The share premium recognized on a convertible bond O A. remains in equity only if the bonds are actually converted B. reclassified out of equity to profit or loss if the bonds are not converted O c. remains in equity whether the bonds are actually converted or not D. recognized as gain or loss on conversion E. becomes part of the bonds payable account

The share premium recognized on a convertible bond O A. remains in equity only if the bonds are actually converted B. reclassified out of equity to profit or loss if the bonds are not converted O c. remains in equity whether the bonds are actually converted or not D. recognized as gain or loss on conversion E. becomes part of the bonds payable account

Chapter13: Long-term Liabilities

Section: Chapter Questions

Problem 4MC: A convertible bond can be converted into ________. A. preferred stock B. common stock and then...

Related questions

Question

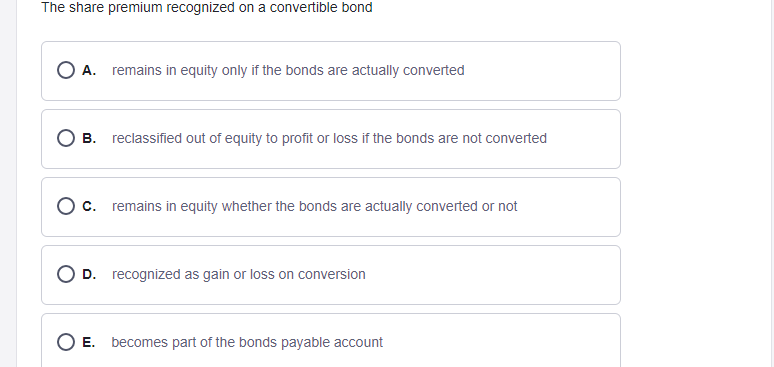

Transcribed Image Text:The share premium recognized on a convertible bond

O A. remains in equity only if the bonds are actually converted

В.

reclassified out of equity to profit or loss if the bonds are not converted

O c. remains in equity whether the bonds are actually converted or not

O D. recognized as gain or loss on conversion

E. becomes part of the bonds payable account

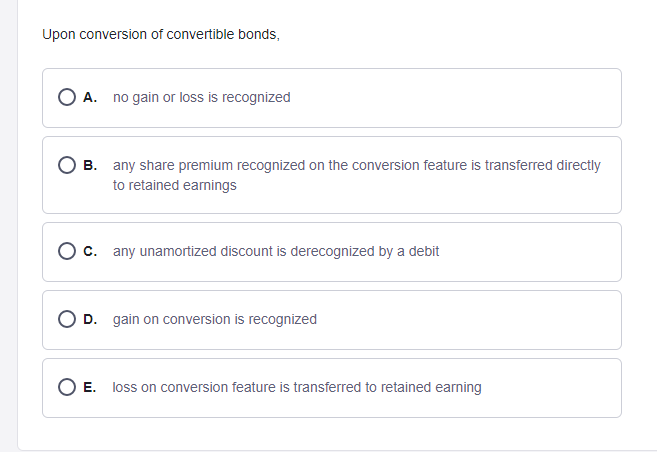

Transcribed Image Text:Upon conversion of convertible bonds,

A.

no gain or loss is recognized

B. any share premium recognized on the conversion feature is transferred directly

to retained eamings

O c. any unamortized discount is derecognized by a debit

D. gain on conversion is recognized

O E. loss on conversion feature is transferred to retained earning

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

Step by step

Solved in 3 steps

Recommended textbooks for you

Principles of Accounting Volume 1

Accounting

ISBN:

9781947172685

Author:

OpenStax

Publisher:

OpenStax College

Financial Reporting, Financial Statement Analysis…

Finance

ISBN:

9781285190907

Author:

James M. Wahlen, Stephen P. Baginski, Mark Bradshaw

Publisher:

Cengage Learning

Principles of Accounting Volume 1

Accounting

ISBN:

9781947172685

Author:

OpenStax

Publisher:

OpenStax College

Financial Reporting, Financial Statement Analysis…

Finance

ISBN:

9781285190907

Author:

James M. Wahlen, Stephen P. Baginski, Mark Bradshaw

Publisher:

Cengage Learning