A project's internal rate of return (IRR) is the that forces the PV of the expected future cash flows to equal the initial cash flow. The IRR is an estimate of the project's rate of return, and it is comparable to the on a bond. The equation for calculating the IRR is: CFt is the expected cash flow in Period t and cash outflows are treated as negative cash flows. There must be a change in cash flow signs to calculate the IRR. The IRR equation is simply the NPV equation solved for the particular discount rate that causes NPV to equal . The IRR calculation assumes that cash flows are reinvested at the . If the IRR is than the project's cost of capital, then the project should be accepted; however, if the IRR is less than the project's cost of capital, then the project should be . Because of the IRR reinvestment rate assumption, when projects are evaluated the IRR approach can lead to conflicting results from the NPV method. Two basic conditions can lead to conflicts between NPV and IRR: differences (earlier cash flows in one project vs. later cash flows in the other project) and project size (the cost of one project is larger than the other). When mutually exclusive projects are considered, then the method should be used to evaluate projects. Quantitative Problem: Bellinger Industries is considering two projects for inclusion in its capital budget, and you have been asked to do the analysis. Both projects' after-tax cash flows are shown on the time line below. Depreciation, salvage values, net operating working capital requirements, and tax effects are all included in these cash flows. Both projects have 4-year lives, and they have risk characteristics similar to the firm's average project. Bellinger's WACC is 11%. 0 1 2 3 4 Project A -1,250 730 360 270 315 Project B -1,250 330 295 420 765 What is Project A’s IRR? Do not round intermediate calculations. Round your answer to two decimal places. % What is Project B's IRR? Do not round intermediate calculations. Round your answer to two decimal places. % If the projects were independent, which project(s) would be accepted according to the IRR method? would be accepted. If the projects were mutually exclusive, which project(s) would be accepted according to the IRR method? would be accepted. Could there be a conflict with project acceptance between the NPV and IRR approaches when projects are mutually exclusive? The reason is the NPV and IRR approaches use when mutually exclusive projects are considered. Reinvestment at the is the superior assumption, so when mutually exclusive projects are evaluated the approach should be used for the capital budgeting decision.

The Basics of Capital Budgeting: Evaluating Cash Flows: IRR

A project's

CFt is the expected cash flow in Period t and

The IRR calculation assumes that cash flows are reinvested at the . If the IRR is than the project's cost of capital, then the project should be accepted; however, if the IRR is less than the project's cost of capital, then the project should be . Because of the IRR reinvestment rate assumption, when projects are evaluated the IRR approach can lead to conflicting results from the NPV method. Two basic conditions can lead to conflicts between NPV and IRR: differences (earlier cash flows in one project vs. later cash flows in the other project) and project size (the cost of one project is larger than the other). When mutually exclusive projects are considered, then the method should be used to evaluate projects.

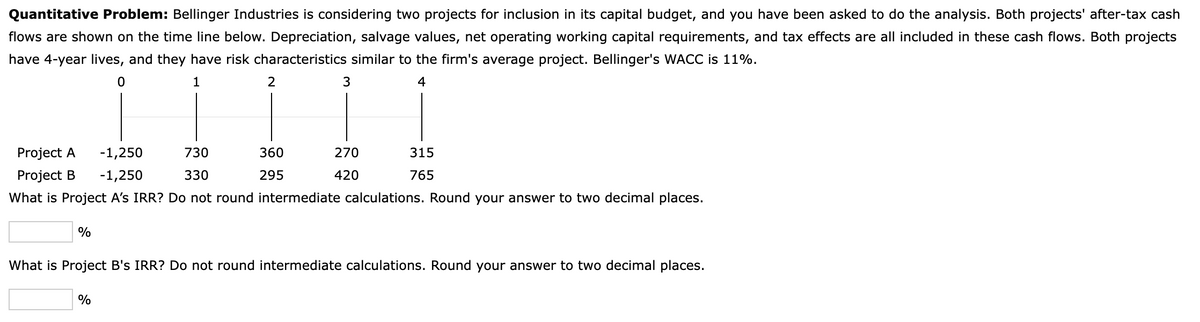

Quantitative Problem: Bellinger Industries is considering two projects for inclusion in its capital budget, and you have been asked to do the analysis. Both projects' after-tax cash flows are shown on the time line below.

| 0 | 1 | 2 | 3 | 4 | ||||||

| Project A | -1,250 | 730 | 360 | 270 | 315 | |||||

| Project B | -1,250 | 330 | 295 | 420 | 765 |

What is Project A’s IRR? Do not round intermediate calculations. Round your answer to two decimal places.

%

What is Project B's IRR? Do not round intermediate calculations. Round your answer to two decimal places.

%

If the projects were independent, which project(s) would be accepted according to the IRR method?

would be accepted.

If the projects were mutually exclusive, which project(s) would be accepted according to the IRR method?

would be accepted.

Could there be a conflict with project acceptance between the NPV and IRR approaches when projects are mutually exclusive?

The reason is the NPV and IRR approaches use when mutually exclusive projects are considered.

Reinvestment at the is the superior assumption, so when mutually exclusive projects are evaluated the approach should be used for the capital budgeting decision.

Trending now

This is a popular solution!

Step by step

Solved in 3 steps with 2 images