An entity provided the following information for the current year:

Q: How is the accounting treatment of an event that occurred on the date before the report was…

A: Subsequent events are events occurring after balance sheet but before the issue of financial…

Q: Which sections of an annual report do IFRSs apply to? a) Management report b) Financial statements…

A: management report is used as a means of communicating whatever information that is essential to be…

Q: а. Record the appropriate journal entry on December 31, 20X1. b. Where on the financial statements…

A: Mark to market accounting is made to ensure that the financial statement consists of true amounts.…

Q: Explain the need for using coterminous year ends and uniform accounting policies in preparing…

A: The question is related to IFRS 10 Consolidated Financial Statements. The coterminous year means…

Q: Assuming the entity paid its employees their wages, incurred during the period. The proper debit to…

A: Nominal account have a rule of - Debiting all expenses and losses and crediting all incomes and…

Q: What are the steps to be taken in preparing IFRS financial statements for the first time?

A: IFRS: International Financial Reporting Standard is abbreviated as IFRS. The IFRS is set up to bring…

Q: The following transactions were completed by the company.

A: It is the equation that states that the total assets of an entity is equal to the sum of total…

Q: Are transactions recorded on a fiscal‐year basis or a calendar‐year basis? Does it have to be one or…

A: Fiscal year is a 12 months period, which normally starts from Apr 1 to Mar 31 of next year. Calendar…

Q: Revenue is recognized based on a five-step process that is applied to a company's revenue…

A: Five Step Revenue Process : Step 1 : Identification of the contract with the customer Step 2 :…

Q: The most important information about an entity generally shall be disclosed in a. Notes to the…

A: Financial statements shows the position of a company. Balance sheet, profit and loss statement ,…

Q: For accounting purposes, we classify accounting changes into three categories. What are they?…

A: Accounting changes: Accounting changes are the alternations made to the accounting methods,…

Q: Determine the list of the initial financial statements in accordance with IFRS.

A: IFRS means International Financial Reporting Standards Thers is list of the Initial Financial…

Q: TRUE or FALSE An entity can begin its operation in a calendar year or fiscal year.

A: The calendar year starts on January 1 and ends on December 31. but the fiscal year is a time period…

Q: An entity is preparing its financial statements for the first time in accordance with PFRS for SMEs…

A: Financial statements are the reports presenting the financial position and profitability of an…

Q: For each of the following subsequent events, indicate the impact to the financial statements

A: The impact of the subsequent events on the financial statement is classified as follows:- 1. The…

Q: An entity shall disclose for each reportable segment a measure of all of the following, except A.…

A: Answer; The reportable segment is the segment which reports the revenue that includes the…

Q: During the life-time of an entity accounting produce financial statements in accordance with which…

A: According to the accounting concept i.e. “Accounting Period”, In accordance with accounting period…

Q: The following statement An entity presents on a net basis gains and losses arising from a group of…

A: Answer is POINT 'C'

Q: Indicate how prior period adjustments should be reported on the financial statements presented only…

A: Prior Period Adjustments Prior period adjustments refer to the error that is caused due to any…

Q: An entity uses a calnedar period for is financial reporting. Its current financial statements are…

A: As per PFRS 10, Events after the reporting period are those events, that occur between the end of…

Q: related party transactions,

A: Option 1 is wrong because in case of related party transactions the business entity should disclose…

Q: Prepare journal entries to record the transactions for the current year.

A: Since yo have posted the question with multiple subpart, we will solve the first three subpart for…

Q: S1: Financial statements must be prepared by a publicly-listed entity at least semiannually. S2: An…

A: The financial statements are prepared by an entity in order to show the financial performance and…

Q: Which fundamental characteristic of requires that financial statements are prepared in a similar way…

A: option c is the correct answer.

Q: Explain briefly the items generally included in a compa-ny’s annual report. (You may use the…

A: Company Annual reports include the following: Income statement Balance sheet Cash flows statement…

Q: true or false according to PAS 1, PFRS apply to financial statements as well as to other…

A: Accounting principles are general rules and guidelines that the company follows while recording and…

Q: The following statements are based on PAS 34 – "Interim Financial Reporting": Interim financial…

A: The question is related to the PAS 34 Interim Financial Reporting. As per PAS 34 1. The minimum…

Q: act on the financial statements of previous years. Istatements of only previous years. 1 statements…

A: Prospective adjustments refer to all those adjustments that will be made from the date the changes…

Q: The primary objective of the matching principle is toa. Provide full disclosureb. Record expenses in…

A: Matching principle: According to this principle, the expense should be recognized when it is…

Q: [The following information applies to the questions displayed below Simon Company's yearend balance…

A: Debt Ratio = Total Debt/Total Assets Equity Ratio = Shareholder's Equity/Total assets

Q: Discuss the disclosure requirements for related-party transactions, post-balance-sheet events, major…

A: Segment reporting: Segment reporting refers to the process of preparing accounting report by segment…

Q: What are the three basic financial statements contained in a company's annual report?

