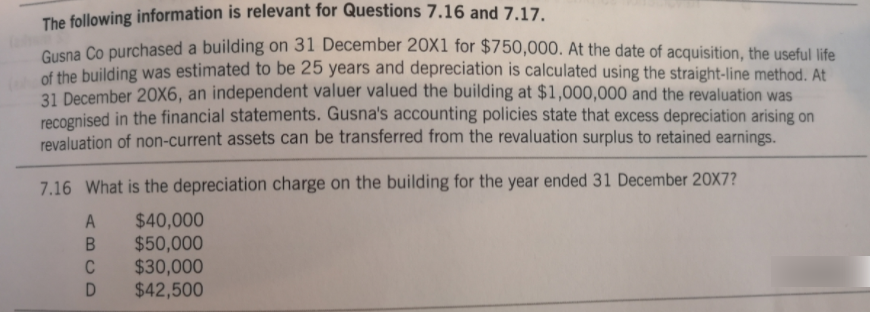

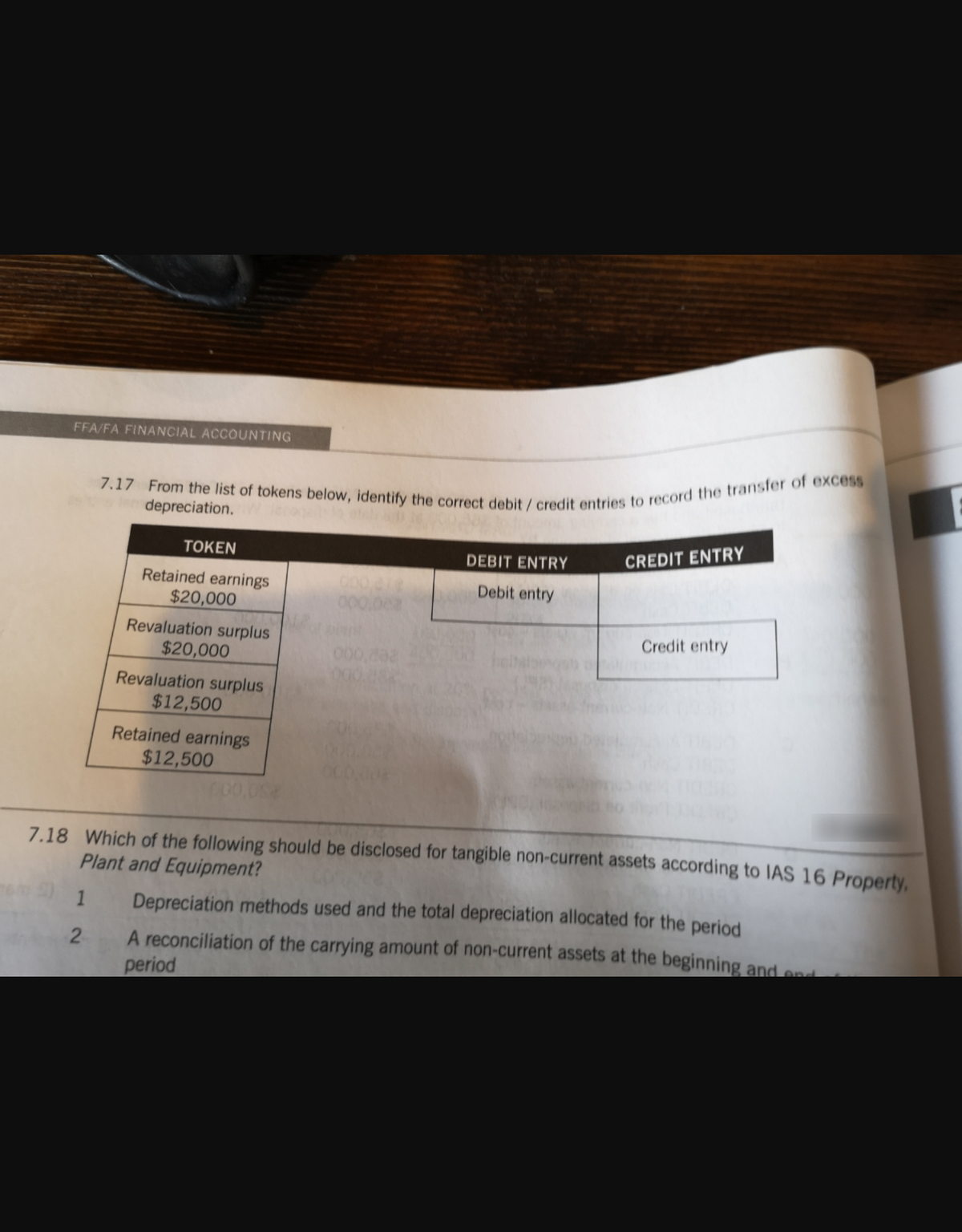

The following information is relevant for Questions 7.16 and 7.17. Gusna Co purchased a building on 31 December 20x1 for $750,000. At the date of acquisition, the useful life of the building was estimated to be 25 years and depreciation is calculated using the straight-line method. At 31 December 20X6, an independent valuer valued the building at $1,000,000 and the revaluation was recoenised in the financial statements. Gusna's accounting policies state that excess depreciation arising on revaluation of non-current assets can be transferred from the revaluation surplus to retained earnings. 7.16 What is the depreciation charge on the building for the year ended 31 December 20X7? $40,000 $50,000 $30,000 $42,500 A C 7.17 From the list of tokens below, identify the correct debit / credit entries to record the transfer of excess FFA/FA FINANCIAL ACCOUNTING depreciation. TOKEN CREDIT ENTRY DEBIT ENTRY Retained earnings $20,000 Debit entry 000,0ea Revaluation surplus Credit entry $20,000 Revaluation surplus $12,500 Retained earnings $12,500 7.18 Which of the following should be disclosed for tangible non-current assets according to IAS 16 Property. Plant and Equipment? 1 Depreciation methods used and the total depreciation allocated for the period 2 A reconciliation of the carrying amount of non-current assets at the beginning and end period

The following information is relevant for Questions 7.16 and 7.17. Gusna Co purchased a building on 31 December 20x1 for $750,000. At the date of acquisition, the useful life of the building was estimated to be 25 years and depreciation is calculated using the straight-line method. At 31 December 20X6, an independent valuer valued the building at $1,000,000 and the revaluation was recoenised in the financial statements. Gusna's accounting policies state that excess depreciation arising on revaluation of non-current assets can be transferred from the revaluation surplus to retained earnings. 7.16 What is the depreciation charge on the building for the year ended 31 December 20X7? $40,000 $50,000 $30,000 $42,500 A C 7.17 From the list of tokens below, identify the correct debit / credit entries to record the transfer of excess FFA/FA FINANCIAL ACCOUNTING depreciation. TOKEN CREDIT ENTRY DEBIT ENTRY Retained earnings $20,000 Debit entry 000,0ea Revaluation surplus Credit entry $20,000 Revaluation surplus $12,500 Retained earnings $12,500 7.18 Which of the following should be disclosed for tangible non-current assets according to IAS 16 Property. Plant and Equipment? 1 Depreciation methods used and the total depreciation allocated for the period 2 A reconciliation of the carrying amount of non-current assets at the beginning and end period

Intermediate Accounting: Reporting And Analysis

3rd Edition

