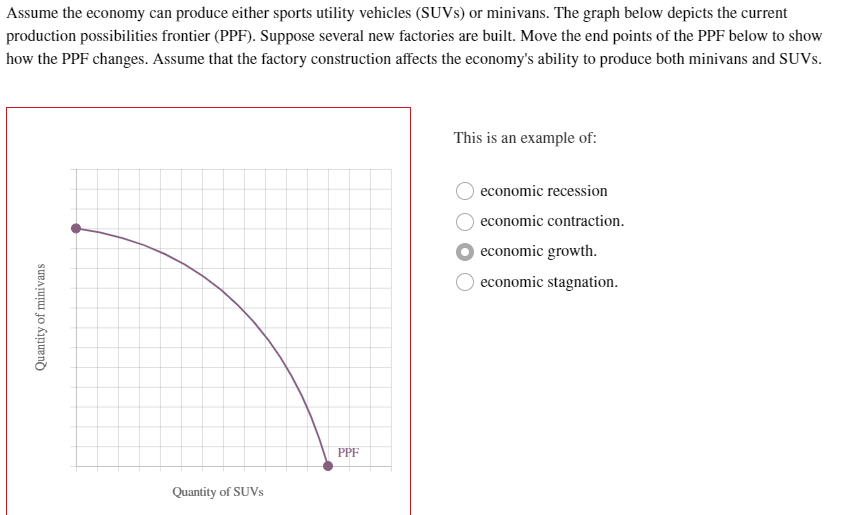

Assume the economy can produce either sports utility vehicles (SUVS) or minivans. The graph below depicts the current production possibilities frontier (PPF). Suppose several new factories are built. Move the end points of the PPF below to show how the PPF changes. Assume that the factory construction affects the economy's ability to produce both minivans and SUVS. This is an example of: economic recession economic contraction. economic growth. economic stagnation. PPF Quantity of SUV. Quantity of minivans

Assume the economy can produce either sports utility vehicles (SUVS) or minivans. The graph below depicts the current production possibilities frontier (PPF). Suppose several new factories are built. Move the end points of the PPF below to show how the PPF changes. Assume that the factory construction affects the economy's ability to produce both minivans and SUVS. This is an example of: economic recession economic contraction. economic growth. economic stagnation. PPF Quantity of SUV. Quantity of minivans

Chapter9: Classical Macro Economics And The Self Regulating Economy

Section: Chapter Questions

Problem 6WNG

Related questions

Question

Full explanation.

Thank you

Transcribed Image Text:Assume the economy can produce either sports utility vehicles (SUVS) or minivans. The graph below depicts the current

production possibilities frontier (PPF). Suppose several new factories are built. Move the end points of the PPF below to show

how the PPF changes. Assume that the factory construction affects the economy's ability to produce both minivans and SUVS.

This is an example of:

economic recession

economic contraction.

economic growth.

economic stagnation.

PPF

Quantity of SUVS

Quantity of minivans

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution!

Trending now

This is a popular solution!

Step by step

Solved in 2 steps

Recommended textbooks for you

Economics (MindTap Course List)

Economics

ISBN:

9781337617383

Author:

Roger A. Arnold

Publisher:

Cengage Learning

Economics (MindTap Course List)

Economics

ISBN:

9781337617383

Author:

Roger A. Arnold

Publisher:

Cengage Learning