You are given the following information about the yield curve: the 1-, and 2-year yields are y1 = 4.5% and y2 = 5.5%, respectively. A 2-year annual 5% coupon bond with a face value of $1,000 is currently selling for $1,000. Assume the first coupon will not be paid until one year from now. Is there an arbitrage opportunity and, if so, how would you explolt it (assume we cannot trade in fractions of a penny)? A. There is no arbitrage opportunity B. Yes: Buy the bond and fund this by shorting a $50 face value 1-year discount bond and a $1,050 face value 2-year discount bond C. Yes: Buy the bond and fund this by shorting a $47.85 face value 1-year discount bond and a $943.38 face value 2-year discount bond D. Yes: Short the bond and buy a $50 face value 1-year discount bond and a $1,050 face value 2-year discount bond E. Yes: Short the bond and buy a $47.85 face value 1-year discount bond and a $943.38 face value 2-year discount bond

You are given the following information about the yield curve: the 1-, and 2-year yields are y1 = 4.5% and y2 = 5.5%, respectively. A 2-year annual 5% coupon bond with a face value of $1,000 is currently selling for $1,000. Assume the first coupon will not be paid until one year from now. Is there an arbitrage opportunity and, if so, how would you explolt it (assume we cannot trade in fractions of a penny)? A. There is no arbitrage opportunity B. Yes: Buy the bond and fund this by shorting a $50 face value 1-year discount bond and a $1,050 face value 2-year discount bond C. Yes: Buy the bond and fund this by shorting a $47.85 face value 1-year discount bond and a $943.38 face value 2-year discount bond D. Yes: Short the bond and buy a $50 face value 1-year discount bond and a $1,050 face value 2-year discount bond E. Yes: Short the bond and buy a $47.85 face value 1-year discount bond and a $943.38 face value 2-year discount bond

Intermediate Financial Management (MindTap Course List)

13th Edition

ISBN:9781337395083

Author:Eugene F. Brigham, Phillip R. Daves

Publisher:Eugene F. Brigham, Phillip R. Daves

Chapter4: Bond Valuation

Section: Chapter Questions

Problem 8MC: Suppose a 10-year, 10% semiannual coupon bond with a par value of 1,000 is currently selling for...

Related questions

Concept explainers

Debenture Valuation

A debenture is a private and long-term debt instrument issued by financial, non-financial institutions, governments, or corporations. A debenture is classified as a type of bond, where the instrument carries a fixed rate of interest, commonly known as the ‘coupon rate.’ Debentures are documented in an indenture, clearly specifying the type of debenture, the rate and method of interest computation, and maturity date.

Note Valuation

It is the process to determine the value or worth of an asset, liability, debt of the company. It can be determined by many processes or techniques. Many factors can impact the valuation of an asset, liability, or the company, like:

Question

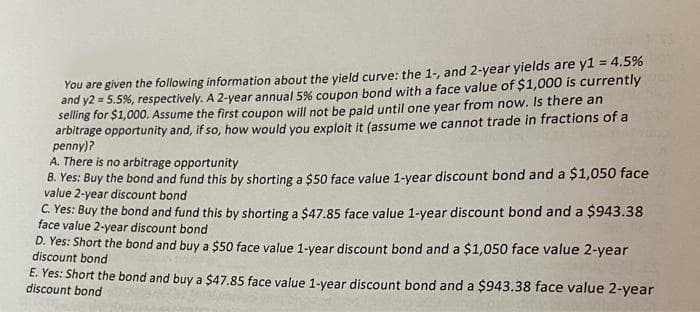

Transcribed Image Text:You are given the following information about the yield curve: the 1-, and 2-year yields are yl = 4.5%

and y2 = 5.5%, respectively. A 2-year annual 5% coupon bond with a face value of $1,000 is currently

selling for $1,000. Assume the first coupon will not be paid until one year from now. Is there an

arbitrage opportunity and, if so, how would you exploit it (assume we cannot trade in fractions of a

penny)?

A. There is no arbitrage opportunity

B. Yes: Buy the bond and fund this by shorting a $50 face value 1-year discount bond and a $1,050 face

value 2-year discount bond

C Yes: Buy the bond and fund this by shorting a $47.85 face value 1-year discount bond and a $943.38

face value 2-year discount bond

D. Yes: Short the bond and buy a $50 face value 1-year discount bond and a $1,050 face value 2-year

discount bond

E. Yes: Short the bond and buy a $47.85 face value 1-vear discount bond and a $943.38 face value 2-year

discount bond

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

Step by step

Solved in 2 steps

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, finance and related others by exploring similar questions and additional content below.Recommended textbooks for you

Intermediate Financial Management (MindTap Course…

Finance

ISBN:

9781337395083

Author:

Eugene F. Brigham, Phillip R. Daves

Publisher:

Cengage Learning

EBK CONTEMPORARY FINANCIAL MANAGEMENT

Finance

ISBN:

9781337514835

Author:

MOYER

Publisher:

CENGAGE LEARNING - CONSIGNMENT

Intermediate Financial Management (MindTap Course…

Finance

ISBN:

9781337395083

Author:

Eugene F. Brigham, Phillip R. Daves

Publisher:

Cengage Learning

EBK CONTEMPORARY FINANCIAL MANAGEMENT

Finance

ISBN:

9781337514835

Author:

MOYER

Publisher:

CENGAGE LEARNING - CONSIGNMENT