1. Under the perpetual inventory system, in addition to making the entry to record a sales return, a company would a. make no additional entry until the end of the period. b. debit Cost of Goods Sold and credit Purchases. c. debit Cost of Goods Sold and credit Merchandise Inventory. d. debit Merchandise Inventory and credit Cost of Goods Sold.

1. Under the perpetual inventory system, in addition to making the entry to record a sales return, a company would a. make no additional entry until the end of the period. b. debit Cost of Goods Sold and credit Purchases. c. debit Cost of Goods Sold and credit Merchandise Inventory. d. debit Merchandise Inventory and credit Cost of Goods Sold.

Accounting Information Systems

11th Edition

ISBN:9781337552127

Author:Ulric J. Gelinas, Richard B. Dull, Patrick Wheeler, Mary Callahan Hill

Publisher:Ulric J. Gelinas, Richard B. Dull, Patrick Wheeler, Mary Callahan Hill

Chapter13: The Accounts Payable/cash Disbursements (ap/cd) Process

Section: Chapter Questions

Problem 5P: Our narrative and DFDs are created assuming that accounts payable result from the purchase of...

Related questions

Question

100%

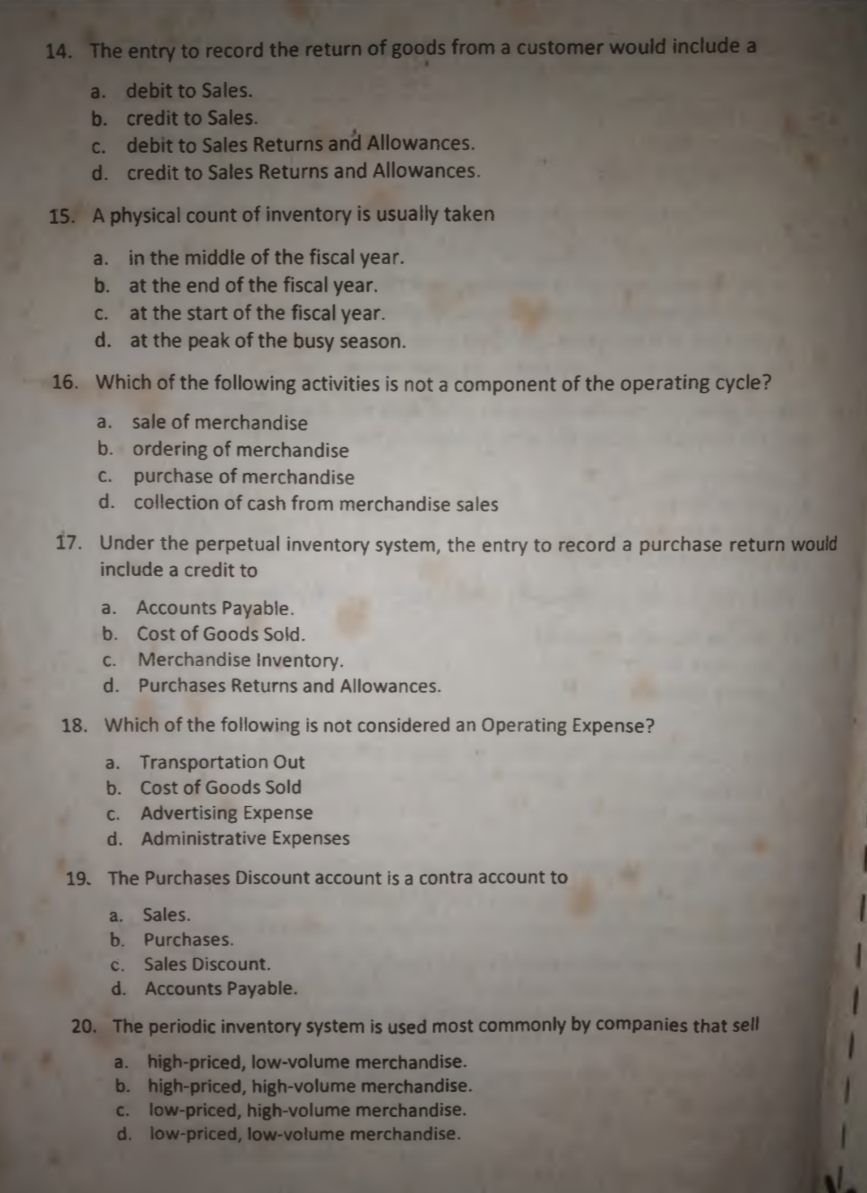

Transcribed Image Text:14. The entry to record the return of goods from a customer would include a

a. debit to Sales.

b. credit to Sales.

debit to Sales Returns and Allowances.

C.

d. credit to Sales Returns and Allowances.

