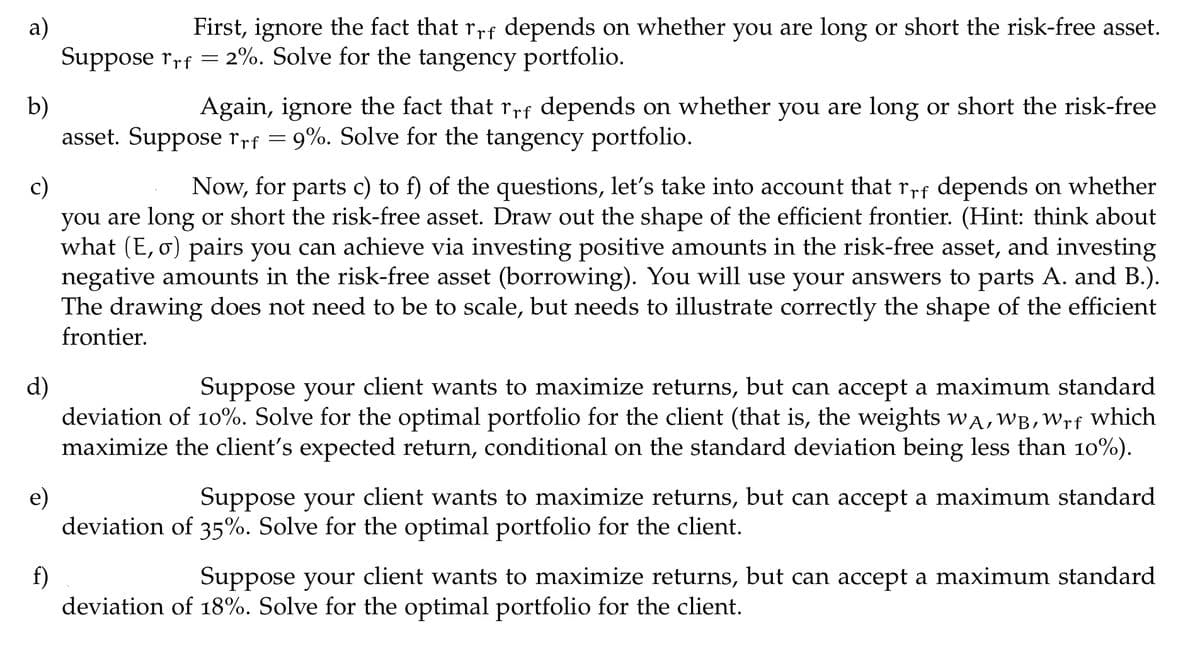

a) First, ignore the fact that rrf depends on whether you are long or short the risk-free asset. Suppose Trf = 2%. Solve for the tangency portfolio. b) Again, ignore the fact that rrf depends on whether you are long or short the risk-free asset. Suppose Trf = 9%. Solve for the tangency portfolio. c) Now, for parts c) to f) of the questions, let's take into account that rrf depends on whether you are long or short the risk-free asset. Draw out the shape of the efficient frontier. (Hint: think about what (E, o) pairs you can achieve via investing positive amounts in the risk-free asset, and investing negative amounts in the risk-free asset (borrowing). You will use your answers to parts A. and B.). The drawing does not need to be to scale, but needs to illustrate correctly the shape of the efficient frontier.

a) First, ignore the fact that rrf depends on whether you are long or short the risk-free asset. Suppose Trf = 2%. Solve for the tangency portfolio. b) Again, ignore the fact that rrf depends on whether you are long or short the risk-free asset. Suppose Trf = 9%. Solve for the tangency portfolio. c) Now, for parts c) to f) of the questions, let's take into account that rrf depends on whether you are long or short the risk-free asset. Draw out the shape of the efficient frontier. (Hint: think about what (E, o) pairs you can achieve via investing positive amounts in the risk-free asset, and investing negative amounts in the risk-free asset (borrowing). You will use your answers to parts A. and B.). The drawing does not need to be to scale, but needs to illustrate correctly the shape of the efficient frontier.

