appointment as the new accountant of a client ountant even though he is aware that the exis collected professional fee from said client.

appointment as the new accountant of a client ountant even though he is aware that the exis collected professional fee from said client.

Survey of Accounting (Accounting I)

8th Edition

ISBN:9781305961883

Author:Carl Warren

Publisher:Carl Warren

Chapter7: Fixed Assets, Natural Resources, And Intangible Assets

Section: Chapter Questions

Problem 7.6C

Related questions

Question

100%

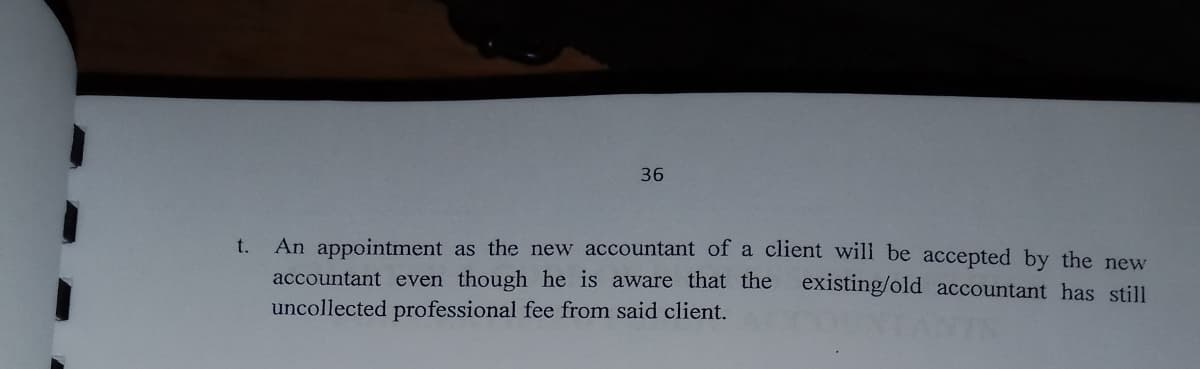

Transcribed Image Text:36

An appointment as the new accountant of a client will be accepted by the new

accountant even though he is aware that the existing/old accountant has still

t.

uncollected professional fee from said client.

