1. Cash purchases can be recorded only in the cash payments journal. TF 2. Special jourmals are intended to accommodate large umber of transactions of frequent occurrence an same nature. TF 3. The purchase of furniture and fixture on account should be recorded in the purchases journal. TF 4. Initial investment of cash is recorded in the general journal. TF 5. A general joumal is necessary while the special journal is optional. T F general journal. TF 7. Merchandise inventory counted should be reflected in the general journal. TF 8. The design of special journals should fit the individual need of a particular business. TF 9. Subsidiary ledgers are maintained as support to the general ledger balances. TF 10. The cash payments journal is alternatively called cash disbursements jourmal. TF 11. The cash account in the cash payments journal is a debit entry. T F T F T F T F 6. If the business wants to use the four (4) special journals, it is not necessary for the business to maintair 12. The accounts receivable subsidiary ledger provides the individual account balances of customers or c 13. The use of special journals saves time and cost otherwise spent with the use of general journals. 14. Payments for all purposes are properly recorded in cash payments journal. 15. The requirement that cash receipts should always be deposited is a feature of the imprest system.

1. Cash purchases can be recorded only in the cash payments journal. TF 2. Special jourmals are intended to accommodate large umber of transactions of frequent occurrence an same nature. TF 3. The purchase of furniture and fixture on account should be recorded in the purchases journal. TF 4. Initial investment of cash is recorded in the general journal. TF 5. A general joumal is necessary while the special journal is optional. T F general journal. TF 7. Merchandise inventory counted should be reflected in the general journal. TF 8. The design of special journals should fit the individual need of a particular business. TF 9. Subsidiary ledgers are maintained as support to the general ledger balances. TF 10. The cash payments journal is alternatively called cash disbursements jourmal. TF 11. The cash account in the cash payments journal is a debit entry. T F T F T F T F 6. If the business wants to use the four (4) special journals, it is not necessary for the business to maintair 12. The accounts receivable subsidiary ledger provides the individual account balances of customers or c 13. The use of special journals saves time and cost otherwise spent with the use of general journals. 14. Payments for all purposes are properly recorded in cash payments journal. 15. The requirement that cash receipts should always be deposited is a feature of the imprest system.

Financial Accounting

14th Edition

ISBN:9781305088436

Author:Carl Warren, Jim Reeve, Jonathan Duchac

Publisher:Carl Warren, Jim Reeve, Jonathan Duchac

Chapter5: Accounting Systems

Section: Chapter Questions

Problem 2PA: Transactions related to revenue and cash receipts completed by Albany Architects Co. during the...

Related questions

Question

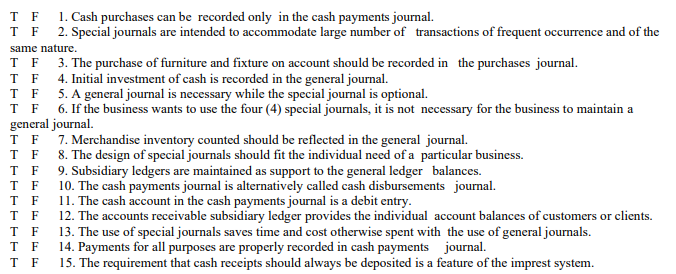

Transcribed Image Text:1. Cash purchases can be recorded only in the cash payments journal.

2. Special journals are intended to accommodate large number of transactions of frequent occurrence and of the

T F

T F

same nature.

T F 3. The purchase of furniture and fixture on account should be recorded in the purchases journal.

F

4. Initial investment of cash is recorded in the general journal.

T F 5. A general journal is necessary while the special journal is optional.

T F 6. If the business wants to use the four (4) special journals, it is not necessary for the business to maintain a

general journal.

T F

T F 8. The design of special journals should fit the individual need of a particular business.

T F 9. Subsidiary ledgers are maintained as support to the general ledger balances.

T F

T F

T F

7. Merchandise inventory counted should be reflected in the general journal.

10. The cash payments journal is alternatively called cash disbursements journal.

11. The cash account in the cash payments journal is a debit entry.

12. The accounts receivable subsidiary ledger provides the individual account balances of customers or clients.

13. The use of special journals saves time and cost otherwise spent with the use of general journals.

14. Payments for all purposes are properly recorded in cash payments journal.

15. The requirement that cash receipts should always be deposited is a feature of the imprest system.

T F

T F

T F

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution!

Trending now

This is a popular solution!

Step by step

Solved in 2 steps

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, accounting and related others by exploring similar questions and additional content below.Recommended textbooks for you

Financial Accounting

Accounting

ISBN:

9781305088436

Author:

Carl Warren, Jim Reeve, Jonathan Duchac

Publisher:

Cengage Learning

Century 21 Accounting Multicolumn Journal

Accounting

ISBN:

9781337679503

Author:

Gilbertson

Publisher:

Cengage

Financial Accounting

Accounting

ISBN:

9781305088436

Author:

Carl Warren, Jim Reeve, Jonathan Duchac

Publisher:

Cengage Learning

Century 21 Accounting Multicolumn Journal

Accounting

ISBN:

9781337679503

Author:

Gilbertson

Publisher:

Cengage

College Accounting, Chapters 1-27

Accounting

ISBN:

9781337794756

Author:

HEINTZ, James A.

Publisher:

Cengage Learning,

Principles of Accounting Volume 1

Accounting

ISBN:

9781947172685

Author:

OpenStax

Publisher:

OpenStax College