15. A physical count of inventory is usually taken

a. in the middle of the fiscal year.

b. at the end of the fiscal year.

at the start of the fiscal year.

d. at the peak of the busy season.

с.

16. Which of the following activities is not a component of the operating cycle?

a. sale of merchandise

b. ordering of merchandise

c. purchase of merchandise

d. collection of cash from merchandise sales

17. Under the perpetual inventory system, the entry to record a purchase return would

include a credit to

a. Accounts Payable.

b. Cost of Goods Sold.

C. Merchandise Inventory.

d. Purchases Returns and Allowances.

18. Which of the following is not considered an Operating Expense?

a. Transportation Out

b. Cost of Goods Sold

c. Advertising Expense

d. Administrative Expenses

19. The Purchases Discount account is a contra account to

a.

Sales.

b. Purchases.

. Sales Discount.

d. Accounts Payable.

20. The periodic inventory system is used most commonly by companies that sell

a. high-priced, low-volume merchandise.

b. high-priced, high-volume merchandise.

c. low-priced, high-volume merchandise.

d. low-priced, low-volume merchandise.

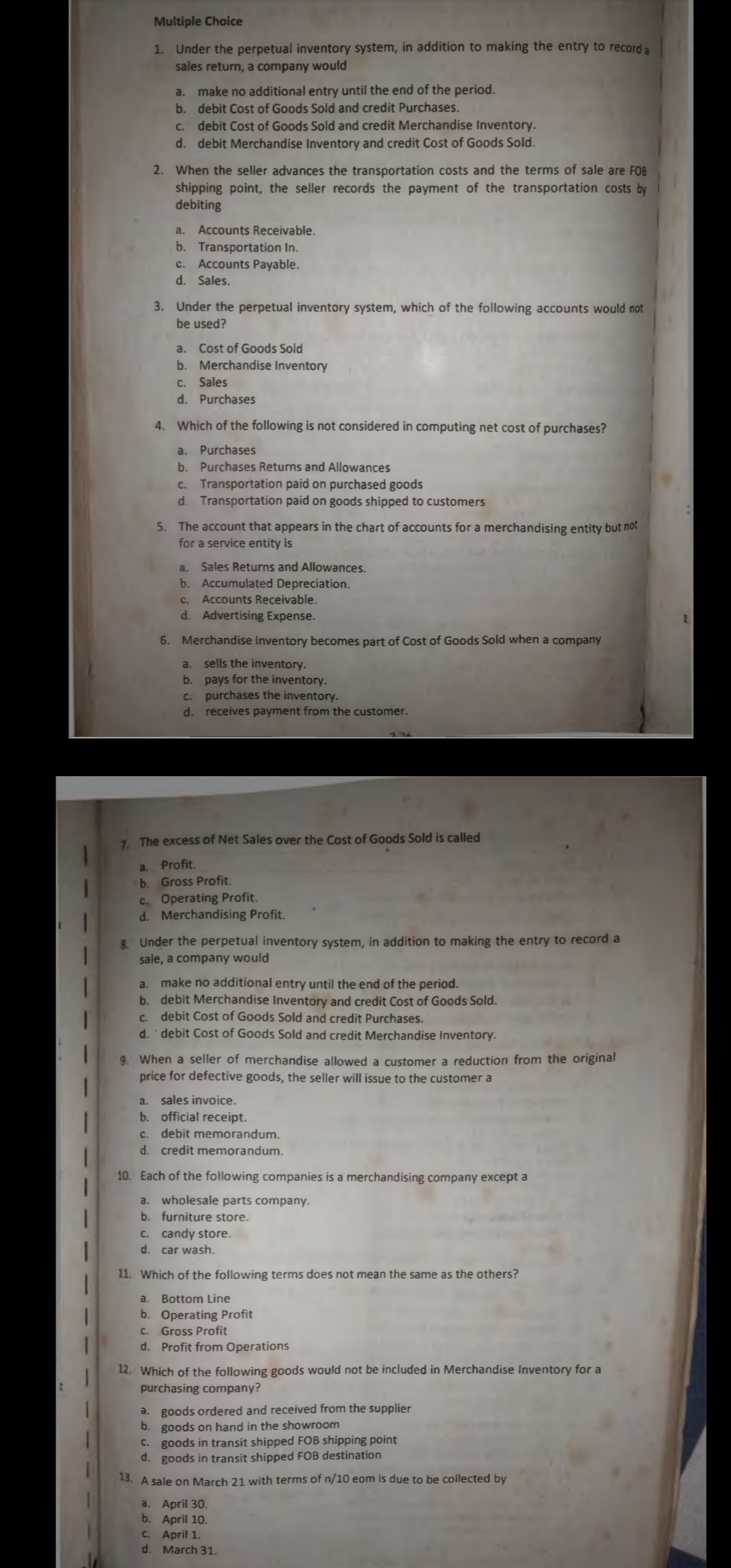

Transcribed Image Text:Multiple Choice

1. Under the perpetual inventory system, in addition to making the entry to record a

sales return, a company would

a. make no additional entry until the end of the period.

b. debit Cost of Goods Sold and credit Purchases.

c. debit Cost of Goods Sold and credit Merchandise Inventory.

d. debit Merchandise Inventory and credit Cost of Goods Sold.

