a) Historical nominal returns for Coca-Cola have been 8% and -20%. The nominal returns for the market index S&P500 over the same periods were -15% and 28%. Calculate the beta for Coca-cola. b) The covariance between stocks A and B is 0.0014, standard deviation of stock A is 0.032, and standard deviation of stock B is 0.044. Which of the following is the most appropriate to depict the risk-return characteristics of a portfolio consisting of only stocks A and B, and explain why? E(R) E(R) E(R) B B A A A (A) (B) (C) c) Assume that using the Security Market Line (SML) the required rate of return (Ra) on stock A is found to be half of the required return (RB) on stock B. The risk-free rate (R:) is one-fourth of the required return on A. Return on market portfolio is denoted by Rm. Find the ratio of beta of A (Ba) to beta of B (Вв). d) Assume that the short-term risk-free rate is 3%, the market index S&P500 is expected to pay returns of 15% with the standard deviation equal to 20%. Asset A pays on average 5%, has standard deviation equal to 20% and is NOT correlated with the S&P500. Asset B pays on average 8%, also has standard deviation equal to 20% and has correlation of 0.5 with the S&P500. Determine whether asset A and B are overvalued or undervalued, and explain why.

a) Historical nominal returns for Coca-Cola have been 8% and -20%. The nominal returns for the market index S&P500 over the same periods were -15% and 28%. Calculate the beta for Coca-cola. b) The covariance between stocks A and B is 0.0014, standard deviation of stock A is 0.032, and standard deviation of stock B is 0.044. Which of the following is the most appropriate to depict the risk-return characteristics of a portfolio consisting of only stocks A and B, and explain why? E(R) E(R) E(R) B B A A A (A) (B) (C) c) Assume that using the Security Market Line (SML) the required rate of return (Ra) on stock A is found to be half of the required return (RB) on stock B. The risk-free rate (R:) is one-fourth of the required return on A. Return on market portfolio is denoted by Rm. Find the ratio of beta of A (Ba) to beta of B (Вв). d) Assume that the short-term risk-free rate is 3%, the market index S&P500 is expected to pay returns of 15% with the standard deviation equal to 20%. Asset A pays on average 5%, has standard deviation equal to 20% and is NOT correlated with the S&P500. Asset B pays on average 8%, also has standard deviation equal to 20% and has correlation of 0.5 with the S&P500. Determine whether asset A and B are overvalued or undervalued, and explain why.

Chapter8: Analysis Of Risk And Return

Section: Chapter Questions

Problem 15P

Related questions

Question

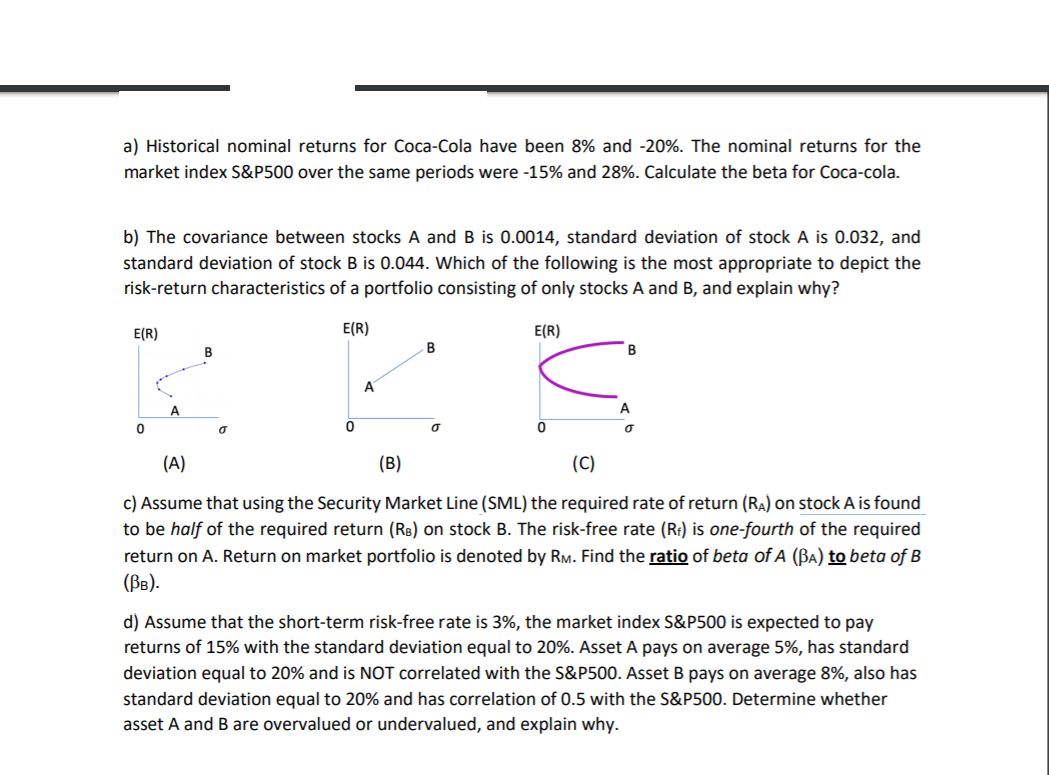

Transcribed Image Text:a) Historical nominal returns for Coca-Cola have been 8% and -20%. The nominal returns for the

market index S&P500 over the same periods were -15% and 28%. Calculate the beta for Coca-cola.

b) The covariance between stocks A and B is 0.0014, standard deviation of stock A is 0.032, and

standard deviation of stock B is 0.044. Which of the following is the most appropriate to depict the

risk-return characteristics of a portfolio consisting of only stocks A and B, and explain why?

E(R)

E(R)

E(R)

B

B

A

A

A

(A)

(B)

(C)

c) Assume that using the Security Market Line (SML) the required rate of return (Ra) on stock A is found

to be half of the required return (RB) on stock B. The risk-free rate (R:) is one-fourth of the required

return on A. Return on market portfolio is denoted by Rm. Find the ratio of beta of A (Ba) to beta of B

(Вв).

d) Assume that the short-term risk-free rate is 3%, the market index S&P500 is expected to pay

returns of 15% with the standard deviation equal to 20%. Asset A pays on average 5%, has standard

deviation equal to 20% and is NOT correlated with the S&P500. Asset B pays on average 8%, also has

standard deviation equal to 20% and has correlation of 0.5 with the S&P500. Determine whether

asset A and B are overvalued or undervalued, and explain why.

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

Step by step

Solved in 2 steps

Recommended textbooks for you

EBK CONTEMPORARY FINANCIAL MANAGEMENT

Finance

ISBN:

9781337514835

Author:

MOYER

Publisher:

CENGAGE LEARNING - CONSIGNMENT

Managerial Accounting

Accounting

ISBN:

9781337912020

Author:

Carl Warren, Ph.d. Cma William B. Tayler

Publisher:

South-Western College Pub

Intermediate Financial Management (MindTap Course…

Finance

ISBN:

9781337395083

Author:

Eugene F. Brigham, Phillip R. Daves

Publisher:

Cengage Learning

EBK CONTEMPORARY FINANCIAL MANAGEMENT

Finance

ISBN:

9781337514835

Author:

MOYER

Publisher:

CENGAGE LEARNING - CONSIGNMENT

Managerial Accounting

Accounting

ISBN:

9781337912020

Author:

Carl Warren, Ph.d. Cma William B. Tayler

Publisher:

South-Western College Pub

Intermediate Financial Management (MindTap Course…

Finance

ISBN:

9781337395083

Author:

Eugene F. Brigham, Phillip R. Daves

Publisher:

Cengage Learning