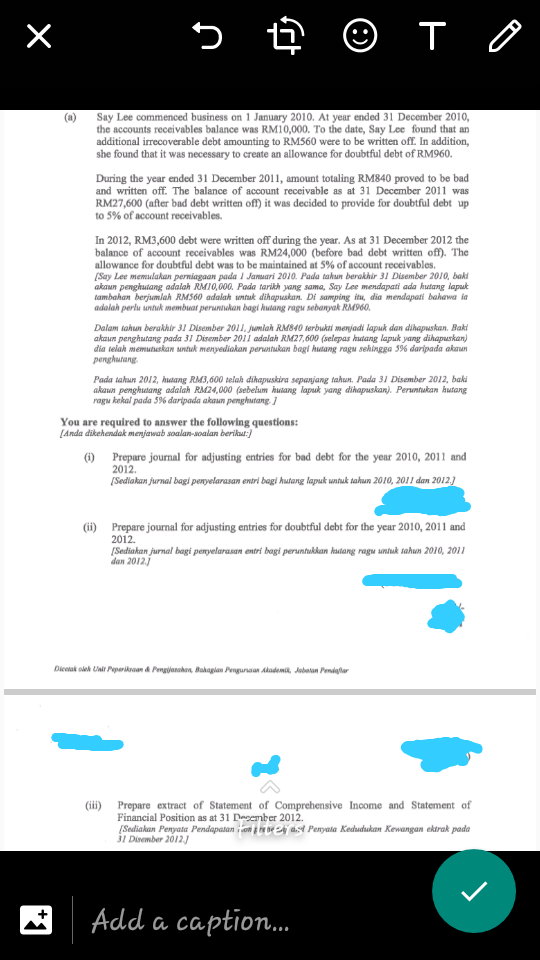

(a) Say Lee commenced business on 1 January 2010. At year ended 31 December 2010, the accounts receivables balance was RM10,000. To the date, Say Lee found that an additional irrecoverable debt amounting to RM560 were to be written off. In addition, she found that it was necessary to create an allowance for doubtful debt of RM960. During the year ended 31 December 2011, amount totaling RM840 proved to be bad and written off. The balance of account receivable as at 31 December 2011 was RM27,600 (after bad debt written off) it was decided to provide for doubtful debt up to 5% of account receivables. In 2012, RM3,600 debt were written off during the year. As at 31 December 2012 the balance of account receivables was RM24,000 (before bad debt written off). The allowance for doubtful debt was to be maintained at 5% of account receivables. [Say Lee memulakan perniagaan pada 1 Jamuari 2010. Pada takun berakhir 31 Disember 2010, baki akaun pengkudang adalah RMI0,000. Pada tarikh yang sama, Say Lee mendapati ada hutang laput iambahan berjumlah RM560 adalah ntak dihapuskan. Di samping in dia mendapati bahawa ie adalah perlu untuk membuat peruntukan bagi hutang ragu sebanyak RM960. Dalam tahun berakhir 31 Disember 2011, jumlah RM840 terbukzi menjadi lapuk dan dihapuskan. Baki akaun penghutang pada 31 Disember 201i adalah RM27,600 (selepas hadang lapuk yang dihapurkan) dia telah memutuskan sentuk menyediakan peruntukan bagi hutang ragu sehingga % daripada aknun penghutang Pada tahun 2012, hutang RM3,600 telak dihapuskira sepanjang takun. Pada 31 Disember 2012, baki akaun penghutang adalah RM24,000 (sebelam husang lapuuk yang dihapuskan). Perantukan kutang ragu kekal pada 5% daripada akaun penghutang ] You are required to answer the following questions: [Anda dikehendak menjawab soalan-soalan berikat:) O Prepare journal for adjusting entries for bad debt for the year 2010, 2011 and 2012. Sediakan jurnal bogi peryelarasan entri bagi hutang lapuk untak tahun 2010, 2011 dan 2012) (i) Prepare journal for adjusting entries for doubtful debt for the year 2010, 2011 and 2012. (Sediakan jurnal bagi penyelarasın entri bagi peruntukkan hadang ragu untuk sahun 2010, 2011 dan 2012j (ii) Prepare extract of Statement of Comprehensive Income and Statement of Financial Position as at 31 Deserber 2012. [Sadiakan Penyata Pendapatan in p a ve 2Á ast Penyata Kedudukan Kewangan ektrak pada 31 Dinember 2012.]

Bad Debts

At the end of the accounting period, a financial statement is prepared by every company, then at that time while preparing the financial statement, the company determines among its total receivable amount how much portion of receivables is collected by the company during that accounting period.

Accounts Receivable

The word “account receivable” means the payment is yet to be made for the work that is already done. Generally, each and every business sells its goods and services either in cash or in credit. So, when the goods are sold on credit account receivable arise which means the company is going to get the payment from its customer to whom the goods are sold on credit. Usually, the credit period may be for a very short period of time and in some rare cases it takes a year.

Step by step

Solved in 2 steps