2. When the seller advances the transportation costs and the terms of sale are FOB

shipping point, the seller records the payment of the transportation costs by

debiting

a. Accounts Receivable.

b. Transportation In.

c. Accounts Payable.

d. Sales.

3. Under the perpetual inventory system, which of the following accounts would not

be used?

a.

Cost of Goods Sold

b. Merchandise Inventory

C.

Sales

d. Purchases

4. Which of the following is not considered in computing net cost of purchases?

a. Purchases

b. Purchases Returns and Allowances

c. Transportation paid on purchased goods

d. Transportation paid on goods shipped to customers

5. The account that appears in the chart of accounts for a merchandising entity but not

for a service entity is

a. Sales Returns and Allowances.

b. Accumulated Depreciation.

c.

Accounts Receivable.

d. Advertising Expense.

6. Merchandise Inventory becomes part of Cost of Goods Sold when a company

sells the inventory.

b. pays for the inventory.

c. purchases the inventory.

d. receives payment from the customer.

a.

1. The excess of Net Sales over the Cost of Goods Sold is called

a. Profit.

b. Gross Profit.

c. Operating Profit.

d. Merchandising Profit.

& Under the perpetual inventory system, in addition to making the entry to record a

sale, a company would

make no additional entry until the end of the period.

b. debit Merchandise Inventory and credit Cost of Goods Sold.

debit Cost of Goods Sold and credit Purchases.

a.

C.

d. debit Cost of Goods Sold and credit Merchandise Inventory.

9. When a seller of merchandise allowed a customer a reduction from the original

price for defective goods, the seller will issue to the customer a

a. sales invoice.

b. official receipt.

c. debit memorandum.

d. credit memorandum.

10. Each of the following companies is a merchandising company except a

a. wholesale parts company.

b. furniture store.

c. candy store.

d. car wash.

11. Which of the following terms does not mean the same as the others?

a. Bottom Line

b. Operating Profit

Gross Profit

d. Profit from Operations

C.

12. Which of the following goods would not be included in Merchandise Inventory for a

purchasing company?

a. goods ordered and received from the supplier

b. goods on hand in the showroom

C. goods in transit shipped FOB shipping point

d. goods in transit shipped FOB destination

13.

A sale on March 21 with terms of n/10 eom is due to be collected by

a. April 30.

b. April 10.

C. April 1.

d. March 31.

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution!

Trending now

This is a popular solution!

Step by step

Solved in 3 steps

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, accounting and related others by exploring similar questions and additional content below.Recommended textbooks for you

Accounting Information Systems

Finance

ISBN:

9781337552127

Author:

Ulric J. Gelinas, Richard B. Dull, Patrick Wheeler, Mary Callahan Hill

Publisher:

Cengage Learning

Cornerstones of Financial Accounting

Accounting

ISBN:

9781337690881

Author:

Jay Rich, Jeff Jones

Publisher:

Cengage Learning

Intermediate Accounting: Reporting And Analysis

Accounting

ISBN:

9781337788281

Author:

James M. Wahlen, Jefferson P. Jones, Donald Pagach

Publisher:

Cengage Learning

Accounting Information Systems

Finance

ISBN:

9781337552127

Author:

Ulric J. Gelinas, Richard B. Dull, Patrick Wheeler, Mary Callahan Hill

Publisher:

Cengage Learning

Cornerstones of Financial Accounting

Accounting

ISBN:

9781337690881

Author:

Jay Rich, Jeff Jones

Publisher:

Cengage Learning

Intermediate Accounting: Reporting And Analysis

Accounting

ISBN:

9781337788281

Author:

James M. Wahlen, Jefferson P. Jones, Donald Pagach

Publisher:

Cengage Learning

Financial And Managerial Accounting

Accounting

ISBN:

9781337902663

Author:

WARREN, Carl S.

Publisher:

Cengage Learning,

Principles of Accounting Volume 1

Accounting

ISBN:

9781947172685

Author:

OpenStax

Publisher:

OpenStax College

Financial Accounting

Accounting

ISBN:

9781337272124

Author:

Carl Warren, James M. Reeve, Jonathan Duchac

Publisher:

Cengage Learning