A: The company's annual report is one of the most important resource of reliable and audited financial…

Q: there are general features that ias 1 require every entity that its financial statement

A: IAS 1 is an Indian Accounting Standard which guides for Presentation of Financial Statements.

Q: Describe the accounting for changes in estimates and changes in the reporting entity.

A: Accounting changes: When a company requires to sacrifice the consistent accounting methods and…

Q: e information, in its current state, be included in the current financial statements

A: The items are disclosed in the financial statements to increase the awareness of the users.

Q: nancial year stating up to.......

A: The financial year is the period during which money is earned. Salaried professionals and senior…

Q: The purpose of presenting comparative information in the transition to IFRS is: a. to ensure that…

A: International Financial Reporting Standards (IFRS) They are commonly known as IFRS. It is a set of…

Q: What are the steps that a company must follow in preparing its initial set of IFRS financial…

A: International Financial Reporting Standards (IFRS) They are commonly known as IFRS. It is a set of…

Q: What is the revenue to be recognized by Entity A for the year ended December 31, 2020?

A: Particulars Stand-alone amount Revenue Royalty $25000 Non-Refundable Fees: Construction…

Q: What type of business is most likely to select a fiscal year that corresponds to its natural…

A: Fiscal year is a period of 52 week used by the businesses for reporting purposes. It can be…

Q: On which financial statement are permanent accounts reported?

A: The company's aim will be to increase the profitability of the company. The profits can be arrived…

Q: The __________ is also referred to as the reporting date. Select one alternative: balance sheet…

A: Account means the systematic record of various transactions entered by businesses. Income statement…

Q: discuss the identification and accounting treatments of adjusting and non-adjusting events

A: International Accounting Standard (IAS) 10 has prescribed the adjustments for those events that…

Q: The balance of this account shows the net income or net loss for the period before it is closed to…

A: Solution: Balance of income summary account shows the net income or net loss for the period before…

Q: Identify and discuss the chronological steps of the accounting cycle and preparation of the…

A: The accounting is a process of identifying, classifying and recording the transactions of the…