Chapter8: Analysis Of Risk And Return

Section: Chapter Questions

Problem 13QTD

Related questions

Question

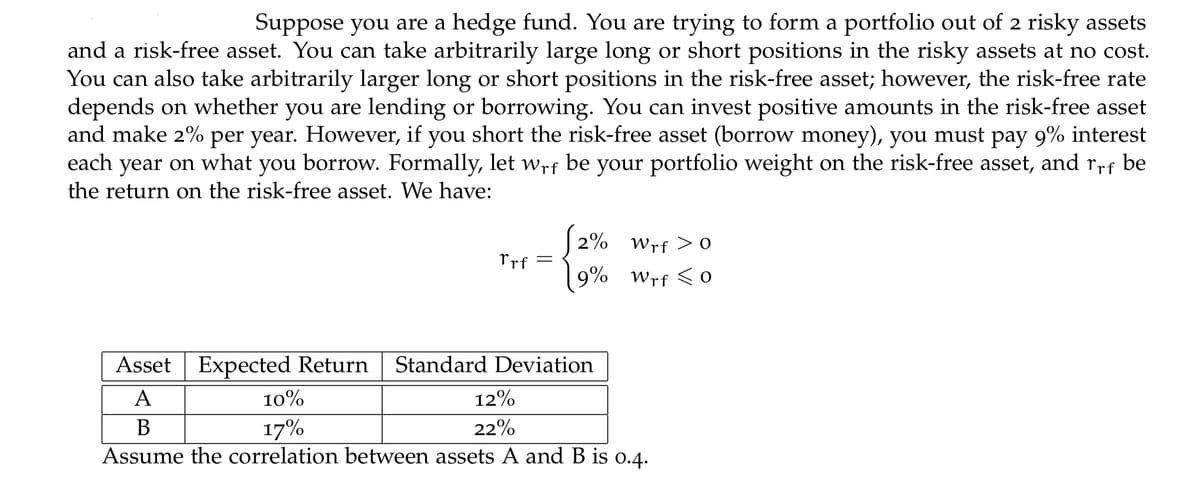

Transcribed Image Text:Suppose you are a hedge fund. You are trying to form a portfolio out of 2 risky assets

and a risk-free asset. You can take arbitrarily large long or short positions in the risky assets at no cost.

You can also take arbitrarily larger long or short positions in the risk-free asset; however, the risk-free rate

depends on whether you are lending or borrowing. You can invest positive amounts in the risk-free asset

and make 2% per year. However, if you short the risk-free asset (borrow money), you must pay 9% interest

each year on what you borrow. Formally, let wrf be your portfolio weight on the risk-free asset, and rrf be

the return on the risk-free asset. We have:

2% Wrf > 0

Prf

9% Wrf <0

Asset Expected Return

Standard Deviation

A

10%

12%

В

17%

22%

Assume the correlation between assets A and B is 0.4.

Transcribed Image Text:a)

First, ignore the fact that r,rf depends on whether you are long or short the risk-free asset.

Suppose rrf = 2%. Solve for the tangency portfolio.

b)

asset. Suppose rrf = 9%. Solve for the tangency portfolio.

Again, ignore the fact that rrf depends on whether you are long or short the risk-free

Now, for parts c) to f) of the questions, let's take into account that rrf depends on whether

c)

you are long or short the risk-free asset. Draw out the shape of the efficient frontier. (Hint: think about

what (E, o) pairs you can achieve via investing positive amounts in the risk-free asset, and investing

negative amounts in the risk-free asset (borrowing). You will use your answers to parts A. and B.).

The drawing does not need to be to scale, but needs to illustrate correctly the shape of the efficient

frontier.

d)

deviation of 10%. Solve for the optimal portfolio for the client (that is, the weights wA, WB,Wrf which

maximize the client's expected return, conditional on the standard deviation being less than 10%).

Suppose your client wants to maximize returns, but can accept a maximum standard

e)

deviation of 35%. Solve for the optimal portfolio for the client.

Suppose your client wants to maximize returns, but can accept a maximum standard

f)

deviation of 18%. Solve for the optimal portfolio for the client.

Suppose your client wants to maximize returns, but can accept a maximum standard

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

Step by step

Solved in 7 steps with 6 images

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, finance and related others by exploring similar questions and additional content below.Recommended textbooks for you

EBK CONTEMPORARY FINANCIAL MANAGEMENT

Finance

ISBN:

9781337514835

Author:

MOYER

Publisher:

CENGAGE LEARNING - CONSIGNMENT

EBK CONTEMPORARY FINANCIAL MANAGEMENT

Finance

ISBN:

9781337514835

Author:

MOYER

Publisher:

CENGAGE LEARNING - CONSIGNMENT