve for risk-free zero-coupon bonds is as follows: Maturity (years) YTM (%) 10 11 12 (Round your final answers to 2 decimal places. Enter percentages "as-Is", without the % sign, prices without the $ sign.) a) What are the 1-year forward rates implied by the spot rates? (i.e., f2, f3) 12 % 13 % b) If next year, you decide to buy a 2-year zero-coupon bond how much would you need to pay? What will be the YTM offered (next year)? Assume that the expectations hypothesis is correct, and the market expectations are accurate. All Face Values are equal to $1000. $ YTM Price c) If you were to buy a 3-year zero-coupon bond today and sell it next year, what would your holding period return be? (Again, assume that expectations theory holds.) HPR

Debenture Valuation

A debenture is a private and long-term debt instrument issued by financial, non-financial institutions, governments, or corporations. A debenture is classified as a type of bond, where the instrument carries a fixed rate of interest, commonly known as the ‘coupon rate.’ Debentures are documented in an indenture, clearly specifying the type of debenture, the rate and method of interest computation, and maturity date.

Note Valuation

It is the process to determine the value or worth of an asset, liability, debt of the company. It can be determined by many processes or techniques. Many factors can impact the valuation of an asset, liability, or the company, like:

Trending now

This is a popular solution!

Step by step

Solved in 7 steps with 7 images