Step by step

Solved in 2 steps with 1 images

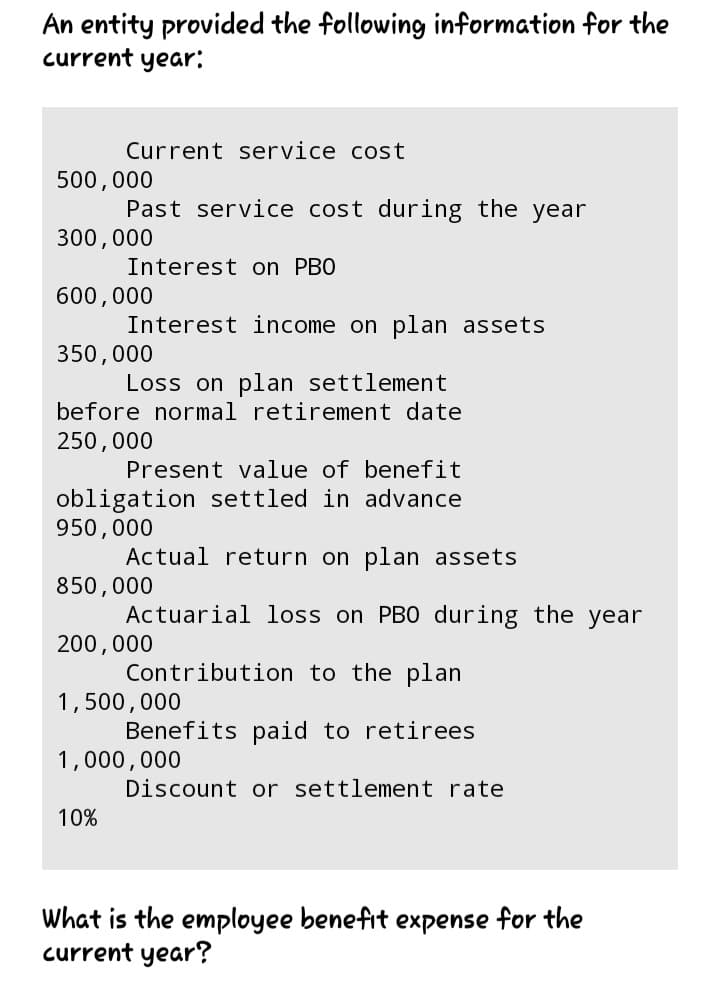

- William and Raj Company provided the following information for the year:Projected benefit obligation - January 1 P 700,000Fair value of plan assets - January 1 560,000Pension benefits paid during the year 50,000Current service cost for the year 350,000Past service cost for the year (vesting period 5 years) 85,000Actual return on plan assets 36,000Contributions to the plan 300,000Actuarial loss due to change in assumptions on projected benefit obligation 40,000Discount or settlement rate 10%Expected return on plan assets 12%1. What is the employee benefit expense for the current year?2. How much is the actuarial gain/loss on return on plan assets?3. What is the prepaid/accrued balance of the pension at yearend?4. How much is the defined benefit cost?5. If the pension benefits paid during the year is worth P50,000 but the company was able to pay only P45,000, what would be the employee benefitexpense for the current year assuming the above given is the same?SJ Company provided the following information for the current year. •Current service cost - 500,000 •Interest expense on PBO - 600,000 •Interest income on plan assets - 350,000 •Loss on plan settlement before normal retirement date - 250,000 •Present value of benefit obligation settled in advance - 950,000 •Past service cost during the year - 300,000 •Actual return on plan assets - 850,000 •Actuarial loss on PBO during the year - 200,000 •Contribution to the plan - 1,500,000 •Benefits paid to retirees - 1,000,000 •Discount or settlement rate - 10% What is the net remeasurement for the current year? a. 500,000 gain b.200,000 loss c.300,000 gain d.300,000 lossInformation on Complicated Company's defined benefit plan is as follows: Fair value of plan assets, Jan. 1 - P480,000; Return on plan assets (Actual rate of return for the period) - 10%; Contributions to the retirement fund during the year - P800,000; Benefits paid to retirees - P200,000. How much is the balance of the fair value of plan assets as of year-end?

- An entity provided the following information during the current year:January 1 December 31Fair value of plan assets 6,000,000 9,000,000Projected benefit obligation 4,500,000 5,000,000Prepaid/accrued benefit cost – surplus 1,500,000 4,000,000Asset ceiling 1,000,000 2,500,000Effect of asset ceiling 500,000 1,500,000During the year, the entity recognized current service cost P2,000,000, actual return on plan assets P400,000,and contribution to the plan P4,550,000 and benefits paid P1,950,000. The discount rate is 10%REQUIRED: . Compute the defined benefit costFair value of plan assets 4,750,000Unamortized past service cost 1,250,000Projected benefit obligation 5,500,000Unrecognized actuarial gain 850,000The transactions for the current year relating to the defined benefit plan are as follows:Current service cost 925,000Discount rate 6%Actual return on plan assets 485,000Contribution to the plan 1,350,000Benefits paid to retirees 995,000Increase in projected benefit obligation due to changes in actuarial assumptions 150,000Effective in the current year, the entity has applied the provisions of revised PAS 19 in relation to the definedbenefit plan.REQUIRED:15. Prepare journal entry to recognize the transitional effect of adopting revised PAS 19.16. Determine the employee benefit expense for the current year.17. Compute the remeasurement related to the defined benefit plan.18. Prepare journal entry to record the employee benefit expense.19. Compute for the Fair Value Plan Asset (FVPA) as of December 31.20. Compute for the projected benefit…A. At the beginning of current year, an entity provided the following information in connection with adefined benefit plan: Fair value of plan assets 10,000,000Projected benefit obligation (13,000,000)Prepaid /accrued benefit cost (3,000,000) The entity revealed the following transactions affecting the plan for the current year: Current service cost 2,500,000Past service cost - remaining vesting period of covered employees is 5 years 1,200,000Contribution to the plan 3,500,000Benefits paid to retirees 3,000,000Actual return on plan assets 1,500,000 Decrease in projected benefit obligation due to change in actuarial assumptions 400,000Discount rate 10%Expected return on plan assets 12% Compute the projected benefit obligation at year-end What amount should be reported as accrued or prepaid benefit cost at year-end

