A. At the beginning of current year, an entity provided the following information in connection with a defined benefit plan: Fair value of plan assets Projected benefit obligation Prepaid /accrued benefit cost 10,000,000 (13,000,000) (3,000,000) The entity revealed the following transactions affecting the plan for the current year: Current service cost 2,500,000 Past service cost - remaining vesting period of covered employees is 5 years Contribution to the plan Benefits paid to retirees Actual return on plan assets Decrease in projected benefit obligation due to change in actuarial assumptions 1,200,000 3,500,000 3,000,000 1,500,000 400,000 Discount rate 10% Expected return on plan assets 12%

A. At the beginning of current year, an entity provided the following information in connection with a defined benefit plan: Fair value of plan assets Projected benefit obligation Prepaid /accrued benefit cost 10,000,000 (13,000,000) (3,000,000) The entity revealed the following transactions affecting the plan for the current year: Current service cost 2,500,000 Past service cost - remaining vesting period of covered employees is 5 years Contribution to the plan Benefits paid to retirees Actual return on plan assets Decrease in projected benefit obligation due to change in actuarial assumptions 1,200,000 3,500,000 3,000,000 1,500,000 400,000 Discount rate 10% Expected return on plan assets 12%

Intermediate Accounting: Reporting And Analysis

3rd Edition

ISBN:9781337788281

Author:James M. Wahlen, Jefferson P. Jones, Donald Pagach

Publisher:James M. Wahlen, Jefferson P. Jones, Donald Pagach

Chapter19: Accounting For Post Retirement Benefits

Section: Chapter Questions

Problem 7RE

Related questions

Question

4. Compute the projected benefit obligation at year-end

see pic for the problem

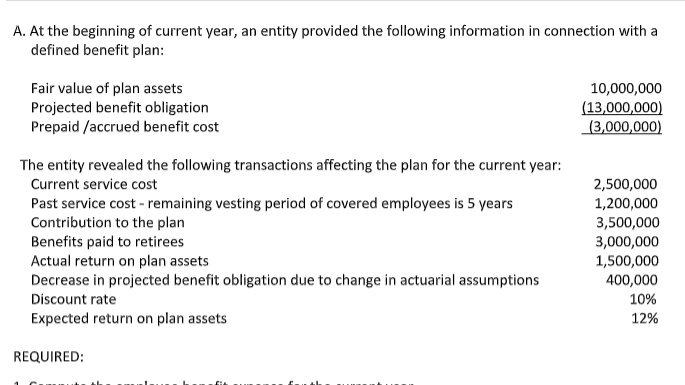

Transcribed Image Text:A. At the beginning of current year, an entity provided the following information in connection with a

defined benefit plan:

Fair value of plan assets

Projected benefit obligation

Prepaid /accrued benefit cost

10,000,000

(13,000,000)

(3,000,000)

The entity revealed the following transactions affecting the plan for the current year:

Current service cost

2,500,000

Past service cost - remaining vesting period of covered employees is 5 years

Contribution to the plan

Benefits paid to retirees

Actual return on plan assets

Decrease in projected benefit obligation due to change in actuarial assumptions

Discount rate

1,200,000

3,500,000

3,000,000

1,500,000

400,000

10%

Expected return on plan assets

12%

REQUIRED:

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

Step by step

Solved in 2 steps

Recommended textbooks for you

Intermediate Accounting: Reporting And Analysis

Accounting

ISBN:

9781337788281

Author:

James M. Wahlen, Jefferson P. Jones, Donald Pagach

Publisher:

Cengage Learning

Intermediate Accounting: Reporting And Analysis

Accounting

ISBN:

9781337788281

Author:

James M. Wahlen, Jefferson P. Jones, Donald Pagach

Publisher:

Cengage Learning

Individual Income Taxes

Accounting

ISBN:

9780357109731

Author:

Hoffman

Publisher:

CENGAGE LEARNING - CONSIGNMENT