ISBN:9781337788281

Author:James M. Wahlen, Jefferson P. Jones, Donald Pagach

Publisher:James M. Wahlen, Jefferson P. Jones, Donald Pagach

Chapter11: Depreciation, Depletion, Impairment, And Disposal

Section: Chapter Questions

Problem 7E: Loban Company purchased four cars for 9,000 each and expects that they will be sold in 3 years for...

Related questions

Question

Question 7.17 please explained in detail.

Transcribed Image Text:The following information is relevant for Questions 7.16 and 7.17.

Gusna Co purchased a building on 31 December 20x1 for $750,000. At the date of acquisition, the useful life

of the building was estimated to be 25 years and depreciation is calculated using the straight-line method. At

31 December 20X6, an independent valuer valued the building at $1,000,000 and the revaluation was

recoenised in the financial statements. Gusna's accounting policies state that excess depreciation arising on

revaluation of non-current assets can be transferred from the revaluation surplus to retained earnings.

7.16 What is the depreciation charge on the building for the year ended 31 December 20X7?

$40,000

$50,000

$30,000

$42,500

A

C

Transcribed Image Text:7.17 From the list of tokens below, identify the correct debit / credit entries to record the transfer of excess

FFA/FA FINANCIAL ACCOUNTING

depreciation.

TOKEN

CREDIT ENTRY

DEBIT ENTRY

Retained earnings

$20,000

Debit entry

000,0ea

Revaluation surplus

Credit entry

$20,000

Revaluation surplus

$12,500

Retained earnings

$12,500

7.18 Which of the following should be disclosed for tangible non-current assets according to IAS 16 Property.

Plant and Equipment?

1

Depreciation methods used and the total depreciation allocated for the period

2

A reconciliation of the carrying amount of non-current assets at the beginning and end

period

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

Step by step

Solved in 2 steps with 2 images

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, accounting and related others by exploring similar questions and additional content below.Recommended textbooks for you

Intermediate Accounting: Reporting And Analysis

Accounting

ISBN:

9781337788281

Author:

James M. Wahlen, Jefferson P. Jones, Donald Pagach

Publisher:

Cengage Learning

Principles of Accounting Volume 1

Accounting

ISBN:

9781947172685

Author:

OpenStax

Publisher:

OpenStax College

Intermediate Accounting: Reporting And Analysis

Accounting

ISBN:

9781337788281

Author:

James M. Wahlen, Jefferson P. Jones, Donald Pagach

Publisher:

Cengage Learning

Principles of Accounting Volume 1

Accounting

ISBN:

9781947172685

Author:

OpenStax

Publisher:

OpenStax College

Financial Accounting: The Impact on Decision Make…

Accounting

ISBN:

9781305654174

Author:

Gary A. Porter, Curtis L. Norton

Publisher:

Cengage Learning