Unrealized holding gains and losses for trading securities are: a) Reported as a separate com ponent of the shareholder's equity section of the balance sheet, i.e., other comprehensive income b) Included in the determination of income from operations in the period of the change c) Reported as extraordinary items d) Not reported in the income statement nor the balance sheet

Unrealized holding gains and losses for trading securities are: a) Reported as a separate com ponent of the shareholder's equity section of the balance sheet, i.e., other comprehensive income b) Included in the determination of income from operations in the period of the change c) Reported as extraordinary items d) Not reported in the income statement nor the balance sheet

Auditing: A Risk Based-Approach (MindTap Course List)

11th Edition

ISBN:9781337619455

Author:Karla M Johnstone, Audrey A. Gramling, Larry E. Rittenberg

Publisher:Karla M Johnstone, Audrey A. Gramling, Larry E. Rittenberg

Chapter10: Auditing Cash, Marketable Securities, And Complex Financial Instruments

Section: Chapter Questions

Problem 28RQSC

Related questions

Question

Please i need all questions to be answered.

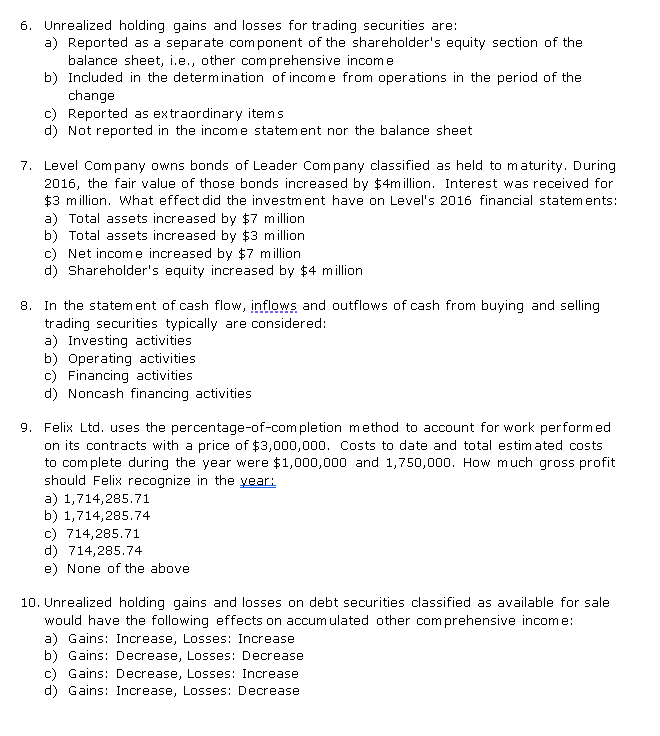

Transcribed Image Text:6. Unrealized holding gains and losses for trading securities are:

a) Reported as a separate com ponent of the shareholder's equity section of the

balance sheet, i.e., other comprehensive income

b) Included in the determination of income from operations in the period of the

change

c) Reported as extraordinary items

d) Not reported in the income statement nor the balance sheet

7. Level Company owns bonds of Leader Com pany classified as held to maturity. During

2016, the fair value of those bonds increased by $4million. Interest was received for

$3 million. What effect did the investment have on Level's 2016 financial statements:

a) Total assets increased by $7 million

b) Total assets increased by $3 million

c) Net income increased by $7 million

d) Shareholder's equity increased by $4 million

8. In the statement of cash flow, inflows and outflows of cash from buying and selling

trading securities typically are considered:

a) Investing activities

b) Operating activities

c) Financing activities

d) Noncash financing activities

9. Felix Ltd. uses the percentage-of-com pletion method to account for work performed

on its contracts with a price of $3,000,000. Costs to date and total estim ated costs

to com plete during the year were $1,000,000 and 1,750,000. How much gross profit

should Felix recognize in the year:

a) 1,714,285.71

b) 1,714,285.74

c) 714,285.71

d) 714,285.74

e) None of the above

10. Unrealized holding gains and losses on debt securities classified as available for sale

would have the following effects on accum ulated other comprehensive income:

a) Gains: Increase, Losses: Increase

b) Gains: Decrease, Losses: Decrease

c) Gains: Decrease, Losses: Increase

d) Gains: Increase, Losses: Decrease

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution!

Trending now

This is a popular solution!

Step by step

Solved in 2 steps

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, accounting and related others by exploring similar questions and additional content below.Recommended textbooks for you

Auditing: A Risk Based-Approach (MindTap Course L…

Accounting

ISBN:

9781337619455

Author:

Karla M Johnstone, Audrey A. Gramling, Larry E. Rittenberg

Publisher:

Cengage Learning

Financial Reporting, Financial Statement Analysis…

Finance

ISBN:

9781285190907

Author:

James M. Wahlen, Stephen P. Baginski, Mark Bradshaw

Publisher:

Cengage Learning

Auditing: A Risk Based-Approach (MindTap Course L…

Accounting

ISBN:

9781337619455

Author:

Karla M Johnstone, Audrey A. Gramling, Larry E. Rittenberg

Publisher:

Cengage Learning

Financial Reporting, Financial Statement Analysis…

Finance

ISBN:

9781285190907

Author:

James M. Wahlen, Stephen P. Baginski, Mark Bradshaw

Publisher:

Cengage Learning