16. At 95% confidence ( 0.05), determine which variables are significant and which are not. a. Both Shares Sold and NYSE Exchange are significant. b. Both Shares sold and NYSE Exchange are insignificant. Shares sold is significant and NYSE Exchange is insignificant. d. с. Shares sold is insignificant and NYSE Exchange is significant.

16. At 95% confidence ( 0.05), determine which variables are significant and which are not. a. Both Shares Sold and NYSE Exchange are significant. b. Both Shares sold and NYSE Exchange are insignificant. Shares sold is significant and NYSE Exchange is insignificant. d. с. Shares sold is insignificant and NYSE Exchange is significant.

Glencoe Algebra 1, Student Edition, 9780079039897, 0079039898, 2018

18th Edition

ISBN:9780079039897

Author:Carter

Publisher:Carter

Chapter10: Statistics

Section10.6: Summarizing Categorical Data

Problem 27PPS

Related questions

Question

Transcribed Image Text:16. At 95% confidence (a 0.05), determine which variables are significant and which are not.

Both Shares Sold and NYSE Exchange are significant.

b.

a.

Both Shares sold and NYSE Exchange are insignificant.

Shares sold is significant and NYSE Exchange is insignificant.

d.

с.

Shares sold is insignificant and NYSE Exchange is significant.

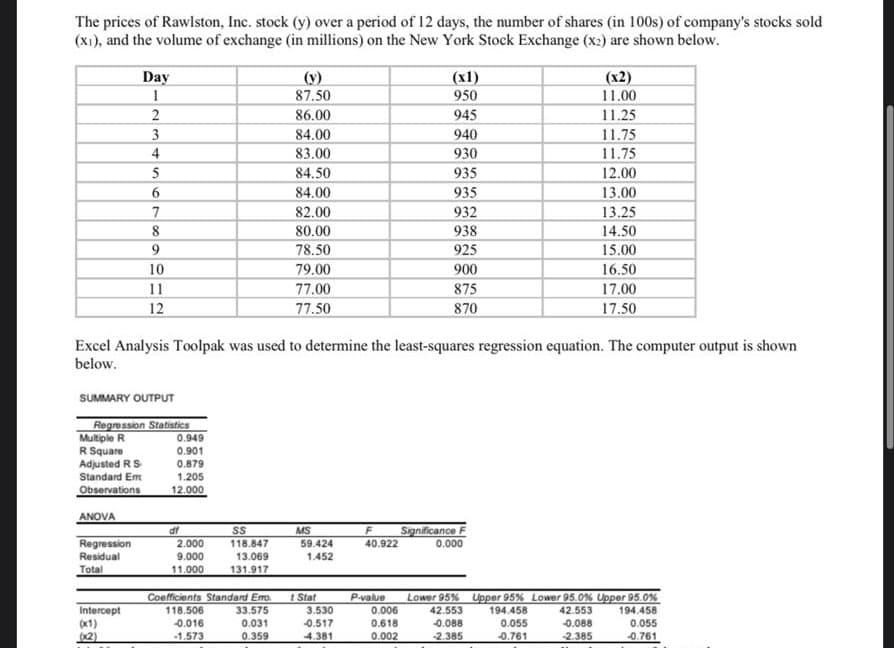

Transcribed Image Text:The prices of Rawlston, Inc. stock (y) over a period of 12 days, the number of shares (in 100s) of company's stocks sold

(x1), and the volume of exchange (in millions) on the New York Stock Exchange (x2) are shown below.

Day

(x1)

950

(x2)

(v)

87.50

11.00

2

86.00

945

11.25

3

84.00

940

11.75

11.75

4

83.00

930

5

84.50

935

12.00

6.

84.00

935

13.00

13.25

7

82.00

932

8

80.00

938

14.50

78.50

925

15.00

10

79.00

900

16.50

77.00

77.50

11

875

17.00

12

870

17.50

Excel Analysis Toolpak was used to determine the least-squares regression equation. The computer output is shown

below.

SUMMARY OUTPUT

Regression Statistics

Multiple R

R Square

0.949

0.901

Adjusted RS

Standard Em

Observations

0.879

1.205

12.000

ANOVA

df

MS

59.424

Significance F

SS

Regression

2.000

118.847

40.922

0.000

Residual

9.000

13.069

1.452

Total

11.000

131.917

Coefficients Standard Ero

118.506

0.016

33.575

0.031

t Stat

3.530

P-value

0.006

Lower 95% Upper 95% Lower 95.0% Upper 95.0%

194.458

194.458

Intercept

(x1)

(2)

42.553

42.553

-0.517

0.618

0.088

0.055

0.088

0.055

-1.573

0.359

4.381

0.002

-2.385

-0.761

2.385

-0.761

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

Step by step

Solved in 2 steps

Recommended textbooks for you

Glencoe Algebra 1, Student Edition, 9780079039897…

Algebra

ISBN:

9780079039897

Author:

Carter

Publisher:

McGraw Hill

Glencoe Algebra 1, Student Edition, 9780079039897…

Algebra

ISBN:

9780079039897

Author:

Carter

Publisher:

McGraw Hill