- A. At the beginning of current year, an entity provided the following information in connection with adefined benefit plan:Fair value of plan assets 10,000,000Projected benefit obligation (13,000,000)Prepaid /accrued benefit cost (3,000,000)The entity revealed the following transactions affecting the plan for the current year:Current service cost 2,500,000Past service cost - remaining vesting period of covered employees is 5 years 1,200,000Contribution to the plan 3,500,000Benefits paid to retirees 3,000,000Actual return on plan assets 1,500,000Decrease in projected benefit obligation due to change in actuarial assumptions 400,000Discount rate 10%Expected return on plan assets 12%REQUIRED:1. Compute the employee benefit expense for the current year 2. Compute the net remeasurement gain for the current year3. Compute the fair value of plan assets at year-end4. Compute the projected benefit obligation at year-end5. What amount should be reported as accrued or prepaid benefit cost at…E. Charlton Company provided the following information concerning a defined benefit plan at the beginning ofcurrent year prior to the adoption of revised PAS 19:Debit CreditFair value of plan assets 4,750,000Unamortized past service cost 1,250,000Projected benefit obligation 5,500,000Unrecognized actuarial gain 850,000The transactions for the current year relating to the defined benefit plan are as follows:Current service cost 925,000Discount rate 6%Actual return on plan assets 485,000Contribution to the plan 1,350,000Benefits paid to retirees 995,000Increase in projected benefit obligation due to changes in actuarial assumptions 150,000Effective in the current year, the entity has applied the provisions of revised PAS 19 in relation to the definedbenefit plan.REQUIRED: 17. Compute the remeasurement related to the defined benefit plan.E. Charlton Company provided the following information concerning a defined benefit plan at the beginning ofcurrent year prior to the adoption of revised PAS 19:Debit CreditFair value of plan assets 4,750,000Unamortized past service cost 1,250,000Projected benefit obligation 5,500,000Unrecognized actuarial gain 850,000The transactions for the current year relating to the defined benefit plan are as follows:Current service cost 925,000Discount rate 6%Actual return on plan assets 485,000Contribution to the plan 1,350,000Benefits paid to retirees 995,000Increase in projected benefit obligation due to changes in actuarial assumptions 150,000Effective in the current year, the entity has applied the provisions of revised PAS 19 in relation to the definedbenefit plan.REQUIRED: 19. Compute for the Fair Value Plan Asset (FVPA) as of December 31.

- E. Charlton Company provided the following information concerning a defined benefit plan at the beginning ofcurrent year prior to the adoption of revised PAS 19:Debit CreditFair value of plan assets 4,750,000Unamortized past service cost 1,250,000Projected benefit obligation 5,500,000Unrecognized actuarial gain 850,000The transactions for the current year relating to the defined benefit plan are as follows:Current service cost 925,000Discount rate 6%Actual return on plan assets 485,000Contribution to the plan 1,350,000Benefits paid to retirees 995,000Increase in projected benefit obligation due to changes in actuarial assumptions 150,000Effective in the current year, the entity has applied the provisions of revised PAS 19 in relation to the definedbenefit plan. Compute the remeasurement related to the defined benefit plan.E. Charlton Company provided the following information concerning a defined benefit plan at the beginning ofcurrent year prior to the adoption of revised PAS 19:Debit CreditFair value of plan assets 4,750,000Unamortized past service cost 1,250,000Projected benefit obligation 5,500,000Unrecognized actuarial gain 850,000The transactions for the current year relating to the defined benefit plan are as follows:Current service cost 925,000Discount rate 6%Actual return on plan assets 485,000Contribution to the plan 1,350,000Benefits paid to retirees 995,000Increase in projected benefit obligation due to changes in actuarial assumptions 150,000Effective in the current year, the entity has applied the provisions of revised PAS 19 in relation to the definedbenefit plan.REQUIRED: 16. Determine the employee benefit expense for the current year.At the beginning of the current year, the memorandum records of Fischl Company’s defined benefitplan showed the following:Fair value of plan assets P7,500,000Defined benefit obligation (11,000,000)Prepaid (accrued) benefit expense (P3,500,000)Fischl determined that its current service cost was P1,000,000 and the interest cost is 10%. Theexpected return on plan asset was 12% but the actual return during the year was 8%. Other relatedinformation at the end of the year:Contribution to the plan P1,200,000Benefits paid to retirees 1,500,000Decrease in defined benefit obligation due to changes inactuarial assumptions200,000REQUIREMENTS:1. What will be presented in the income statement in relation to the defined benefit plan?2. What will be presented in the statement of financial position in relation to the defined benefitplan?