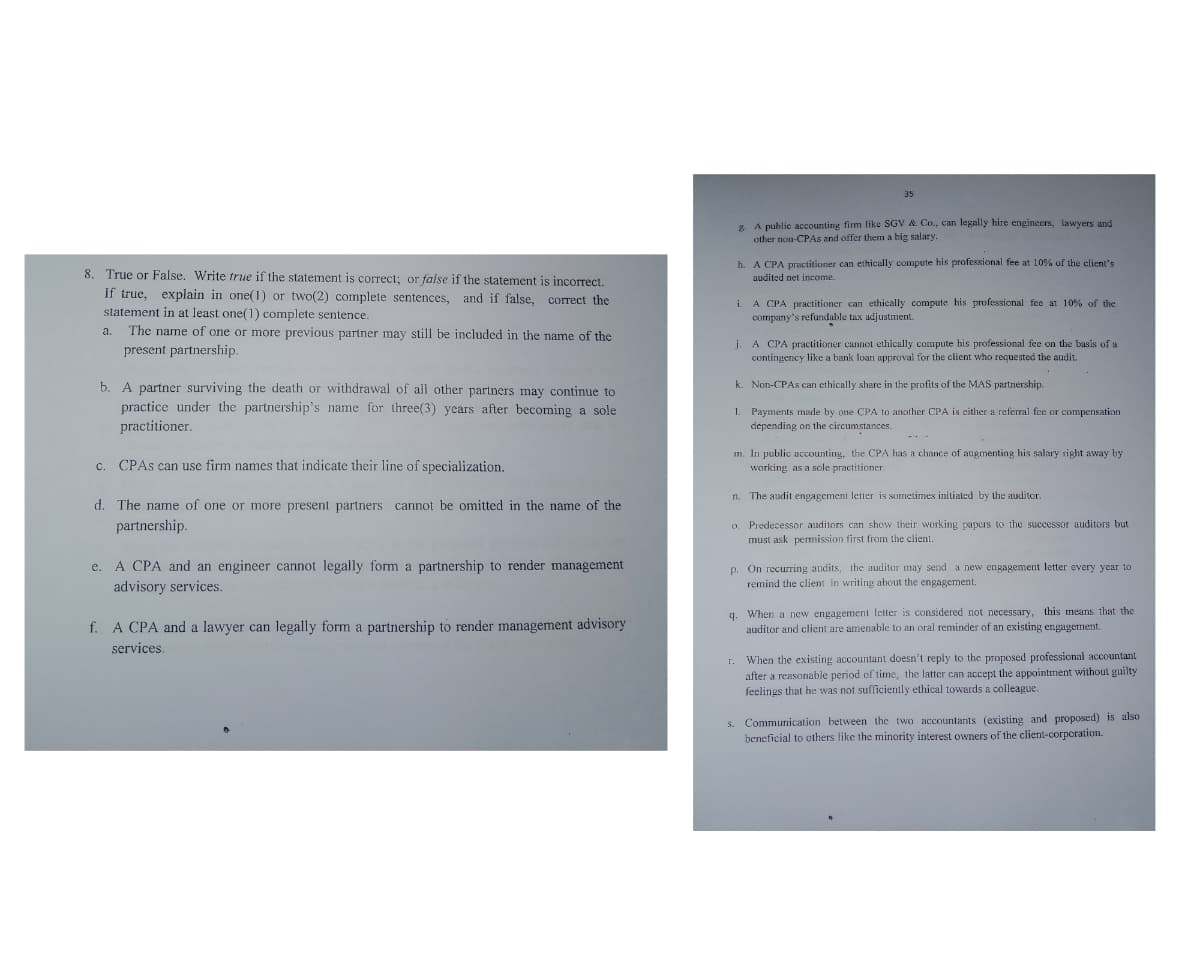

Transcribed Image Text:35

* A public accounting firm like SGV & Co., can legally hire engineers, lawyers and

other non-CPAS and offer them a big salary.

h. A CPA practitioner can ethically compute his professional fee at 10% of the client's

8. True or False. Write true if the statement is correct; or false if the statement is incorrect.

audited net income.

If true, explain in one(1) or two(2) complete sentences, and if false, correct the

statement in at least one(1) complete sentence.

i. A CPA practitioner can ethically compute his professional fee at 10% of the

company's refundable tax adjustment.

a.

The name of one or more previous partner may still be included in the name of the

j. A CPA practitioner cannot ethically compute his professional fee on the basis of a

contingency like a bank loan approval for the client who requested the audit.

present partnership.

b. A partner surviving the death or withdrawal of all other partners may continue to

k. Non-CPAS can ethically share in the profits of the MAS partnership.

practice under the partnership's name for three(3) years after becoming a sole

practitioner.

1. Payments made by one CPA to another CPA is cither a referral fee or compensation

depending on the circumstances.

c. CPAS can use firm names that indicate their line of specialization.

m. In public accounting, the CPA has a chance of augmenting his salary right away by

working as a sole practitioner.

n. The audit engagement letter is sometimes initiated by the auditor.

d. The name of one or more present partners cannot be omitted in the name of the

partnership.

o. Predecessor auditors can show their working papers to the successor auditors but

must ask permission first from the client.

O.

e. A CPA and an engineer cannot legally form a partnership to render management

p. On recurring audits, the auditor may send a new engagement letter every year to

remind the client in writing about the engagement.

advisory services.

f. A CPA and a lawyer can legally form a partnership to render management advisory

q. When a new engagement letter is considered not necessary, this means that the

auditor and client are amenable to an oral reminder of an existing engagement.

services.

r. When the existing accountant doesn't reply to the proposed professional accountant

after a reasonable period of time, the latter can accept the appointment without guilty

feelings that he was not sufficiently ethical towards a colleague.

s. Communication between the two accountants (existing and proposed) is also

beneficial to others like the minority interest owners of the client-corporation.

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

Step by step

Solved in 2 steps

Recommended textbooks for you

Survey of Accounting (Accounting I)

Accounting

ISBN:

9781305961883

Author:

Carl Warren

Publisher:

Cengage Learning

Survey of Accounting (Accounting I)

Accounting

ISBN:

9781305961883

Author:

Carl Warren

Publisher:

Cengage Learning